Price growth edges lower despite reasonable economy

Insight

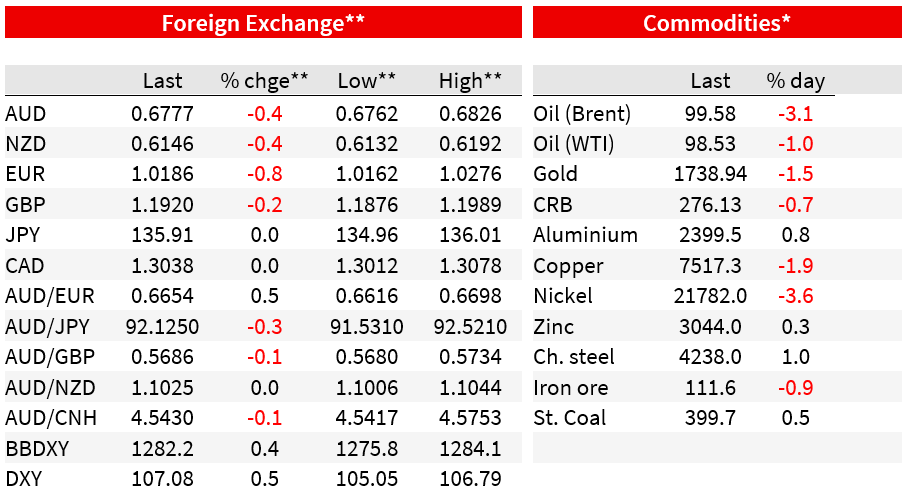

Higher US yields together with a further drop in the EUR sees the USD in DXY terms now at its highest since September 2002.

https://soundcloud.com/user-291029717/significant-risk-still?in=user-291029717/sets/the-morning-call&utm_source=clipboard&utm_medium=text&utm_campaign=social_sharing

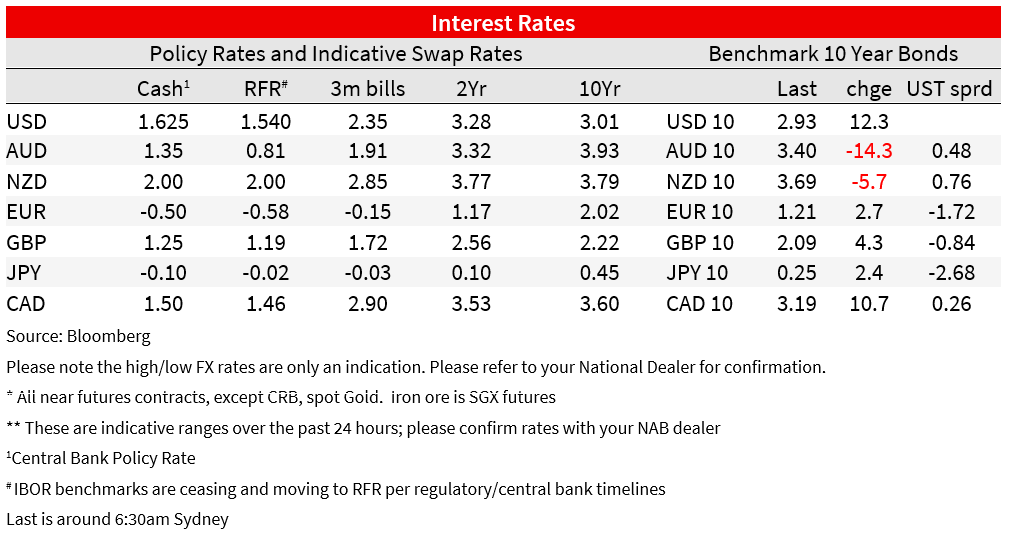

US bond yields are higher across the curve in the last 24 hours but more so at the front end with Tuesday’s 2/10s Treasury curve re-inversion now more pronounced at -5bps. Higher US yields together with a further drop in the EUR sees the USD in DXY terms now at its highest since September 2002. US equities have posted small gains (following much bigger, and somewhat surprising, gains in Europe) amid a somewhat mixed picture from incoming US data.

