Price growth edges lower despite reasonable economy

Insight

How low can the pound go if the UK shifts towards a no-deal Brexit?

https://soundcloud.com/user-291029717/pound-hit-hard-may-ploughs-on-regardless

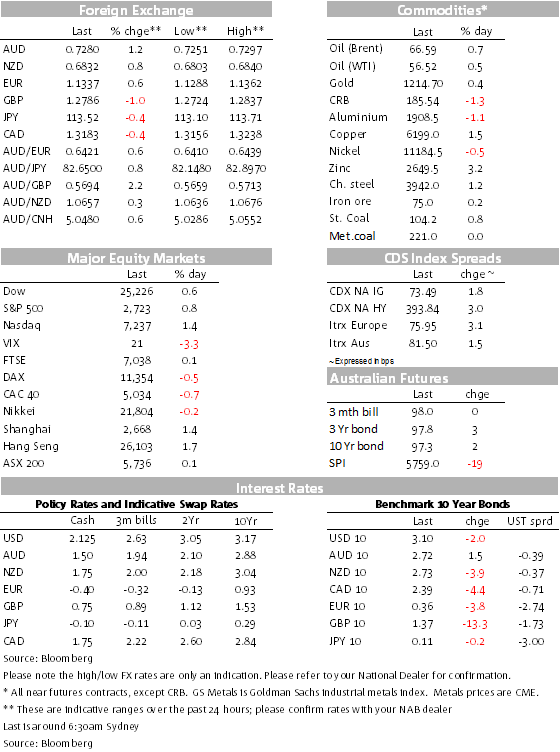

The Economist has described it as political chaos, a Scottish parliamentarian described Brexit as “a step backward into the imagined past”. Somebody else urged me to use “Houston, we have a problem”. Whatever the description you choose, it’s been extremely tumultuous night for Brexit and UK politics, Sterling taking a bath, losing more than two big figure against the USD, the Euro gaining nearly two big figures against sterling, and the AUD this morning trading at over 0.57, having been in the 55s yesterday, also helped by yesterday’s low unemployment AUD rally.

The pressure escalated with no less than the resignation of Brexit Secretary Raab in the wake of the previous day’s five hour Cabinet meeting that approved the Withdrawal Agreement (WA), Raab saying that he could not support the terms of the WA. It was then off to the races as another five ministers joined the resignation queue, the tense political climate heightened by MPs suggesting that there would be a challenge to May’s leadership, led by prominent Brexiteer Jacob Rees-Mogg.

When the Prime Minister called a press conference late in the afternoon, there was speculation she might resign. But no, when the going gets tough, the tough get going and she was batting on to get the job done. She said that she believed with “every fibre of my being” that the course she has set out for Brexit is the right one, telling the Commons later in the afternoon that “British people want us to get this done”.

Just on the leadership challenge, before a vote can take place, under Conservative party rules, the Chairman of the 1922 Committee needs letters from 15% of Conservative MPs before a vote can be called. That equates currently to 48 letters that apparently have not been received, as yet. If there is a vote, and if she survives, she’s then immune from another challenge for 12 months.

Not surprising that in this fast-changing environment, Sterling volatility is the highest since the 2016 Brexit referendum. Markets now have the almost impossible task of navigating thought a maze of possibilities with the potential for leadership changes, whether she can get Parliamentary approval, could the Government lose the confidence of the House and therefore another election, would there be a change of Government, will the Europeans approve the deal and get it passed by continental parliaments? There are truly many questions and possibilities.

Almost as an aside, UK Retail Sales were on the soft side, but the damage had already been done to Sterling and it was full-on Brexit focus. Retail Sales excluding fuel fell 0.4% against expectations that a 0.2% gain would follow last month’s 0.3% decline. The disappointment was partly ascribed to a mild autumn denting winter clothing sales.

Stocks have had a mixed night, down in Europe, initially choppy in the US, but having a better overnight session. As we go to press, the S&P 500 is up 0.49%, the Dow doing about the same, the Nasdaq better, lifted by some trade tension optimism.

Oil had been staging a mild rally after the big sell off in recent weeks, but this mild rally was stifled by the weekly US crude inventories report revealing a whopping 10.27mb rise against expectations of a 2.914mb rise. Despite this inventory build, both WTI (currently $56.18) and Brent ($66.53) are up ¼-½% on net for the day, suggestive of the unwinding of some shorts. Elsewhere, gold is up marginally, by 0.33%, and despite some net rise in the USD. Base metals were mixed, copper and zinc up in size, but ally and nickel lower. Iron ore and Chinese steel rebar futures made some net gains yesterday.

UK gilts rallied in size, the 10y down 13.3bps in a European market with a bid tone. US yields have eased marginally, by around 1bps along the curve, 10s currently at 3.11% well within its recent range. The US Retail Sales report for October revealed headline sales were stronger than expected, while the “control group” that feeds into household consumption was a little shy of expectations. The Atlanta Fed’s GDPNow estimate for the December quarter was shaved to 2.8% from 2.9% with consumption growth lowered to 2.7% from 2.9% after the retail sales report.

Import prices ticked higher in October, up 0.2% (excluding oil) against expectations of a flat result, a hint perhaps of some tariff impact, and following some declines in recent months from USD strength. Fed President Bostic noted overnight that while the tariffs had so far not affected inflationary expectations, he noted that trade tension and tariffs had seen businesses delaying investments. Powell was also speaking, mentioning that wages were about where he expected them to be given inflation and productivity, having said yesterday during our time zone that he was essentially waiting to see how inflation and growth would evolve to condition the Fed’s stance further. Gradual for now.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.