Price growth edges lower despite reasonable economy

Insight

The NZ dollar saw the biggest currency move over the last 24 hours.

https://soundcloud.com/user-291029717/the-kiwi-flies-powell-stands-still?in=user-291029717/sets/the-morning-call

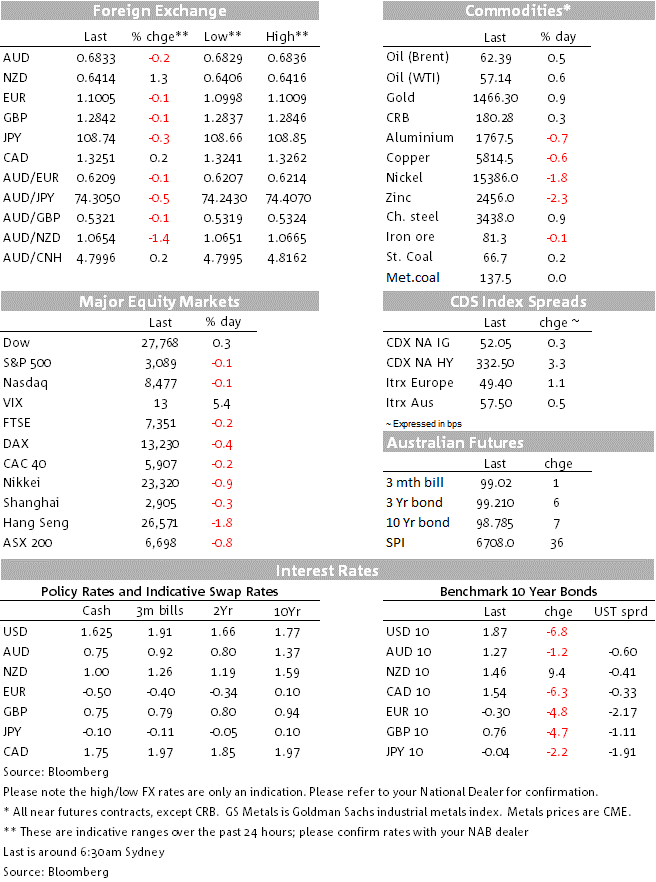

In the words of Major Lazer’s 2016 hit “Cold Water”, markets had two does of “cold, cold water” with the RBNZ holding rates against markets pricing in an 80% chance of a cut, while optimism over an interim US-China trade deal has faded somewhat after a WSJ article reported “trade talks hit snag over farm purchases”. In terms of market moves, the NZD surged after the on hold RBNZ decision, with the Kiwi taking flight +1.3% and hitting a high of 0.6417. Those gains were sustained overnight with the NZD currently trading at 0.6414. Kiwi rates also saw sharp moves with 2yr swap rates up 15bps to 1.20%, while 10yr yields rose 9bps to 1.61%. Moves in other FX pairs in contrast were more moderate with the USD (DXY) unchanged at 98.35 with small declines in EUR (-0.1% to 1.1005) and GBP (-0.1% to 1.2842) offset by a moderate move lower in USD/JPY (-0.3% to 108.74). The AUD was also little moved (-0.2% to 0.6833), though the AUD/NZD cross has fallen -1.4% to 1.0655. Global yields have moved lower, though there was no clear catalyst apart from fading trade optimism with US 10yr yields -6.8bps to 1.87%.

In what was a close decision, the RBNZ kept rates on hold at 1.0% with an easing bias (“further add monetary stimulus if economic developments warranted”). Emphasising how close the decision was RBNZ Governor Orr stated this morning that “it was without doubt a tough decision to hold rates”. With markets having gone into the meeting pricing in an 80% chance of a cut, there were sharp moves in FX (NZD +1.3%) and Rates (2yr swap +15bps). Also adding to the sustainability of the knee jerk reaction was some notion that the RBNZ could be on hold for a while with my kiwi colleagues at BNZ noting that the key to the RBNZ’s reluctance to reduce its cash rate stemmed from its revised view on the economy’s potential growth rate: the RBNZ’s potential growth rate track now troughs at 2.2% in 2021, which means that any growth in excess of 2.0% will likely start to see inflation rise. BNZ now sees rates remaining on hold at 1.0% for the foreseeable future, with the risk skewed to another cut if economic conditions materially weaken.

