Price growth edges lower despite reasonable economy

Insight

Bond yields are back to where they were before the FOMC meeting, says NABs David de Garis, with the focus now back on the reflation trade.

https://soundcloud.com/user-291029717/the-crawl-back-is-done-reflation-takes-over?in=user-291029717/sets/the-morning-call

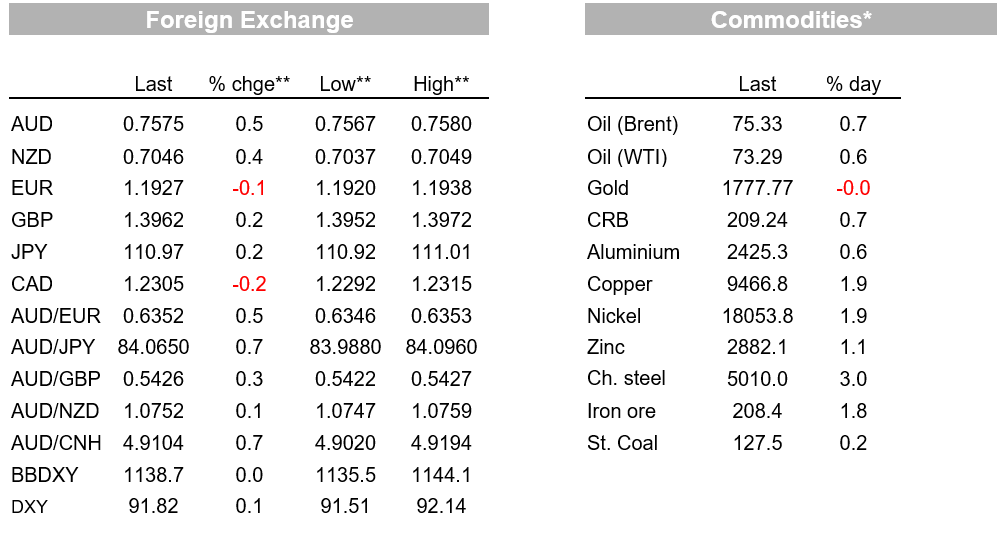

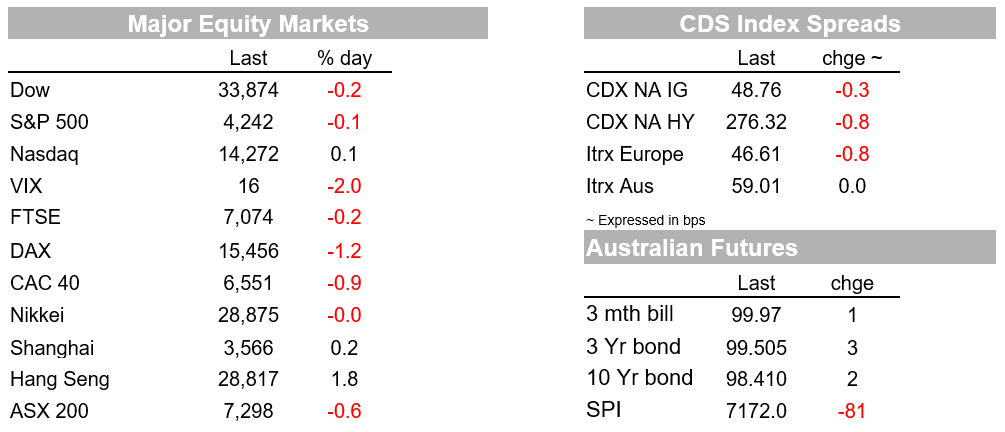

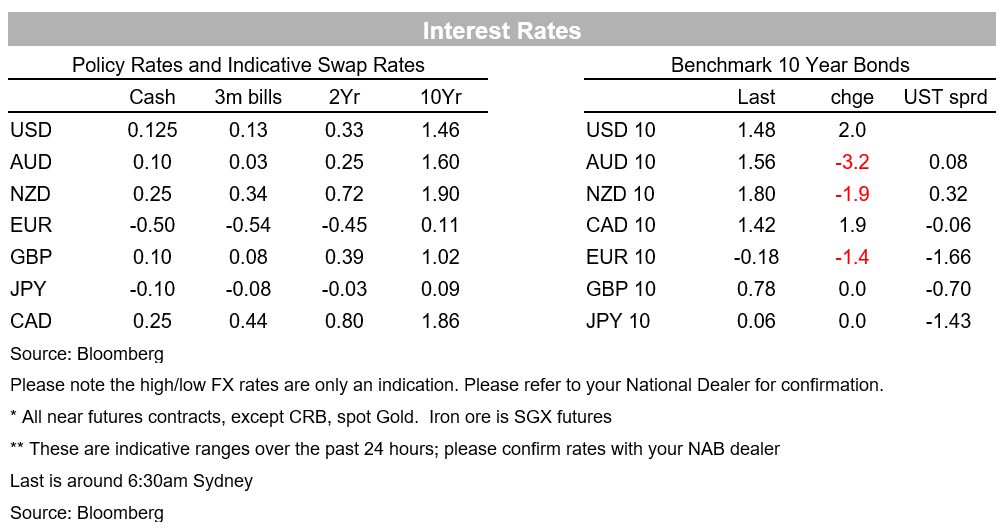

A very quiet overnight with no real news or top tier data to drive. Global PMIs confirmed the rapid recovery continued into June, while the Fed’s Bostic (voter) outed himself as a 2022 hiker. There was no reaction to Bostic’s comments, though for your scribe Bostic’s move from dove to slightly hawkish should be noted and suggests a 2022 hike is a real possibility if the data makes a case for it. Market moves were modest with the S&P500 wavering between +/-, closing at -0.1% and is just 0.4% off its all-time record high. The US 10yr yield also continues to hover around 1.50%, +2.0bps to 1.48% overnight. FX showed the most interesting moves with the AUD (+0.5%) and NZD (+0.4%) outperforming and further retracing their post-FOMC moves. The USD in contrast was little changed (BBDXY +0.0%) with GBP (0.2%), EUR (-0.1%) and USD/Yen (+0.2%). GBP gained a little support on signs that UK-EU will avoid escalating trade tensions.

