Labour market strong, housing supply falling behind

Insight

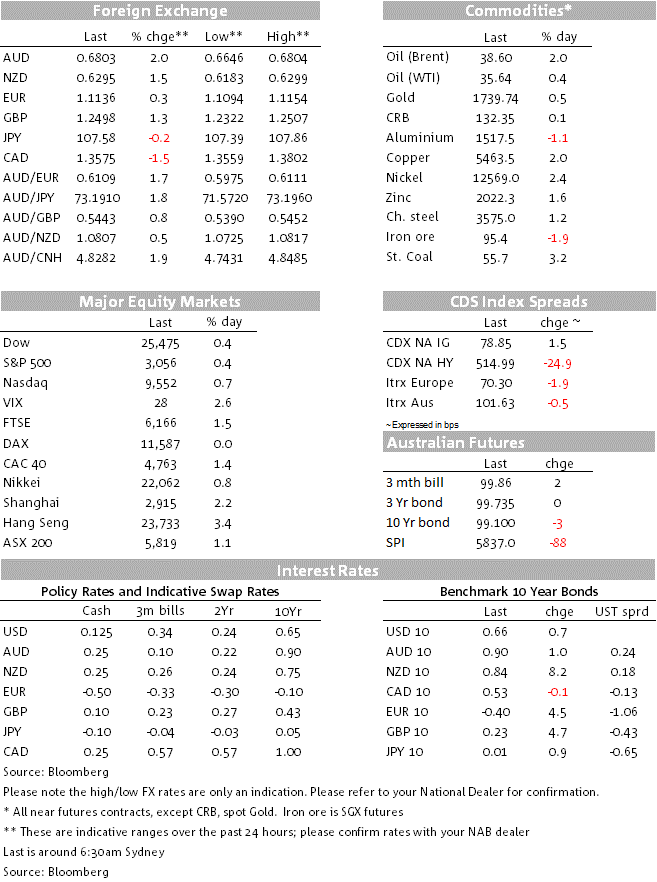

The Australian dollar has climbed even higher this morning, reaching 68 US cents.

https://soundcloud.com/user-291029717/the-rise-and-rise-of-the-aussie-dollar?in=user-291029717/sets/the-morning-call

The AUD/USD was languishing beneath Friday’s night’s closing highs of 0.6668 and US stock market futures were down about 1.5% by way of first response to the scenes unfolding across America and which filled the world’s TV screens throughout the weekend. Fast forward less than 24 hours and the S&P 500 has closed up 0.4%, the NASDAQ 0.7% and AUD/USD has spent time above 0.68 (high of 0.6803) last seen on January 27.

The DXY index is down a further 0.5% to 97.8, its weakest level since March 16 but the AUD’s percentage gain on Friday night’s close is four times that. The flattening of tail risks related to a potential Emerging Market blow-up have receded with the White House response to China’s approval of a new Hong Kong security law which leave the Phase 1 US-China trade deal intact; China PMI data on Sunday, where strength in Construction and Steel PMIs was most notable, was augmented yesterday by a better than expected Caixin manufacturing PMI (50.7 from 49.4 and the 49.6 expected); and commodity prices – iron ore in particular – have been on a tear.

While we are always at pains to point out that day-to-day volatility in the iron ore price has scant influence on the day-to-day performance of the AUD, there is no denying that the rise from below $92 to above $97 (referencing the Singapore futures contract, and to above $100 on other benchmarks) has had a hand. So too the $30 rise in the gold price since the middle of last week. Risk sentiment, both in terms of the ongoing US equity market rally but also vis-à-vis the risk metrics most relevant for the AUD, have also continued to improve.

Just after we left off yesterday was a news report that China’s state owned enterprises had been ordered to stop buying some US agricultural products, soy beans in particularly, which ostensibly means that the Phase 1 trade deal may not be sacrosanct – for both sides – after all. Yet the bounce in USD/CNH on the news, from 7.13 to 7.15, has since been more than fully retraced. Something to watch for sure, but for now not undermining the AUD rally. CAD and NZD have been the next best performing G10 currencies, both up around 1.5% versus 2% for the AUD, followed by GBP (1.2%) and where they are a few news snippets around suggesting that all might not be lost with respect to the fate of the next round of UK-EU trade talks that are due to get underway later today.

The recovery in US stocks has not been significantly undermined by news that third-phase trials of Gilead’s Remdesivir anti-viral drug have been disappointing, its stock only off about 2.5%, which perhaps tells us that the stock market rally is not founded on (misplaced?) hopes for the early development and roll-out of a vaccine.

Government bond yields are higher across the board since the weekend, European benchmarks for the UK, France and Germany all up 4-5bps at 10 years but Italy by only 1bps, the same as for the US 10-year note.

Economic news has been dominated by PMIs data – the US manufacturing ISM and either first and only or final European PMIs. The pan-Eurozone manufacturing PMI was little changed on the ‘flash’ estimate at 39.4 (from 39.5) with little change in the French or German readings, but Italy (no flash estimate) bounced from 31.1 in May to 45.4. Still in contraction territory for sure, but evidence that the first big European country to start exiting from lock-down – being the first in – is the first to see its activity readings becoming significantly less bad. The UK manufacturing PMI was little changed at 40.7 from 40.6.

The rise to 43.1 from 41.5 was once again flattered by the strength of the supplier deliveries sub-index, albeit down to 68 from 76 (reflecting ongoing supply chain disruptions) with orders up to only 31.8 from 27.1, production to 33.2 from 27.5 and employment to 32.1 from 27.5 – all still deep in contraction territory. Also out in the US, April Construction Spending was down by much less than expected, -2.9% vs. -7.0% consensus, with residential activity holding up the overall reading but doing nothing to assuage concerns about the outlook for non-residential activity, office and other commercial developments in particular.

RBA at 14:30 AEST. No change to either the 0.25% cash rate or 0.25% 3-year yield target are expected.

Governor Lowe recently testified before the Senate, where he said the economy was tracking a little better than the Reserve Bank’s baseline scenario. However, the Governor noted even the bank’s upside scenario was “pretty depressing”, with unemployment high for years. Given this outlook, easy monetary policy was locked in for some years, but Lowe noted his “main concern is that we don’t withdraw the fiscal stimulus too early”.

In particular, Lowe noted many key government assistance programmes were scheduled to end in September, making this a “critical” point in the economy. As such, Lowe remarked that the government might need to extend its JobKeeper wage subsidy scheme and spend more on infrastructure, depending on how the economy was tracking at that point. Governor Lowe emphasised that the recovery depends on health outcomes and how quickly confidence is restored. As such, the RBA should keep policy unchanged as it continues to monitor the recovery.

Q1 GDP partials for net exports, public spending and and inventories (11:30 AEST) ahead of GDP on Wednesday where NAB forecast -0.1% QoQ (consensus -0.4%). We expect:

There is nothing of particular note offshore this evening.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Labour market strong, housing supply falling behind

Insight

Discover how to take advantage of opportunities in the US Private Placement (USPP) market.

Video

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.