Initially it was driven by President Trump’s remarks the day before yesterday who said “if we don’t make a deal, we’re going to substantially raise those tariffs”. Subsequently a WSJ article notes that “talks hit snag over farm purchases” with China reportedly cautious on “putting a numerical commitment [on farm buys] in the text of a potential agreement….Beijing wants to avoid cutting a deal that looks one-sided in Washington’s favour”, while Chinese officials have also resisted US demands for a strong enforcement mechanism for the deal and curbs on technology transfers for companies seeking to do business in China (see WSJ article for details).

The Fed’s Powell gave his usual testimony to Congress with remarks very similar to his October FOMC press conference. He noted again that he sees “the current stance of monetary policy as likely to remain appropriate as long as incoming information about the economy remains broadly consistent with the outlook” and of course is ready to adjust policy if developments were to occur that caused a material reassessment of the outlook.

US data had little impact on markets with Headline CPI above expectations, but Core CPI at consensus. Headline came in one-tenth above consensus at 0.4% m/m against 0.3%, while core was in line at 0.2% m/m though it was a low 0.2 which saw the year-ended miss a tenth at 2.3% y/y. There were a whole host of volatile components with apparel prices falling sharply (-1.8% m/m) along with lodgings (-3.8% m/m), while there were strong increases for vehicles (+1.3% m/m), medical care serves and recreation services. Overall the data suggests core inflation in the US remains contained.

Global bonds rallied with US 10yr yields -6.8bps to 1.87%. Most of the move occurred as London opened with no specific catalyst apart from fading optimism around an interim US-China trade agreement. Equities also pared gains on the fading optimism with the S&P500 -0.1% to 3,089. Equities in Asia continue to be buffeted by unrest in Hong Kong with the Hang Seng -1.8%.

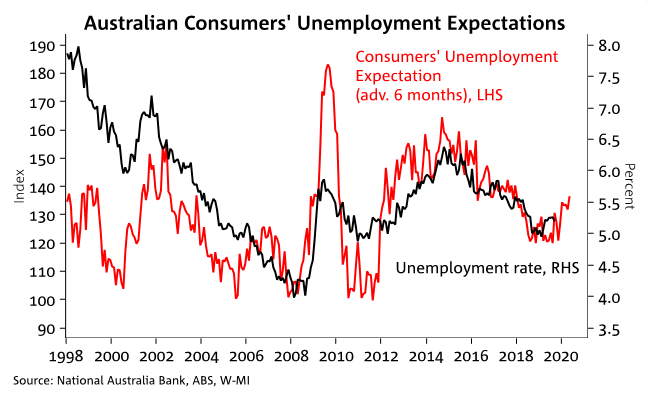

An as expected wages print had little impact on markets with WPI at 0.5% q/q and 2.2% y/y. That pace of wages growth is in line with the RBA’s now downgraded wages outlook where the RBA forecasts wages growth stalls at 2.3% y/y until at least the end of 2021. Low wages growth likely reflects spare capacity, as well as notions of a global market for labour. It is also worth noting that wages growth of 2.2% is inconsistent with the RBA’s 2-3% inflation target – if it was than consumers would be having real wage cuts. Interestingly for businesses the data also hints that companies are tilting more remuneration towards bonuses (which can be varied with the fortunes of the business) with private wages including bonuses rising 3% in annual terms. Also out in Australia was the W-MI Consumer Confidence measure which rose 4.6% in November to 97.0. More interesting though was the unemployment expectation out of the survey which rose to its highest level since 2017 (see chart below).

A very busy day ahead both domestically and internationally. Domestic focus will be on October Employment data. Focus then shifts to Chinese activity indicators and then to Europe for German Q3 GDP. In the US the Fed’s Powell is also speaking again along with seven other Fed officials.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.