Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

Oil and equities have bounced back up.

https://soundcloud.com/user-291029717/oil-rises-stocks-rebound-china-warned

When the weekend comes I know I’ll feel alive (Bounce), You will be the last thing on my mind (Bounce) – Calvin Harris.

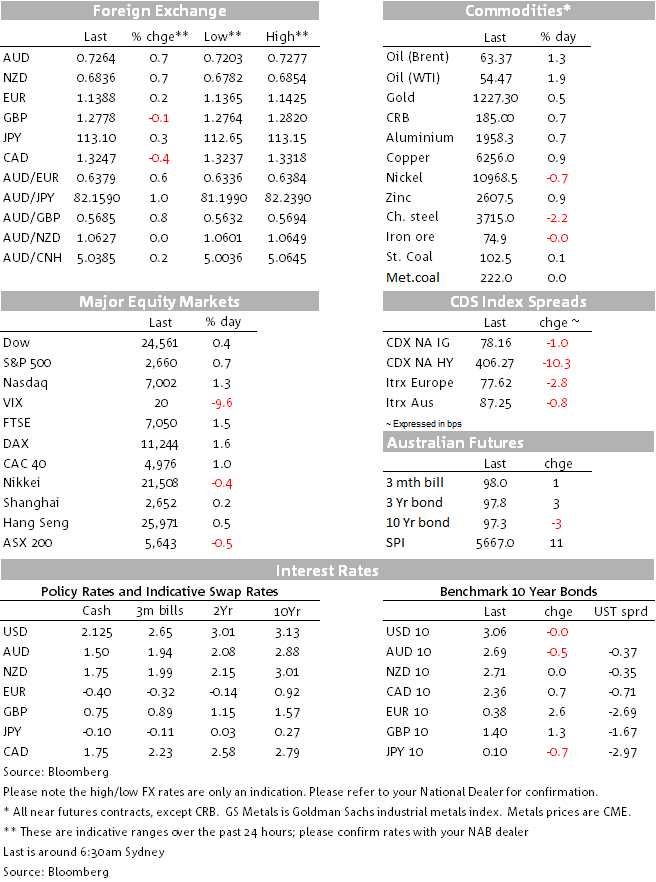

After two consecutive days of steep declines, US equities have rebounded overnight with gains led by energy shares and small caps. Amid a low trading environment ahead of Thanksgiving holiday tonight, gains in oil prices have been one supporting factor while US economic data printed on the softer side of expectations. Improvement in risk appetite sees the USD give up some ground with AUD and NZD among the main beneficiaries within G10 currencies. Meanwhile UST yields are a touch higher and BTPS rallied on hopes of an Italian budget compromise

An improvement in risk appetite alongside an increasing number of commentary suggesting the Fed could well be considering a pause to its gradual tightening plan next year has seen the USD give up some of its recent gains. The narrow DXY index now trades at 96.69, down 0.14% on the day while the broader BBDXY is at 1204.78, down -0.15%. That said declines in both indices are relatively minor and both remains comfortably in their upward trends established late in September. Meanwhile EM FX (+0.36%) and ADXY (Asian Currency index, +0.23%) have made bigger gains reflecting the risk on mood overnight.

An MNI report suggesting the Fed may be looking to pause next year got a fair bit of air time and has played a role for the small pullback in the USD overnight. The report suggested the Fed could end its cycle of interest rate hikes “as early as the spring, as it starts to consider at least a pause to its gradual monetary tightening”, according senior Fed sources. The report also noted that the Fed is just one or two hikes away from a point where major decisions have to be made about the outlook, so while a December rate hike is all but assured, the debate will become more lively beginning at the central bank’s March meeting and certainly by June. It added that last week’s seemingly more dovish comments by Fed vice-chair Clarida in a CNBC interview was part of a coordinated step, following the market reaction to Chair Powell’s upbeat remarks in early October.

To some extent the report is not new news, but it has helped reaffirm the repricing in Fed expectations seen in recent weeks. Early in the month the market was looking for 1.5 Fed hikes in 2019 and now these expectations have declined to 1.15.

