Price growth edges lower despite reasonable economy

Insight

Strong US payrolls data on Friday saw bond yields push higher.

https://soundcloud.com/user-291029717/goldilocks-pushes-us-bond-yields-higher

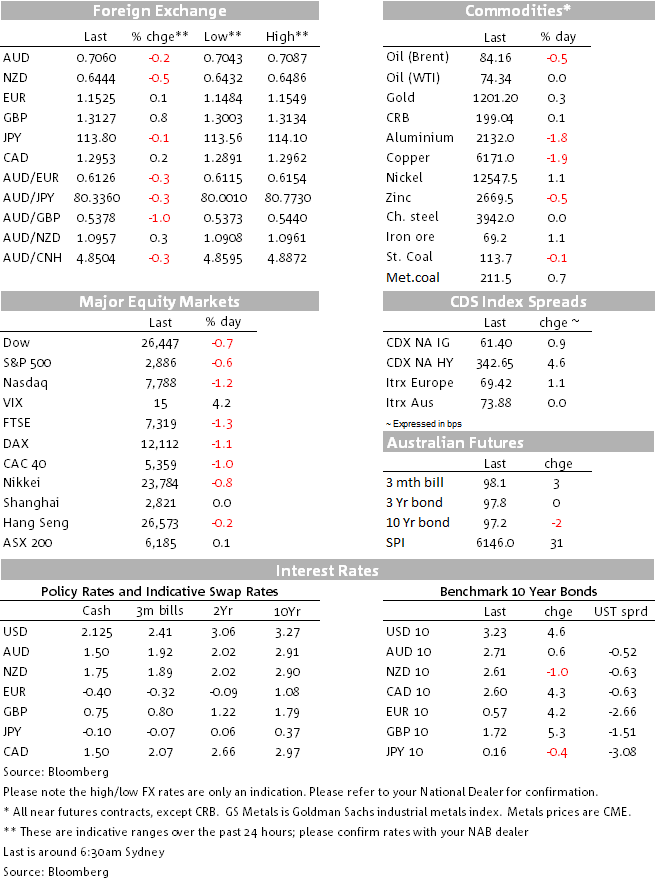

Friday’s US payrolls report, did nothing to arrest the rise in Treasury yields and where 10s came within kissing distance of 3.25% for a 17bps rise on the week. Upward revisions to July and August payrolls of 87k more than offset the headline miss of 134k and the unemployment rate fell to its lowest level since the Vietnam War (December 1969 to be precise).

So despite another ‘goldilocks’ employment report (average earnings growth is still contained at 2.8%) the combination of rising yields and the ongoing reverberations from Thursday’s Bloomberg ‘Big Hack story kept US equities pressured. The IT sector again lead the charge lower and ensured that the NASDAQ fell twice as much as the S&P500 for the second day running to be the second worst performing major global index on the week (-3.2%) after the smaller-cap Russell 2000 (-3.8%) though perhaps only because China was shut?.

A continuation of the ongoing short covering rally in Sterling meant that the dollar lost a bit of altitude in index terms while AUD and NZD remain very much under the cosh, both making new lows for this run lower.

Yesterday, the PBoC announced an across-the board 1% cut to Reserve Requirement Ratios (RRR) effective October 15th, a move will inject a net 750 billion yuan ($109.2 billion) in cash into the banking system by releasing a total of 1.2 trillion yuan in liquidity, with 450 billion yuan of that to offset maturing Medium-Term Lending Facility (MLF) loans. The PBoC claims The RRR cut would not create depreciation pressure on the yuan, saying the central bank would keep the foreign exchange markets stable. Let’s see.

For the second day in succession, Sterling was the best performing G10 currency Friday as optimism toward striking a Brexit Withdrawal Agreement acceptable to both sides continues to drive short covering in all things GBP. The AUD and NZD lost further ground to again be the worst performing currencies, AUD to a low of 0.7043 (closed in NY at 0.7052) and NZD to a low of 0.6432 (closed at 0.6443). CAD outperformed both AUD and NZD but was still down on the day despite a consensus busting 63.3l jump in employment, impact softened by the full time/part split of -16.9k/80.2k.

GBP strength, along with minor gains for JPY and EUR, ensured the DXY had a small down day and BBDXY a bigger one, the latter thanks to negative contributions from MXN, CAD and KRW in particular. KRW, THB and IDR against led losses for the ADXY and which was 0.1% lower on the day. The Antipodeans are the worst performing currencies on the week, Aussie down 2.38% and the Kiwi 2.66%. USD indices are just over half a percent up and ADXY almost a percent lower. All eyes will be on CNY on Monday where given intervening moves in CNH, our estimate for the appropriate level of today’s CNY fixing is 6.8840.

