Price growth edges lower despite reasonable economy

Insight

It’s been a relatively quiet 24 hours with only slight market moves

https://soundcloud.com/user-291029717/powells-slow-road-biden-plays-it-cool-with-china?in=user-291029717/sets/the-morning-call

According to Songacts, this instrumental studio jam at the end of the My Generation album was titled for The Who’s bass player, John Entwistle, who was nicknamed “The Ox” for his strong constitution and ability to out-eat and out-drink the other band members. Doubtless the inspiration for some of my colleagues.

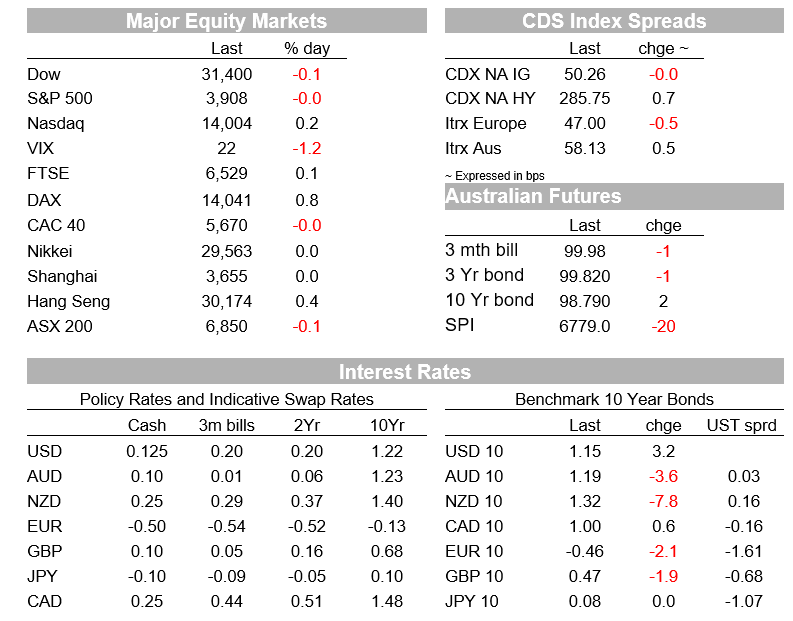

The S&P 500 is down 0.15% and the NASDAQ +0.1%.

US Treasury yields have recouped all of the ground they lost on Wednesday afternoon (10s currently up 3.5bps to 1.15%) while a mixed performance in currencies sees the AUD at the top of the G10 scoreboard, +0.3% and following slight slippage in oil prices – albeit Brent crude is holding above $61 for the third day running – NOK at the bottom (-0.3%) with GBP also giving back a little of its recent strong gain (-0.2%).

Was for weekly US initial jobless claims, which fell to 793K from an upwardly-revised 812K, above the consensus, 760K. The four-week moving average level of initial claims has dropped to a five-week low of 823K, and should fall further as restrictions are slowly eased across many parts of the country.

We won’t see January’s drop in US non-fam payrolls repeated in February and beyond.

At the same time, the current level of claims remains a long way above the worst single reading during the GFC of 655K and, as Fed chair Jay Powell noted this time yesterday morning, the level of employment last month was nearly 10 million below February 2020 levels, such that, “Achieving and sustaining maximum employment will require more than supportive monetary policy”.

No signs of concern here at the proposed $1.9tn additional covid-relief on top of the $900bn agreed at the end of last year.

We see declining infection trends in most countries – in the US currently averaging around 100,000 new cases a day down from 250,000 at their turn-of-the-year peak, and too hospitalization rates, with particularly sharp falls in infection rates in Spain and, interestingly giving the concerns about the efficacy of at least one of the vaccines vis-à-vis the South African strain, South Africa itself.

Vaccination roll-outs are proceeding apace, with the number of doses administered in the UK now exceeding the equivalent of 20% of the population (though bear in mind these numbers include those now getting their second jab) and in the US comfortably in double digits, while the EU average looks to be nearer 4%.

All encouraging, but not sufficient to allow markets to price in much full economic re-openings in H2 2021 (ex-cross border travel) than they already are.

The Winter economic forecasts released by the European Commission overnight have the Euro area growing by 3.8% this year and next.

That masks what is expected to be a contraction this quarter, before lockdown restrictions/containment measures see growth pick up through Q2 and more so through the second half, including as the vaccine programs are rolled out.

The EC now sees risks as more balanced, both from what’s expected to be a sustainable easing of containment and as the Next Generation EU recovery fund kicks in.

The EC have downgraded growth for this year (continuing restrictions into this quarter) from 4.2% to 3.8% but pushed some of that foregone growth from this year into 2022, upgrading the growth expectation from 3.0% to 3.8%.

The new EC forecasts are on the conservative side compared to the consensus 4.3% for 2021 and 4.0% for 2022. In its December economic projections, the ECB was forecasting growth of 3.9% for 2021 and 4.2% for 2022, those forecasts prepared before a large swath of vaccine news and lockdowns. Even so, the differences in forecasts are not particularly stark.

The biggest sector changes are a 0.7% rise in IT (hence NASDAQ outperforming the S&P) and a 2.2% decline in Energy, the latter given 1%+ falls in crude oil. Other commodities are mixed, with iron ore futures up 1% but copper down and aluminium flat.

The Eurostoxx 50 finished the day +0.6%.

Not much to note in bonds, save that yields in New Zealand fell sharply yesterday following a very well received set of bond auctions, for the 20-year tenor in particular and following which its yield dropped by 12bps.

Little overall movement in the USD with DXY +0.04% and BBDXY -0.1%, with AUD very comfortably outperforming all other G10 currencies, +0.4% to just above 0.7750 versus the next best performing NZD +0.14% at 0.7225.

The shift down in NZ-AU yield differentials yesterday looks to be a factor behind the further rise in AUD/NZD, which if it finishes in NY near its current 1.0730 level will be the highest close of the year to date.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.