Price growth edges lower despite reasonable economy

Insight

In Europe they’ve nicknamed last night as 'Turnaround Tuesday as stocks regained much of their losses.

https://soundcloud.com/user-291029717/it-was-turnaround-tuesday-yet-the-squabble-continues?in=user-291029717/sets/the-morning-call

KangaNews Survey of Australian Fixed Income Investors

The annual KangaNews survey is now open. If you’re an Australian-based Fixed Income investor and value the research provided by NAB’s Economics, Fixed Income (ACGB, Semi, Swap and Credit), Securitisation and FX teams, could you please participate in this year’s poll here. Please note this survey encourages all participants to vote, not just one vote per institution.

Trump comments from yesterday suggesting a successful trade deal seems to have had some positive influence on the market overnight. He told reporters “we’ll let you know in about three or four weeks whether or not [the trade talks] was successful. … But I have a feeling it’s going to be very successful.” He followed that up with a number of trade-related tweets overnight including “when the time is right we will make a deal with China. My respect and friendship with President Xi is unlimited but, as I have told him many times before, this must be a great deal for the United States or it just doesn’t make any sense.”

He also tweeted that “We can make a deal with China tomorrow, before their companies start leaving so as not to lose USA business, but the last time we were close they wanted to renegotiate the deal. No way! We are in a much better position now than any deal we could have made. Will be taking in Billions of Dollars, and moving jobs back to the USA where they belong. Other countries are already negotiating with us because they don’t want this to happen to them. They must be a part of USA action. This should have been done by our leaders many years ago. Enjoy!” And again later, taking another dig at the Fed, “China will be pumping money into their system and probably reducing interest rates, as always, in order to make up for the business they are, and will be, losing. If the Federal Reserve ever did a “match,” it would be game over, we win! In any event, China wants a deal!”

China’s Foreign Ministry responded to US accusations that it had reneged on previously agreed commitments in the negotiations saying that the US had made a last-minute demand that it increase its purchases of US goods. A spokesman for China’s foreign ministry said “the hat that . . . violates promises is absolutely not on the Chinese head.” Markets are likely to remain volatile in the lead-up to the end-June G20 in Osaka, Japan, where Trump and Xi are expected to meet. There was also an interesting take from the FT suggesting that rather than China reneging on its commitments in the draft doc, it was the US who suddenly raised the volume of goods it wanted China to buy from it.

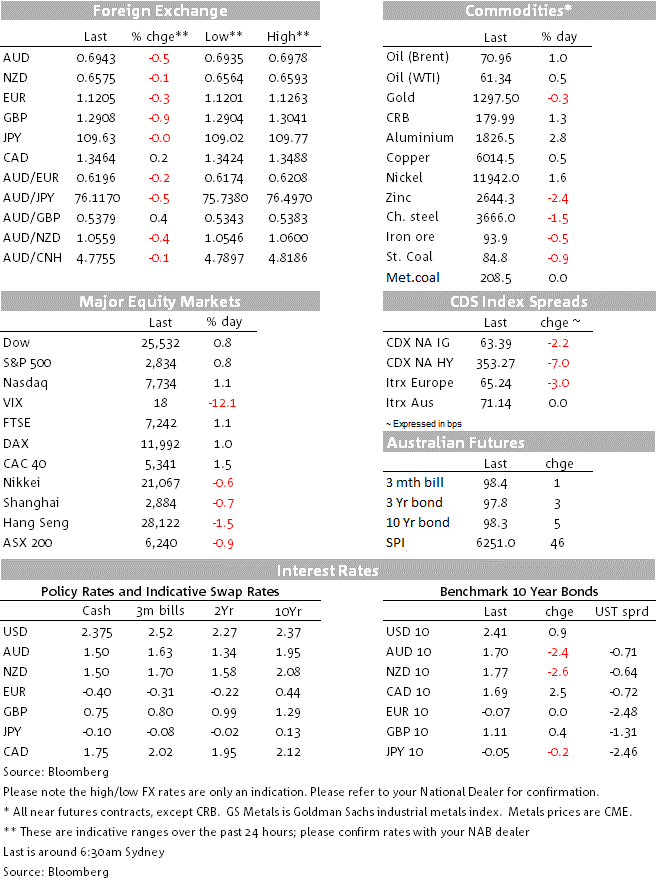

The S&P 500 has closed 0.8% higher for the session, following a 1.01% rise in the Eurostoxx 600. Base metals made some gain (copper rose 0.27%), also retracing some the losses at the start of the week. US Treasury yields also ticked marginally higher, though the market continues to price in a cut from the Fed by the end of the year. An increase in world oil prices overnight has added some support to the CAD that made some limited gains against the US dollar.

Speaking overnight, Fed President Robert Kaplan was speaking of the tariffs as “sand in the gears” for trade firms, injecting a degree of uncertainty, but “will this be for an extended period?”. “We’ll have to see how it unfolds. We just don’ know yet.” Both John Williams (NY Fed President) and Esther George (Kansas City Fed President) were urging patience, Williams saying that policy is in a good place, George saying the “wait-and-see approach is appropriate”.

US Treasury yields have ticked higher by 1-2bps, while German bunds were unchanged at the 10 year tenor at -0.07%. The exception in Europe was Italian bonds, yields there rising a little after suggestions from one of the country’s two Deputy PMs, Mr Salvini (Lega Nord), that the country was willing to break the EU’s debt rules.

Salvini said “if we need to break some limits, like the 3% (deficit to GDP) or 130-140% (debt to GDP ratio), we’re ready to go ahead. Until we arrive at 5% unemployment, we will spend everything that we should and if someone in Brussels complains, that won’t be our concern.” For the record, Italy’s unemployment rate is currently above 10%. Italian short-dated bond yields also moved higher in response to the remarks, with the 2 year Italian yield 6bps higher to 0.68%, its highest level this year, although it is over a percent lower than the level reached mid last year.

The Euro dipped in response and has been an under-performer overnight, down 0.25% sicne yesterday afternoon, currently trading at close to 1.12, the AUD/EUR at just below 0.62.

This morning, the AUD/USD trades not far above its lows for this week, trading at 0.6943 and on the back foot. It’s still 0.13% below late yesterday afternoon (as is the Kiwi at 0.6574 with the yen pretty much unchanged overnight, still comfortably down into the 109s, if off its opening lows for the week.

Elsewhere on the currency front, the Chinese Renminbi has been relatively stable after its fall on Monday.

There was only second tier data out overnight. The May ZEW Investor Sentiment survey for Germany and the EC was released showing still drab expectations and down from May. The German survey revealed some improvement in the Current Situation index.

Across the Atlantic, the US NFIB Small Business Optimism made a further recovery in April, from 101.8 to 103.5 (and above the forecast 102.0). The report was indicative of an economy making some further gains into the June quarter after the lows of earlier this year affected by late last year’s stock market rout and the Government shutdown.

On the Brexit front, the Telegraph reported that Cabinet Ministers have been urging the PM to abandon Labour Party talks though apparently she is pressing on with cross-party talks and on what compromises the Government is prepared to consider in order to secure an agreement to leave the EU. It was also agreed that it is imperative to bring forward the Withdrawal Agreement Bill in time for it to receive Royal Assent by the time of the summer Parliamentary recess, though how this might happen remains unclear. Sterling has lost some ground against the USD but held its ground against the Euro, the pairs trading at 1.2906 and 0.8678 respectively.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.