Friday saw a repeat of Thursday’s IT sector led losses sparked in part by the Bloomberg ‘Big Hack’ report (in which respect note the US Department of Homeland security has been out saying it has no reason to disbelief the denials by Apple and Amazon that their computers had been compromised). The NASDAQ was 1.16% against -0.55% for the S&P with the IT sector down 1.3% within the S&P500. China was shut all week of course and there will be keener than normal interest in how Shanghai opens up this morning on the back of opposing forces – weaker global stocks but Sunday’s RRR news.

After some initially whippy bond price action immediately out of the payrolls report, Treasury yields continued their March higher, 10s to a high of 3.246% and ending the NY day at 2.2328%. 2s hit 2.8973% before settling at 2.885%: On the week, the significant bear-steepening theme was very much in evidence, with 2s +6.6bp, 5s +11.6bps, 10s +17.2bps and the 30 year up a heady 19.9bps.

Another good day for iron ore and metallurgical coal to round out a strong week for both steel-making components (China production curbs not yet in evidence) while aluminium gave back some of the mid-week gains sparked by fears of a shutdown of the Norsk Hydro plant in Brazil. Copper had another down day to cap a down week and where sharply rising US bond yields look to be taking a toll.

WTI crude was flat and Brent lower Friday (following sharp falls in both on Thursday on reports from Saudi Arabia that OPEC could pump as much as another 1.3mn bpd if there’s demand for it). Both crudes are still higher on the week, by 1.5% (WTI) and 1.75% (Brent).

NY Fed president John Williams on Friday reiterated his view that the U.S. is enjoying a “Goldilocks” economy. The jobs data is “a continuation of a strong U.S. economy” that shows “good momentum going forward,” Mr. Williams said in an interview on Bloomberg’s television channel. “This is a bit of a Goldilocks economy” where growth is strong and sustainable amid an absence of big upward inflation pressures.

The rock-bottom level of the jobless rate will like fall further and go under 3.5% at some point next year, Mr. Williams said. But he isn’t worried that the super low unemployment rate, which historically would be a significant factor that could push inflation up, is a problem. He said of the 3.7% jobless rate: “It doesn’t scare me at all. It’s great for the American people.” Williams said the Fed has a “ways to go” before its rate rises move from being stimulative of the economy to a level that is neutral.

US September non-farm payrolls 134k (185k E)

August NFP revised to 270k from 201k, July revised to 165k from 147k (net +87k)

US September unemployment rate 3.7% – lowest since 1969 (3.8%E, 3.9%P)

US September average hourly earnings 0.3% m/m (0.3%E, 0.3%P revised from 0.4%)

US September average hourly earnings 2.8% y/y (2.8%E, 2.9%P)

US September underemployment rate 7.4% from 7.4%

US September participation rate 62.7% (62.7%E, 62.7%P)

US August trade balance -$53.2bn (-53.6bn E, -50.0P revised from -50.16bn)

Canada September employment 63.3k (25.0kE, -51.6kP); Full/Part time -16.9/80.2k)

Canada September unemployment 5.9% (5.9%E, 5.9%P)

Canada September participation rate 65.4% (65.5E, 65.4P)

Canada August merchandise trade 0.53bn (-0.52bn E, -0.19bn P revise from -0.16bn)

CoreLogic reported a preliminary all capital cities weekend auction clearance rate of 53.7% on Sunday on a bounce back in auction volumes (1,809) following the Grand Final weekend slump last week. Melbourne cleared a preliminary 54.4% against a final 57.1% and Sydney 53.5% vs. a 43.8% final rate last week.

Domestically, The NAB Business Survey on Tuesday is the data focus for the week ahead – Business Confidence has been carefully watched for any adverse impacts from US-China trade risk and the housing slowdown. Other noteworthy data releases include Job Ads (Monday), Consumer Sentiment (Wednesday), and Home Loans data (Friday). There is also a speech from the RBA’s Luci Ellis to an Economic Outlook Conference (Thursday) and the RBA’s biannual Financial Stability Review (Friday).

Internationally, US focus will be on the CPI (Thursday) where the consensus is for core (ex-food and energy) inflation to pick up to 2.3% from 2.2% in August. Also out in the week is the NFIB Small Business Survey (Tuesday), PPI (Wednesday) and Consumer Sentiment (Friday). There are a number of Fed speakers, including Williams again (voter, FOMC Vice Chair) on Tuesday. China returns from ‘Golden Week’ public holidays today with trade data on Friday one focus. September money supply and credit data are also due any day.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.