Labour market strong, housing supply falling behind

Insight

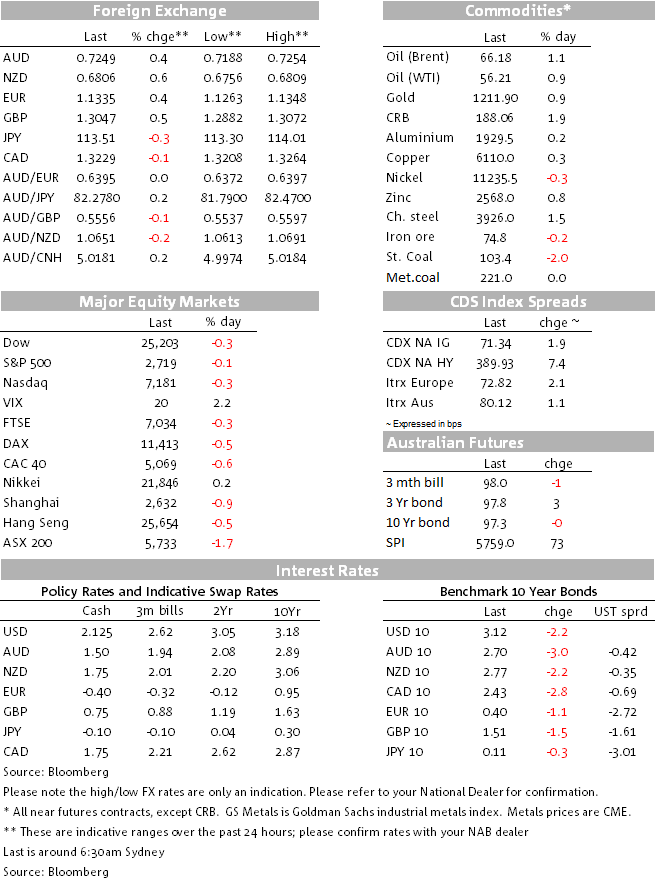

Uncertainty on whether the UK Cabinet would pass May’s Brexit deal played heavily on the pound overnight but it rebounded when the deal was approved.

https://soundcloud.com/user-291029717/mays-first-hurdle-step-two-is-survival

It’s been a wild couple of hours with markets wracked by uncertainty as to whether the UK Cabinet would endorse the 500-page Brexit Withdrawal Agreement stitched together the day before and whether UK PM Theresa May would imminently face a leadership channel. The uncertainty factor had earlier weighed on broader market risk sentiment; hence US stocks and bond yields have pulled back up somewhat on news of Cabinet agreement to the proposed deal. The latter still leaves parliamentary approval in considerable doubt. We still can’t say with any confidence whether this deal, no deal, or indeed a second referendum, is now the most probable outcome to this ongoing saga.

GBP lost a quick 1.5 cents when it became evident the UK Cabinet meeting was continuing beyond its expected time and with that a presumption that a sign-off on the Brexit Withdrawal Agreement was looking unlikely. All of those losses have since been recovered – and then some – after PM Theresa May (who looked to be facing an imminent leadership challenge) confirmed that the Cabinet has now agreed to support the Agreement. GBP/USD has been as low as 1.2880 and as high as 1.3060.

Earlier in the offshore session, EUR/USD was under mild downward pressure after German Q3 GDP printed -0.2% against -0.1% expected, albeit Eurozone preliminary GDP a few hours later came in at +0.2% as expected.

German economic weakness is seen to reflect a combination of auto sector re-tooling related to new EU emission standards but also some hit from trade tensions and in particular weaker Chinese demand for German exports. The former we can be confident will prove temporary, the latter we can’t yet be sure about and which is prompting speculation that the start of ECB interest rate policy normalisation could be shunted into 2020 from ‘after the summer of 2019’ as currently postulated by the ECB.

This debate will intensify in front of the December 13th last ECB meeting of the year and is a crucial factor for the fate of all things EUR (as well as Eurozone yields and with that US and global yields) either side of year-end.

Currency moves elsewhere have been relatively mild. The Swedish Krone slumped after CPI printed 1/10% below expectations casting doubt on a first Riksbank tightening as soon as the December 20th meeting. The NZD sits on top off the G10 leader board for no obvious reason beyond the suggestion of ongoing covering of speculative short positions, with perhaps some fresh speculative selling of AUD/NZD after the cross broke below prior lows around 1.0660.

The JPY is back displaying some (mild) safe-haven characteristics to be the second best performing currency on the night. The AUD (currently 0.7249) has been largely sidelines after failing to get fresh steer from yesterday ‘as expected’ Q3 wages data and in front of this morning’s October labour market data. It has popped up 20 points or so post the Brexit news.

Concerns as to whether global growth is faltering are being discussed more openly, doubtless sparked in part by the negative Japanese and German Q3 GDP prints even if retooling and weather were doubtless beyond some of the reported weakness. Financials had been leading US stock indices lower – consistent with the notion of potentially slower growth and flatter yield curves as result. The main board US indices were all down a little under 1% prior to the news of UK cabinet endorsement of the Withdrawal Agreement, but losses have since been pared by more than half.

US 10 year bonds fell to as low as 3.09% from an intra-day high of just above 3.16% amid the generally risk-averse tone and aforementioned growth concerns and the earlier slight easing in benchmark EZ yields. Gilt yields also fell after headline UK CPI came in just on the low side of expectations (0.1% against 0.2% expected) albeit core CPI at 1.9% was unchanged as expected. Treasuries have since pulled back up a couple of basis points (news of the UK Cabinet agreement to the Brexit Withdrawal agreement has helped here). There was no major impact from the US October CPI release, where headline and core printed as expected at 0.3% and 0.2% respectively. Expected rebounds in rents and used car prices were largely responsible for the gains in core CPI.

Oil has enjoyed a very mild rebound (WTI and Brent currently both up 0.6-0.7%) on new that OPEC and its partners are now contemplating a 1.3 mn. barrels per day production cut. Most other commodities re higher though iron ore and metallurgical coal are little change and steaming coal off 2%.

GE: GDP (q/q%), Q3: -0.2 vs. -0.1 exp.

UK: CPI core (y/y%), Oct: 1.9 vs. 1.9 exp.

EC: Industrial production (m/m%), Sep: -0.3 vs. -0.4 exp.

EC: GDP (q/q%), Q3: 0.2 vs. 0.2 exp.

US: CPI ex food and energy (y/y%), Oct: 2.1 vs. 2.2 exp.

Fed chair Jay Powell is due to give a speech at a Dallas Fed event starting at 10:00 AEDT

AU employment @ 11:30 AEDT. Markets are expecting only a small lift in the unemployment rate to 5.1%, only reversing a third of last month’s sharp fall. NAB expects unemployment to stay at 5%. We expect employment grew 25k in the month (mkt: +20k), and the participation rate lifted a touch to 65.5% (mkt: 65.5%).

China New Home prices @12:30 AEDT.

UK then US retails sales this evening, also weekly US jobless claims and import and export prices.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Labour market strong, housing supply falling behind

Insight

Discover how to take advantage of opportunities in the US Private Placement (USPP) market.

Video

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.