Price growth edges lower despite reasonable economy

Insight

It's been a classic risk-off session so far, at least in the second half.

You’re out of time, those bad apples no friend of mine – the Tribes

With both bonds and currencies for the most part responding as they ‘should’ to the macro and micro developments that have led US stocks lower, the latter led by the technology and consumer discretionary sectors and which sees the S&P500 finish the New York day -1.2%, the Dow -1.3% and the NASDAQ -2.3%.

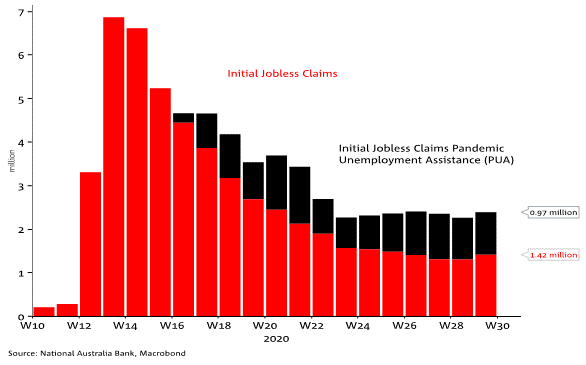

The macro news that has spooked US stocks includes the latest weekly US initial jobless claims data, which unexpectedly rose to 1.416 million against the unchanged 1.3 million expected, on top of which there were 975k new claims under the Pandemic Unemployment Assistance programme by those ineligible for regular unemployment benefit (up from 955k the prior week – see Chart of the Day below). Our friends at Pantheon Economics note that highly unfavourable seasonal adjustment factors were at least part of the reason for the jump in claims, which normally drop sharply at this time of year due to the end of auto-sector shutdowns for re-tooling. This year there were no such shutdowns as firms scrambled to restore depleted inventories caused by the earlier disruption to supply chains, but the seasonal adjustment factor won’t have picked this up.

Such niceties have been lost on the market, but in any event can’t distract from the fact claims are running at more than double their worse weekly levels seen during the 2008 GFC. The data also comes just in front of this weekend’s expiry of the additional $600 weekly unemployment benefit introduced under the CARES Act and currently being drawn by more than 30 million Americans (note not 25 million, as mentioned in our earlier edition). Uncertainty as to whether this week’s payment will be the last or will be extended in time for further payments from the end of the month looks to have aggravated equity market concerns – it could certainly account for some of the 2.0% fall in the consume discretionary sub-sector of the S&P. (NB: the above clarifies our comment in the earlier edition which inferred that benefit payments would cease this weekend. Eligibility for these payments does expire this weekend in all states, but those people currently eligible will receive a payment this week, designed to cover them through the end of next week, which is when the ‘cliff edge’ occurs if Congress fails to agree an extension to the benefit period before 31 July).

Uncertainty over this benefit extension is part of the broader concern as to whether Congress will agree a unified economic stimulus/support bill before the traditional August recess. Remember here that the House is due to go into recess on July 31 (next Friday) and the Senate a week later, but whether this will happen or not if there is no agreement by the 31st remains to be seen. The White House and Republican Senators have not yet dotted the i’s and crossed the t’s on their roughly $1tn proposed economic support package, which once finalised is only the start of a process of reconciliation with the earlier House-passed $3.5tn+ stimulus plan. The Republican plan drops proposals for a payroll tax cut to which many Senators were opposed (a defeat for President Trump). Instead, a repetition of the $1,200 cash handouts for some households looks likely to form part of the plan.

House speaker Nancy Pelosi has been out saying that ‘we cannot piecemeal’ another stimulus package, which is exactly what US Treasury Secretary Steve Mnuchin looks to be proposing, suggesting aid bills be handed ‘in a tiered manner. There’s a long way to go here in a very short space of time.

At the micro/sector level the technology sector, leading the way up in recent weeks (and months) has led the way down, including falls of 4% for Microsoft and 5% for Apple. The latter’s hit is linked at least in part to an Axios report saying multiple US states are investigating Apple for potentially deceiving consumers, according to a March document uncovered by Tech Transparency Project, a tech watchdog group. It says the Texas attorney general may sue Apple for violating the state’s deceptive trade practices law in connection with a multi-state investigation. In the bigger picture, this news likely represents just a foretaste of what is likely to come post the November US elections by way of stepped up antitrust/anti-monopoly investigations of ‘Big Tech’, including Google and Facebook, as well as EU-orchestrated efforts for a new digital tax regime for global technology behemoths.

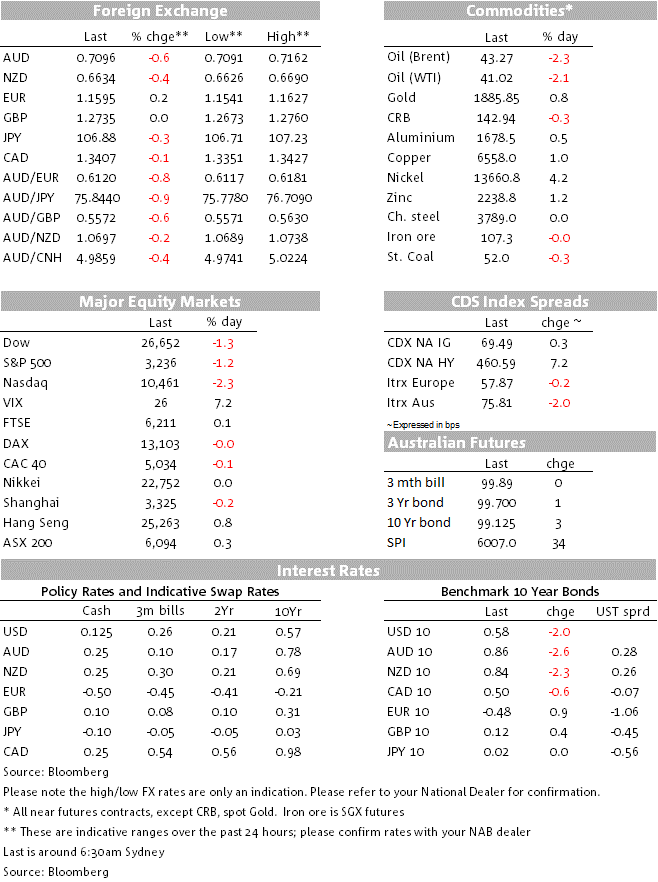

Following a mixed day in Europe where Euro-peripheral government debt has seen further spread compression versus the core (Italy -5bps, Germany +1bp at 10-years) US Treasuries have just closed in New York with the 10-year Note at its lowest close since 21 April and its third lowest since the virus crisis began, down 2bps on the day to 0.58%.

Rationality reigns with the safe haven JPY and CHF at the top of the G10 scoreboard, up 0.3% and 0.4% respectively in the last 24 hours, and AUD and NZD down 0.6% and 0.5% respectively, losses surpassed only by the NOK (-1.4%). The latter has been hit by further falls in oil prices (WTI -$0.85 and Brent -$0.97), the market still reeling from the unexpected 4.7 million barrel jump in crude inventories reported on Wednesday by the EIA and, seemingly, the demand side implications of the aforementioned economic news and doubts over timely fiscal support for the economy. News headlines of US virus cases now surpassing 4 million can’t be helpful either can it?

Holding down USD indices (DXY -0.17%, BBDXY -0.1%) has been further gains for the EUR, still feeding positively off this week’s EU recovery fund deal (ditto Euro-peripheral debt market). EUR/USD has added 0.2% to Tuesday’s and Wednesday’s gains, to spend time above 1.16 (1.1595 now, its best NY closing level since 27 Sep 2018).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.