Price growth edges lower despite reasonable economy

Insight

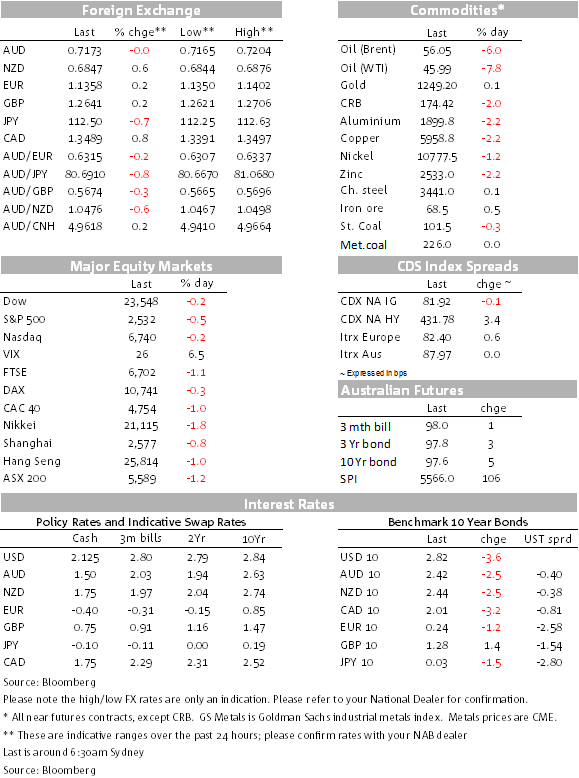

Oil fell even further overnight.

https://soundcloud.com/user-291029717/oil-lower-euro-economy-weaker-trump-warns-against-a-fed-hike

Two big stories overnight, another cathartic clean out in oil prices and more pressure from President Trump on the Fed after the Wall Street Journal suggested the Fed should pause. Stocks were down in Europe after the soggy session in Asia yesterday, the US market was showing green but has reversed into the red into the last hour of trade. Treasury yields are lower again, helped along the way by lower oil, led at the front end, perhaps with a degree of caution ahead of tomorrow’s FOMC. Among currency pairs, the CAD and NOK have been the underperformers, followed by the AUD.

The market wants to take oil lower and news of recent days seems to have given traders the ammunition to sell it lower. The EIA reported earlier this week that it expected US shale production to rise in January while the WSJ reported that Russian production reached a record in December. We also note that US oil production has risen more than 15% this year and that rig count numbers have, so far, been relatively resilient.

The WSJ published an editorial headed “Time for a Fed pause”, arguing the case for the Fed not to hike rates so soon again. “What to do? The right answer is to ignore the politics, inside and outside the Fed, and follow the signals that suggest a prudent pause in raising rates at this week’s meeting”. President Trump jumped on that opportunity and tweeted “I hope the people over at the Fed will read today’s Wall Street Journal Editorial before they make yet another mistake…. Feel the market… Good luck!”.

While the market is pricing in a dovish hike, an expectation for the Fed to then pause, were they to pause, it could be viewed as bowing to political pressure and of course markets could fret over “what does the Fed know that we don’t or haven’t priced for”. The Fed can engineer and market-supportive response but hiking but scaling back underscoring that further “gradual” increases are nowhere near certain. Two year Treasury yields have rallied by 4bps to 2.65% as the market has further scaled back rate hike expectations, though somewhat surprisingly a little less so at the very front end of Fed fund futures.

The German Ifo Survey for December missed expectations slightly. All three components were lower than expected, but not remarkably so, the Current Conditions index at 104.7, close to last year’s average of 105 when the economy grew by 2.2%. It’s still a relatively solid number in level terms, if off its highs from early this year.

US Housing Starts and Permits were better than expectations, signifying a degree of resilience in US housing activity, which should get some support from post-disaster reconstruction and the rally in bonds and thus mortgage rates. The Atlanta Fed shaved their estimate of Q4 GDPNow to 2.9% from 3.0% on a net downscaled estimate of fourth-quarter real residential investment growth from -2.4 percent to -4.2 percent after the data, including revisions.

On the 40th anniversary of Deng’s market opening and reform, in a strong political speech yesterday, President Xi Jinping vowed to push` ahead with China’s “reform and opening up” but warned that “no one is in a position to dictate to the Chinese people what should or should not be done”. It was the latter element of defiance that has captured most of the press since, a read through being that this revealed an element of defiance to the US.

Such an interpretation looks like it could be an over-reach. This was the prelude to the coming setting of economic goals, was more political in nature, ceremonial, messages intended to reinforce the Party’s position, and his leadership. Cooler analysis – including in his strong political speech – suggest that he still wants to get a deal done with the US. In his address he spoke of reform’s importance, noting that “opening brings progress while closure leads to backwardness”.

The main elements and goals for the economy and economic reform will be thrashed out in the remainder of this week starting today at China’s three day Central Economic Working Conference (CEWC) meeting to reset growth and reform objectives. The economic leadership will decide on their growth target for 2019 (pulled back slightly from 5.5% this year), the main elements of macroeconomic policy (growth-supportive fiscal policy), structural change/reform, such reform to include measures that will be the essence of a deal during the 90 day truce, carrots likely on market access and reform of intellectual property rights. Chinese lawmakers are also set to meet before the end of the year, including on such reforms.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.