Labour market strong, housing supply falling behind

Insight

The markets lost a chunk of optimism last week.

And then you say You drive me nervous, nervous

And then I said You drive me nervous, nervous, nervous, oh – Alice Cooper

After the sharp declines on Thursday, European and US equity markets had a good Friday posting positive gains for the day. The seesaw price action, however, pointed to a high degree of uncertainty, investors remain concern over the risk of a new round of containment measures as US infections continue to rise. News over the weekend validate this view with 22 US States recording a rise in infections and part of Beijing going into lockdown following an outbreak in a food market. AUD and NZD managed to post modest returns on Friday but USD indices closed stronger on the day and the week. Longer dated UST yields also edged a little bit higher, but not enough to reverse the big declines over the week. Early Monday trading shows JPY stronger while AUD and NZD are softer.

The good news from European and US equities is that they managed to rebound on Friday after the sharp declines recorded on Thursday. The change of mood on Thursday was triggered by Fed’s sobering assessment of the US economy and officials concerns over the economic outlook and the US labour in particular. This souring mood was exacerbated by reports of an increase in infection rates in many US states, particularly in the South. The lack of major news on Friday likely played into the improvement in sentiment, we also had President Trump’s top economic aid, Larry Kudlow, saying “the US won’t shut down again and it’s not seeing virus returning in second wave”. Offering a wary perspective, Dr. Fauci, the director of the National Institute of Allergy and Infectious Diseases, cautioned US States to rethink their reopening strategies if they see increases in the number of people hospitalized with Covid-19.

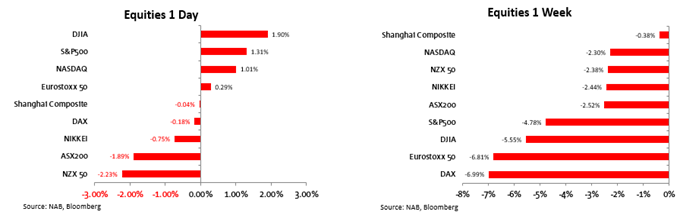

Main US equities indices ended the day with positive returns after enjoying big gains at the open, given them back twice before ending the day in the green. The S&P 500 closed up 1.31% with financials and energy, the big losers on Thursday, at the top of the leader board. Still when we look at the weekly performance, it was not a good week for global equities, reflecting a bit of a reality check, after a period of exuberant gains. The Stoxx Europe 600 Index gain 0.3%, a weekly drop of 5.7% the worst since March 13. The S&P 500 was down 4.78% and S&P/ASX200 was -2.52% for the week.

News over the weekend has done little to ease concerns over the risk of a new round containment measures. Florida’s cases outpaced the week’s average for a fifth day, 22 US States have recorded an increase in their infections over the weekend and part of Beijing has gone into lockdown as a virus outbreak was detected at a food market. As economies reopen, an increase in infection rates is to be expected, the question is whether detecting measures will be efficient enough to allow for localised containment measures without having to shut the whole economy again. China could be the template to watch here.

