Price growth edges lower despite reasonable economy

Insight

Markets were on a positive frame of mind at the end of the week,

https://soundcloud.com/user-291029717/risk-on-for-how-long?in=user-291029717/sets/the-morning-call

“You held me down, but I got up (hey); Already brushing off the dust; You hear my voice, you hear that sound; Like thunder, gonna shake the ground”, Katy Perry 2013

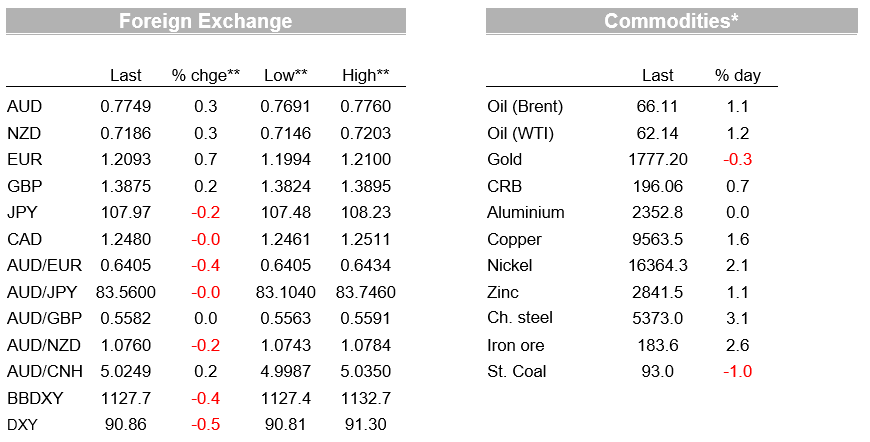

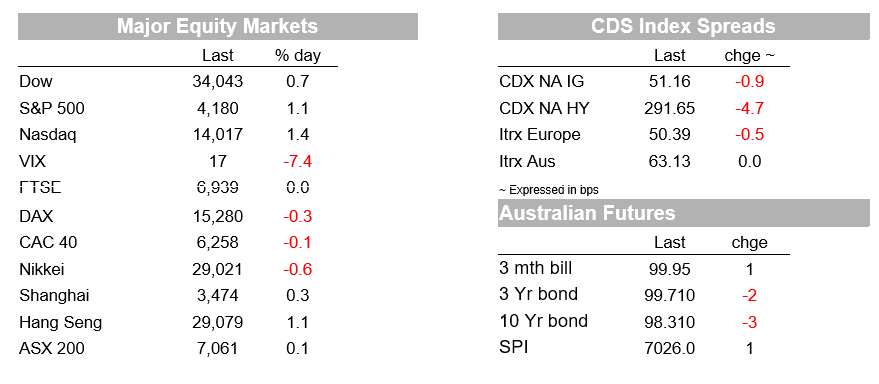

Activity is roaring back on both sides of the Atlantic with the Markit PMIs surprising to the upside in the US, UK and Eurozone. Encouragingly the Services PMI is rebounding sharply with record highs being seen in Services for the US, UK and Australia. The data plays to the view of a sharp rebound in activity once restrictions and Europe’s vaccine rollout should allow that to continue in the months ahead. Equities lifted sharply on the back of the data, with positive earnings also helping. The S&P500 rose +1.1% and ended the week broadly flat at -0.1% in what was a quiet week for data. Improved risk sentiment also saw yields lift a little with the US 10yr yield +2bps to 1.56%, though again in a quiet week are little changed at -1bps. The USD remained on the backfoot with the DXY -0.5% with gains again driven by the Euro with EUR +0.7% 1.2093. Over the week the USD DXY is down -0.8% and EUR is up +1.0%. The AUD also rose against USD weakness with AUD +0.3% to end the week little changed at 0.7749.

The biggest piece of weekend news was US Democratic Senator Manchin again pushing back on Biden’s infrastructure bill as well as re-stating he doesn’t want to use budget reconciliation. Manchin told CNN that he wants a “more targeted ” version of the proposed $2.2 infrastructure package and supports the Republican proposal for a cut down $600bn counteroffer, while also previously stating he doesn’t support he extent of the proposed increase in the corporate tax rate. Note Manchin’s vote is critical if Republicans oppose bills in the Senate, and Manchin has also stated he doesn’t want to use budget reconciliation (see Politico for details). It appears an infrastructure bill appears someway off, as too does further spending plans this side of the mid-term elections in 2022.

Also important for the virus/vaccine track, but not grabbing headline was Pfizer’s CEO stating he is optimistic that the Pfizer/BioNTech vaccine would prove effective against the double mutant ‘Indian’ variant of the virus. Pfizer CEO Bourla in an AFP interview on Friday the Pfizer/BioNTech vaccine’s efficacy against the UK variant as witnessed in Israel was 97 per cent with strong efficacy also seen against the South African and Brazilian variants. Note Pfizer has not compiled sufficient data to fully assess the efficiency of its vaccine against the Indian variant. Also in vaccine news the US re-approved the J&J vaccine for use after an 11 day pause.

As for the data, US data shot the lights out with the US Services PMI lifting to 63.1 against 61.5 expected and highest in at least 11 years. The Manufacturing PMI was also strong at 60.6. New Home Sales also jumped a sharp 20.7% against consensus of 14.2%, with a sharp rebound following the severe winter weather in February which had seen new home sales fall ‑16.2%. Looking forward, a slowdown in mortgage applications since January suggest some easing will occur with such a slowdown occurring on the back of higher mortgage rates, tighter lending standards and perhaps a pivot back to the inner cities as activity starts to normalise.

Across the pond, Euro area PMIs also beat with Services at 50.3 against 49.1 expected despite the recent tightening in restrictions. Manufacturing was also strong at 63.3%. The UK PMIs also beat with Services at 60.1 v. 58.9 expected. Also out in the UK was Retail Sales for March where core sales rose 4.8% m/m against 2.0% expected and illustrative of the sharp rebound in activity as restrictions start to gradually lift.

In FX it was a story of USD weakness, as has been the case for the past week. The USD DXY fell 0.5% with the risk on mood seeing EUR outperform, up 0.7% to 1.2096. The dollar downtrend is likely to continue given the vaccine rollout in Europe is picking up with markets now starting to see the other side of the pandemic in Europe, while further US fiscal stimulus seems further and further away given Manchin (D) wants a smaller stimulus envelope in line with Republicans and is reluctant to use budget reconciliation. The Fed is also not expected to change guidance any time soon, and we will here more at this week’s FOMC meeting. Supportive of a lower USD has been the decline in US 10yr real yields which have fallen by around 18bps since late March to be -0.78%. The AUD broadly followed USD moves with the AUD -0.3% to 0.7749.

A busy week in Australia with focus on Q1 CPI and Weekly Payrolls to see any impact from the end of JobKeeper:

Offshore it’s a crowded calendar with the main highlights being the FOMC, US GDP, EZ GDP, China PMI, BoJ, OPEC, Tech Earnings.

A very quiet day in Australia with a few states having the ANZAC Day Public Holiday (those with a public holiday Monday are QLD, WA, SA, ACT and NT). Offshore it is also fairly quiet ahead of a big week. Germany has its IFO Survey, while in the US, Durable Goods Orders will be one of the final data pieces ahead of Q1 GDP figures on Thursday. Details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.