Price growth edges lower despite reasonable economy

Insight

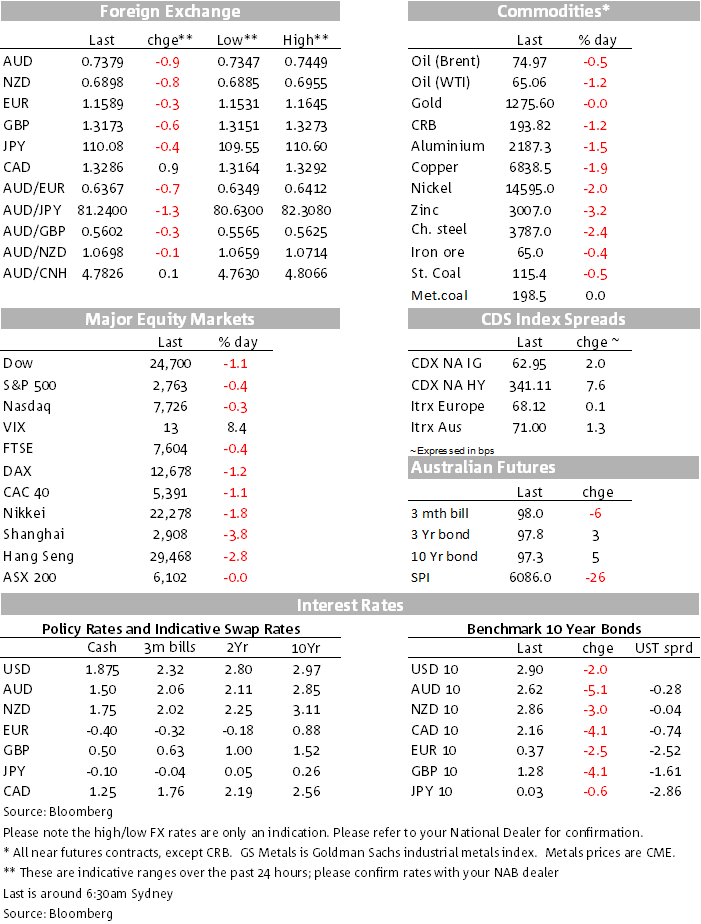

Equities, currencies, bonds and commodities all reacted to more rhetoric from President Trump about Chinese tariffs.

https://soundcloud.com/user-291029717/tariff-talk-hits-harder-but-is-the-bark-worse-than-the-bite

In the FX space, most of the price action of the past 24 hours took place during APAC time in the aftermath of the announcement during the morning that President Trump had called for a list of $200bn of Chinese imports to be subject to an additional 10% tariff. He said he was taking the action because China had increased tariffs on US exports and has no intention of changing its unfair practices related to the acquisition of American intellectual property and technology.

Unsurprisingly, the Chinese responded in forceful terms, noting that if the US loses its sense and publishes a list, China will have to take comprehensive quantitative and qualitative measures and retaliate forcefully.

Those statements were the catalyst for Asian equity markets and the AUD to head south in a classic risk-off reaction, the AUD breaking down through the previous low for the year of 0.7412, through the figure and reaching a low of 0.7347 during the London session, also losing traction on the crosses. The Shanghai stock market was down 4.8% intra-session but managed to claw its way back to a net fall for the day of 3.78%. The AUD has inched its way back up to around 0.7380 as US stocks close down but above intra-session lows.

The Dow has still closed down 287 points, a decline of 1.15%, the S&P 500 by 0.40% and the Eurostoxx 600 by 0.70%. As the AUD was under pressure so were Dalian iron ore and steel rebar futures yesterday along with base metals, the LMEX index ending its overnight session down 1.83%. All base metals on the LME took a sizeable hit, lower by 1¾-2¾%. Oil and gold are also lower as were US soft commodities, including soybeans that were down 2.20%, though even in that market the close was well above its intra-day lows.

To be frank, much of the reaction looks to be catch up to price action in Asia yesterday, rather than another full-blown new round of market risk aversion. The Administration’s trade advisor Peter Navarro has been on the wires saying that the phone lines are open for further discussion with Chinese officials, but that Trump’s actions are a necessary defence of the “crown jewels” of the US economy and that the Chinese have under-estimated Trump’s resolve to secure change in Chinese trade practices.

ECB President Mario Draghi was speaking at the ECB Forum on Central Banking overnight, opening a session on price and wage setting. Less than a week on, the market can hardly be surprised with his comments that “we will remain patient in determining the timing of the first rate rise and will take a gradual approach to adjusting policy thereafter”. He also repeated that “the downside risks to the outlook come from three main sources …..the threat of increased global protectionism prompted by the imposition of steel and aluminium tariffs by the U.S.; rising oil prices triggered by geopolitical risks in the Middle East; and the possibility for persistent heightened financial market volatility.”

What he also served up though was a relatively positive assessment of the Eurozone, saying that the economy is hitting its speed limit, capacity utilization stands above its long-term average in the euro area and in all large economies, and that the current upswing is “job-rich,” but investment has been slow to rise. After all, the ECB did announce last week an end to QE for this year and signal they are thinking of the first move in rates in the second half of next year, not out of keeping with market pricing.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.