Fed speak overnight was interesting but not market moving. Normally dovish Bostic (voter) outed himself as one of the seven who pencilled in a 2022 hike and also pencilled in two more in 2023, noting that “given the upside surprise in recent data points I pulled forward my projection”. A September taper announcement is also looking more likely with Bostic suggesting a decision is likely to take 3-4m with the FOMC to define what substantial further progress is. Key to Bostic’s view is that ‘’ The economy is rebounding strongly. Conditions are in place for us to get to a consistent level of inflation that is slightly above our target”. In other words the Fed will likely fulfill their new Average Inflation Targeting Framework and inflation overshoot earlier than previously expected. Given the turn in the former dove, a 2022 rate hike is a very real possibility – note at the June FOMC only 7/18 pencilled in a 2022 hike (see Bloomberg for Bostic’s remarks). Fed Governor Bowman who didn’t speak directly on policy sounded dovish, noting that “there are over 10 million people still without jobs who are either actively looking for employment or have since left the labor force”.

As for data, Global PMIs confirmed the picture of a rapid recovery. The Eurozone Manufacturing PMI was strong at 63.1 (62.3 expected and 63.1 previously), while Services was also robust at 58.0 (58.0 expected and 55.2 previously). Taken together the overall composite is at a 15 year high with the recovery in services confirming that as virus restrictions ease, activity bounces back. There was also widespread anecdotes of price pressures with average input costs for manufacturing second highest in the 23-year history of the survey, while average prices charged for goods and services grew at the fastest pace since 2002. Across the channel the UK PMIs were similarly very strong (Manufacturing 64.2; Services 61.7) and similarly across the pond with the US PMIs (Manufacturing 62.6; Services 64.8). The most interesting anecdote out of the US PMIs continues to be “difficulties finding suitably trained candidates for current vacancies” in both manufacturing and services, in sharp contrast to Fed Governor Bowman’s observation of 10m people who are still without jobs.

On a less positive note, US new home sales continue to fall (-5.9% m/m v. 0.2% expected and -7.8% previously), as foreshadowed by the decline in mortgage applications. Lumber prices also continue to plummet in the US, with the front future now having fallen a cumulative 47.3% since early May. The overall price of lumber though remains elevated relative to pre-pandemic with the front future trading at 879.8 compared to around 400 prior to the pandemic. Why is your scribe talking about US lumber prices? Chair Powell cited lumber as a reason why he thought the pick-up in inflation is likely to be transitory and a continued decline in lumber plays to that view. Powell’s quote was “ The thought is that prices like that have moved up really quickly because of the shortages and bottlenecks and the like….They should stop going up and at some point, in some cases should actually go down. And we did see that in the case of lumber.”

As for other commodities overnight, they have been generally firmer. Copper prices bounced 1.9% after China’s first sale of copper from its strategic reserves was smaller than expected. Crude oil prices have moved slightly higher, with Brent trading around $75/barrel, after the weekly DOE report showed a substantial, 7.6 million barrels, drawdown in crude oil inventories in the US. The onset of the summer driving season in the US is expected to add to demand pressures. Oil prices though did pulled back from the day’s highs after Saudi Arabia’s Energy Minister said that the OPEC+ cartel had a role to play in “taming and containing inflation”, potentially foreshadowing future supply increases.

In FX, commodity-linked currencies have continued to recover from their post-FOMC sell-offs, supported by the broadly positive backdrop in commodity and risk markets. The AUD (+0.5%) and NZD (+0.4%) are top of the currency leader board. Importantly the AUD has shown little reaction to the latest COVID-19 outbreak in Sydney which involves the more transmissible delta variant. Additional restrictions were put into place at 4pm yesterday. It is hoped the outbreak can be contained within a short timeframe as has been the case previously. Compared to prior outbreaks, vaccination is picking up with doses equivalent to around 26% of the population having been given, though this comprises mainly first doses with only 3.4% of the population full vaccinated. Until vaccination reaches 60-75% of the population (pencilled in by late this year or early next year), Australia remains vulnerable to COVID-19 outbreaks. We do not see the outbreak as having any policy implications. Note NZ is also on alert after an Australian traveller tested positive and visited a number of tourist spots in Wellington with the Wellington now on COVID Alter Level 2 until Sunday.

The other piece of Australian news worth noting from yesterday is the RBA pushing back on hawkish notions with Assistant Governor Luci Ellis emphasising “achieving full employment is an important national priority” and that full employment is a pre-condition to having wages growth strong enough for inflation to be sustainably within the 2-3% target (see RBA Ellis speech for details ). That speech came in the wake of some economists shifting to hikes in late 2022 and early 2023. NAB’s view is that while we can see a probability of the RBA moving in H2 2023 and markets should price in this risk, given the high bar the RBA has given itself on wages growth being sustained at 3% plus, we currently pencil in 2024 as being more likely. Our view is also predicated on the RBA sticking to its recent evolution in monetary policy, that being trying to achieve the maximum sustainable employment by waiting for actual inflation to be sustainably in the band before tightening, instead of hiking on a pre-conceived notion of where NAIRU is.

Domestic focus on will be on virus numbers in Sydney amid a quiet day for data and events. Offshore focus will be on the BoE MPC Meeting as well as US Fed speak with six speakers on the roster.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.