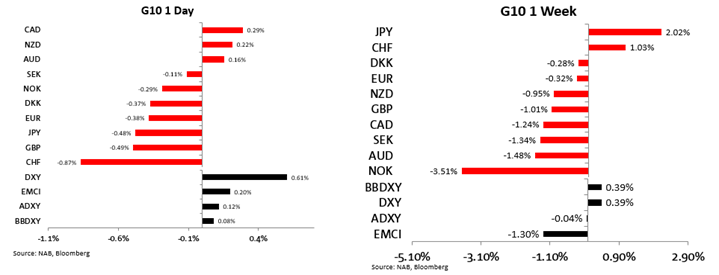

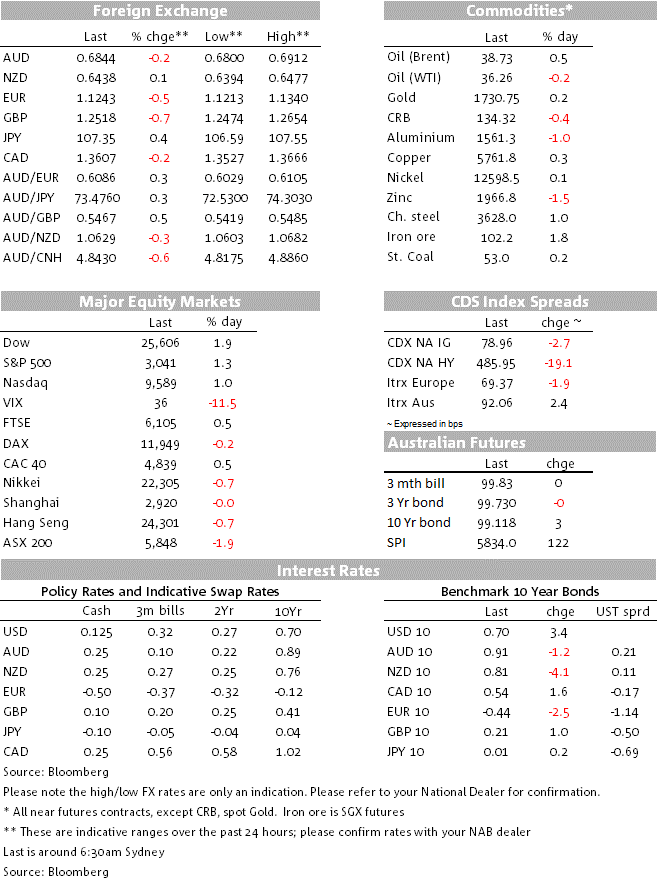

Price action on Friday was mixed and there was a lack of a uniform theme. Commodity linked currencies reflected the improvement in risk sentiment evident in the equity markets with the CAD (+0.29%), NZD (0.22%) and AUD (0.16%) the USD outperformers on the day. After almost trading below the 68c mark during our APAC session, the AUD traded to an overnight high of 0.6912 following the strong US equity open, but then the pair traded down to 0.6813, before ending the day at 0.6855. The kiwi followed a similar price action, after going sub-0.64 during our Friday session, it recovered to around 0.6475, before ending the week at 0.6445. For the week the AUD loss 1.48% while the NZD was -0.95%.

EUR and GBP were on the soft side of the ledger, ending down 0.4-0.5% for the day to 1.1255 and 1.2540 respectively. The UK formally rejected the option to extend its post-Brexit transition period beyond the end of this year. Brussels said that it accepted Britain’s decision as final. Negotiations on a trade deal step up soon with weekly formal meetings beginning towards the end of the month. Meanwhile, UK data releases were not a nice reading. GDP shrank by a record 20.4% in April (on track for its weakest peacetime performance since the “Great Frost” of 1709), ahead of the next Bank of England meeting this week, with expectations odd a further increase in QE. Euro area industrial production plunged 17.1% in April, taking the fall since February to 27%, with the biggest hit being taken by the larger countries. The hope is that April should represent the nadir in activity, given the easing of lockdown restrictions.

So in spite of a mixed performance against G10 pairs, USD indices still managed to record a positive day on Friday (DXY +0.61%) and gains for the week (DXY and BBDXY +0.39%). Only JPY and CHF, the safe haven pairs, managed to outperform the USD on the week. News over the weekend has triggered a cautious opening to the new week with both AUD and NZD down a tad to 0.6842 and 0.6443 respectively.

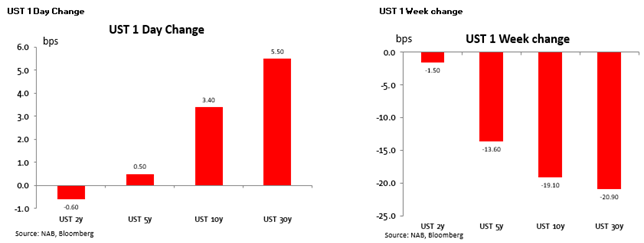

The UST curve steepened on Friday with the 10y Note up 3bps to 0.7034% and the 30y Bond up 5bps to 1.4568%. On the week however yield gains on Friday were not enough to undo the big flattening of the curve during the week ( see chart below).

The preliminary June University of Michigan consumer sentiment survey rose to 78.9 from 72.3 in May. That was better than the 75 expected by consensus, likely reflecting improved optimism as the US economy reopened during the month. Worth noting however, that sentiment remains at subdued levels and it remains to be seen if rising US infection rates across states which could once again spook the consumers.

The Fed released its semi-annual report to Congress on Friday (speaks before Congress on Tuesday night) and in a similar vein to the FOMC and Powell press conference, the report noted “The outlook for the pandemic and economic activity is uncertain. In the near term, risks associated with the course of COVID-19 and its effects on the U.S. and global economies remain high,” adding that “A wide variety of data reveal an alarming picture of small business health during the COVID-19 crisis.

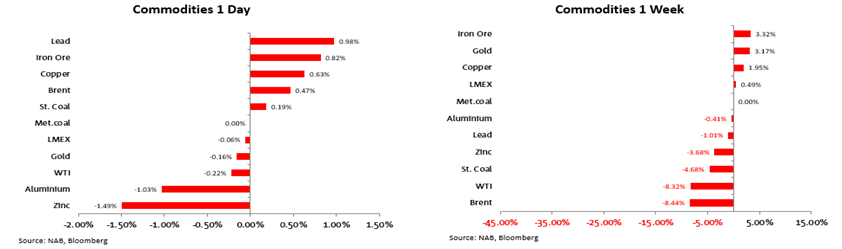

Oil prices ended Friday mixed (Brent +0.47%, WTI -0.22%), but down just over 8% for the week. This week’s price action was a combo of renewed concerns over elevated US inventories and mixed signals from OPEC and friends over the prospect of lower production over coming months. Iron ore was the outperformer o Friday (0.98%) and for the week (+3.32%).

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Labour market strong, housing supply falling behind

Insight

Discover how to take advantage of opportunities in the US Private Placement (USPP) market.

Video

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.