AUD and NZD have made decent gains overnight (~0.70%) boosted by the improvement in risk appetite that has seen the VIX index ease back from yesterday’s intraday high of 23.81 to be 20.14 currently. AUD now trades at 0.7264, so a little bit above the middle of its 0.7071 to 0.7338 range held since the start of the month. NZD on the other hand now trades at 0.6836, closer to the top of its 0.6515-0.6884 range month to date. Risk sentiment looks to be the current main driver for both antipodean currencies, thus focus is now likely to shift towards Black Friday, the day after Thanksgiving, which marks the traditional start to the U.S. holiday shopping season. Amid concerns of a slowing economy and softer equity market, the level of shopping on Friday is likely to be treated as an important gauge of the US consumer state of mind.

After Black Friday, focus is likely to shift back to US-China tensions ahead of the G20 summit next weekend. On that front the news flow is not that reassuring. US-China trade tensions haven’t gone away. Yesterday the Office of the US Trade Representative released an updated report on the investigation of China’s trade practices regarding technology transfer, intellectual property, and innovation. The report concluded that “China fundamentally has not altered its acts, policies, and practices” in this area and “indeed appears to have taken further unreasonable actions in recent months.” The report increases the pressure on China to come up with something ahead of the Xi-Trump meeting on December 1st.

The improvement in risk sentiment has seen USD/JPY climb back above 1.13, while the Euro got a small boost on hopes of an Italian budget truce. The union currency now trades at 1.1388, after briefly trading above 1.14 overnight. No Brexit news sees the pound unchanged at 1.2781.

Oil prices have rebounded overnight helping improve the mood in equity markets. Brent is +2.29% to $63.32 and WTI is +1.42% to $54.45. The bounce in oil prices is interesting considering the stream of negative headlines overnight and as a result it suggest that the market has become short-term oversold. Those headlines included Saudi oil production rising strongly in November, and production across Saudi Arabia, the US and Russia at a near-record level, a report that oil production in the US Permian basin might soon been profitable at a price of just $30 a barrel, and the pipeline bottleneck in Texas set to ease by the end of next year. President Trump tweeted “Oil prices getting lower. Great! Like a big Tax Cut for America and the World. Enjoy! $54, was just $82. Thank you to Saudi Arabia, but let’s go lower!”. We see this as a slightly odd comment when the US is now the world’s largest oil producer and the country and its trade balance would benefit from higher oil prices.

The lift in risk appetite also helped other commodities perform with copper +0.94%, LMEX +0.73% and gold +0.52%. Iron closed unchanged at $74.86.

US equities look set to end the day in positive territory, after starting the week with two days of solid declines. Gains have been led by the energy sector after a decent rebound in oil prices ( more below) while small caps (Russell 200 index is up to just under 2%) and technology shares have also joined the party. That said with questionable factors driving the rebound in oil against a backdrop of light trading volumes before Thanksgiving holiday, it is probably fair to day that the rebound looks to the function of an oversold rather than a fundamental change on the outlook for equities. If anything the softer than expected US data releases overnight played to the view that a slowdown in growth looks to be in the offing.

Early in the session European equities also closed higher with the Eurostoxx 50 climbing 1.51% after 5 consecutive days of negative returns.

US Treasury yields are up 1-2bps across the curve, reflecting the risk-on backdrop and higher oil prices. Italy’s 10-year rate is down 15bps as the market takes a more optimistic view on the budget stand-off with the European Commission. As expected, in its annual review the commission said that Italy’s budget is in “particularly serious non-compliance” of EU limits. But the market hooked on to Italian Deputy Premier Salvini’s comment that although he won’t compromise on core items such as tax cuts and a basic income for the poorest, he is willing to make tweaks and is open to dialogue.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Mandatory climate disclosures are on the way for thousands of businesses and organisations in Australia, with a start date as early as next year planned for the largest corporates. NAB unpacks what’s on the horizon.

Article

Labour market strong, housing supply falling behind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.