Price growth edges lower despite reasonable economy

Insight

Markets are hopeful that a deal will be reached between the US and Mexico, and tariffs will be avoided.

https://soundcloud.com/user-291029717/too-much-oil-hope-for-mexico-and-ecb-on-hold?in=user-291029717/sets/the-morning-call

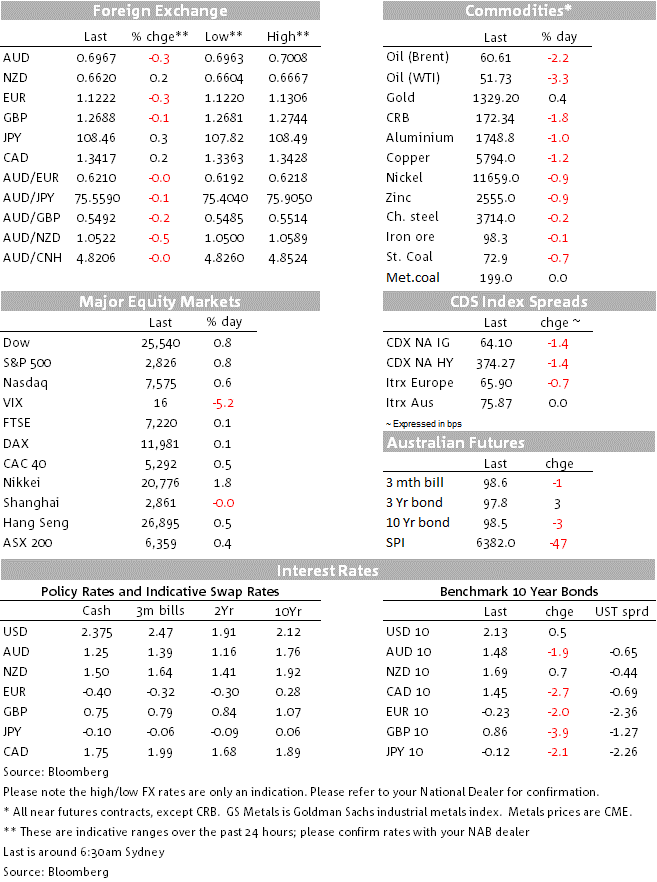

Just like last night’s State of Origin opener, score wise it was very much a game of two haves in markets overnight, some quite extreme volatility caused by two pieces of economic news: first a very weak ADP Employment report, but followed soon thereafter by a stronger than expected US non-manufacturing ISM survey (56.9 up from 55.5) and where the strength in the employment sub-component was one of the standout features. A fresh slide in oil prices after the Energy Information Administration (EIA) reported the strongest build in crude oil and oil product inventories since 1990, is the other big market story.

ADP employment is a notoriously unreliable guide to the non-farm payroll report that comes 48 hours later, but with the number printing at just 27k (the lowest since September 2010) it is not so readily dismissed as guide to which side of the market consensus the official numbers are likely to print on Friday. And while the employment sub-component of the non-manufacturing ISM rose by 4.4 points to 58.1, consistent with still-strong employment growth, this tends to be a better two month lead rather than concurrent indicator of payrolls. As a result, NAB’s own forecast for tomorrow night’s release is 160k (our model that includes ADP wants +140k while one that excludes this is pointing to +237k). There may also be some (negative) weather related factors at play in May (payback from a weather-related boost in April). Hence our low ball forecast.

We have also just had the Fed’s ‘Beige Book’ summarising regional US economic conditions in front of the next (18-19th June) FOMC meeting, which overall shows a modest pick-up in growth in April and May relative to earlier in the year and as yet little by way of hurt being caused by tariffs. .

The US numbers produced some big moves in US bond markets. Immediately following ADP and the EIA inventories data – latter showing a 6.8 million barrel build in crude stocks – US 10-year yields hit a low of 2.08% and the 2-year note a low of 1.77% (from 2.12% and 1.85% respectively beforehand). The US dollar swiftly lost 0.4% in DXY terms. The moves were fully reversed- and in the case of the dollar more than reversed – soon after the ISM report, 2-year yields now back to 1.85%, 10s to 2.13% and the DXY index now 0.3% up on this time yesterday

In terms of currency specifics, NOK is the weakest G10 currency, unsurprising given the scale of the oil price fall, now -$1.70 for WTI and -$1.39 for Brent crude, the latter briefly back below $60 for the first time since January. The NZD, currently 0.6617, is the only G10 currency currently up on the US dollar versus 24 hours ago, though back from the APAC session high of 0.6667 seen after yesterday’s reported comments from RBNZ deputy governor Christian Hawkesby – delivered a week ago – that “rates will remain broadly around the current level”. GBP is little changed; having drawn a modicum of support from a slightly better than expected services PMI (51.0 from 50.4). President Trump, in Ireland, again waded into the Brexit debate, telling Ireland’s Taoiseach, Leo Varadkar, “I think it will all work out very well, and also for you with your wall, your border”. He doesn’t quite get this one, does he?

AUD/USD spent some more time back on a 0.70 handle last night (high of 0.7008) before succumbing to post-ISM data US dollar strengthening, currently 0.3% lower to 0.6968. There was also a Terry McCrann article out soon after midday London time saying that only a seriously strong jobs report on Thursday week now stands in the way of another rate cut and that a seriously bad report could deliver a 50-point cut.

As for the US Mexico border and the threat of the first tariffs on US imports from Mexico coming into effect next Monday, talks on border issues began Wednesday with White House trade advisor Navarro saying that the US had a three-part “solution” for Mexico ahead of the meeting. He said Mexican officials still have time to prevent the US tariffs from taking effect by agreeing to steps such as taking asylum seekers and increasing resources at the border. Trump tweeted that he wasn’t bluffing about putting tariffs on Mexico and while Congress questions the emergency powers that Trump will invoke to put on the tariffs, it appears that there is little it can – or is willing – to do to prevent the tariffs, at least initially.

Equity markets have built on Tuesday’s strong rebound with the major indices closing between 0.6% (NASDAQ) and 0.8% higher (S&P500 and the Dow). It is though the defensive sectors that have led the rally – utilities, consumer staples and real estate – with energy stocks the main drag, as you would expect given the oil price slump.

Australia April trade balance (NAB: +$5.4b; mkt: +$5b)

German April factory goods orders (expected 0.0% after +0.6% in March)

EZ Q1 GDP (final, preliminary was +0.4%)

The ECB meets this evening and will be releasing new staff forecasts for inflation and GDP. Realised CPI outcomes have undershot the ECB’s latest forecasts so it is likely there will be downgrades to their inflation forecasts. It is also clear that the growth slowdown is not as transitory as the ECB first thought with trade tensions more persistent – here Germany is especially vulnerable given exports make up around 47% of GDP). At today’s meeting further details around the next TLTRO are likely to dominate, though speculation will continue on whether the ECB needs to contemplate further policy easing (such as restarting QE, though any such decision would likely need to wait until the next ECB President is in the chair).

The US has the April trade balance and weekly jobless claims

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.