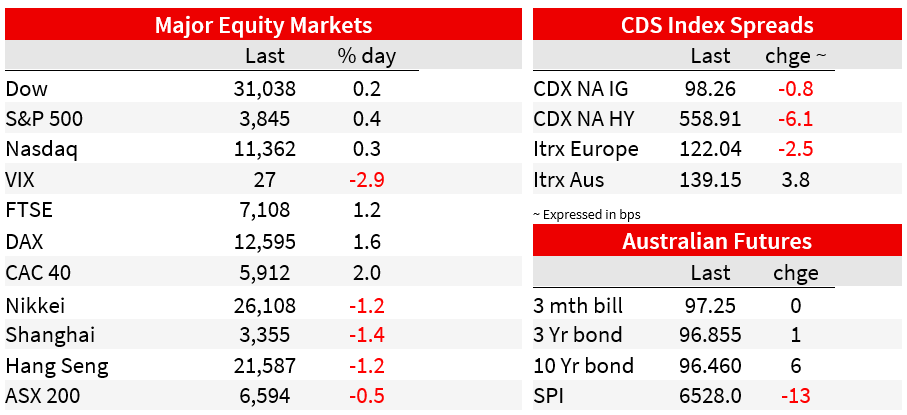

Plenty going on still in markets, no more so than in bonds where the MOVE index (the equivalent of the VIX in the US equity market) is still highly elevated close to this week’s highs and which are the highest levels since the GFC. Overnight, we have seen 10-year yields extending their Tokyo session gains to be 12bps up on Tuesday’s NY close to 2.93% and 2s by a bigger 18bs to 3.00%.

Helping the bond moves and more inverted curve have been the just-released June FOMC Minutes, where the standout sentence appeared to be that ‘Many regarded it as possible than at even more restrictive stance could be appropriate if elevated inflation pressures were to persist’. The Minutes flag a further lift to the FOMC’s central inflation projections on the next quarterly forecast run-through and make clear the July rates decision is about 50 or 75bps (and where a number of FOMC members have of course been out in the past fortnight nailing their colours to the +75bps mast).

Also supporting higher yields has been a better than expected Services ISM report , the headline coming in at 55.3 down slightly from 55.9 but above the 54.0 expected. Most sub-indices were slightly lower, covering new orders, export orders, price paid (to a 9-month low) and employment (sub-50 for the first time since January at 47.4). But overall business activity lifted by 1.6 points and supplier delivery times lengthened slightly, suggestive of ongoing supply bottlenecks (longer wait times for a table at your favourite restaurant, perhaps?).

We also had the latest JOLTS report – a Fed favourite – and while for May so always a little dated, showed 11.3million vacancies, down from an upward revised April read of 11.7mn and meaning there are roughly two job openings for very unemployed person – indicative of a sill uber-tight labour market. The Australian equivalent, incidentally, is about 0.9 vacancies per unemployed person currently in the labour force.

A mixed picture, by sector, for US equities with the small overall gain (0.36% for the S&P 500 and 0.35% for the NASDAQ) led by a 1% rise for the utilities sub-index and 0.9 for Information technology, while energy is down 1.7% (oil off another $1-2 Wednesday) and both financials and consumer discretionaries closing with losses of about a quarter of a percent.

In currencies, further slippage in EUR/USD, by another 0.8% to a low of 1.0162 mean that the DXY USD index has made a new post Sep 2002 high a 107.3 (107.1 now) and where the fears of a major EU energy supply crunch from the potential loss of Russian gas has this week’s jumped to the top of the EUR FX market narrative. All other G10 currencies are also weaker against the mighty greenback but AUD by only 0.4% to 0.6771, so holding above this week’s lows near 0.6760.

Perhaps to some surprise, GBP is one of the least impacted currencies by USD strength, off just 0.2%, albeit to its lowest levels since March 2020 and now languishing beneath $1.20 (1.1922). This is despite the pollical news, where the resignation of (at last count) another 38 Conservative MPs from the government means the almost certain departure of beleaguered prime minister Boris Johnson from 10 Downing Street. The only question is whether this is following his resignation or a rule change by the 1922 back-bench committee that will permit a new leadership challenge (currently only allowed 12 months after the last). If there is one, he wll lose.

One reason GBP is not faring too badly in the view that a new Tory government and chancellor will fast-track fiscal easing (tax cuts) potentially softening the current hit to the economy from shrinking real incomes. Another is more fairly hawkish incoming BoE speak, with Chief Economist Pill saying he was willing to “adopt a faster pace of tightening” in August, albeit dependent on the data between now and then, and Deputy Governor Cunliffe saying the Bank “will do whatever is necessary” to contain inflation.

Read our NAB Markets Research disclaimer. For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.