Price growth edges lower despite reasonable economy

Insight

There’s a strong expectation that the US fiscal stimulus deal will be resolved in the next few hours.

https://soundcloud.com/user-291029717/us-deal-imminent-uk-marooned-brexit-all-at-sea?in=user-291029717/sets/the-morning-call

I feel so close to you right now, it’s a force field – Calvin Harris

Markets were on a wait and see mode during our Friday night as the current two key uncertainties, EU-UK trade deal and US Fiscal Stimulus remained unresolved. European and US equity markets ended Friday marginally in the red, core bond yields were little changed, and the USD was a tad stronger, reflecting the cautiousness in the air. Weekend developments have been mixed, one big positive has been news that US politician have found a compromise on the Fed lending programme, clearing the way for a vote on the pandemic relief package as soon as today. Meanwhile EU-UK Trade negotiations remain stuck on fishing rights and we have had some unwelcome virus news from London to LA and Sydney!

The final big obstacle for a bipartisan approval of a US pandemic relief package was overcome by US Congressional negotiators late Saturday, US time. The big last sticking point was the future of the Fed lending facility, as part of the compromise, going forward the Fed will need Congressional approval to reactivate its emergency lending facilities from earlier in the year, although it will be able to set up similar facilities. The Fed’s current bond buying programme, in US Treasury and mortgage bonds, is unaffected, but the Fed would need approval to reactivate its corporate bond buying programme, which was instrumental in calming markets during the crisis. Under the deal, the remaining $429 bn in the disputed emergency facilities would be used to offset the new relief bill.

The fiscal package is expected to be around $900b (~4.5%/GDP) and reportedly the deal reportedly includes a round of $600 cheques for households, $300 extra per week in unemployment benefits, and extra funding for education and small businesses. Speaking not long ago, Senate Majority Leader Mitch McConnell said “I believe I can speak for all sides when I say that I hope and expect to have a final agreement nailed down in a matter of hours.”. Final votes in the House and Senate could occur over the course of our day.

Meanwhile, Brexit negotiations remain in a stalemate as negotiators are still dealing with the financially immaterial but politically-charged issue of EU fishing rights in UK waters. A deal was supposed to be agreed by the end of the weekend to allow the European parliament time to review and sign it off, although French and UK politicians have suggested talks could yet stretch into this week. A deal can still be provisionally applied on 1st January even if the EU parliament doesn’t get to hold a vote in time. So there is still time for politician to wrangle some more.

That said, the virus dynamics may actually instigate a greater deal of urgency for a deal to be done. Arguably, the UK now has a bigger fish to fry (excuse the pun) with last week’s news of a new virus strain prompting PM Johnson to announced a new Tier 4 level of restrictions for London and some surrounding areas. The Tier 4 restrictions, which amount to a full lockdown, will initially be reviewed on December 30 but could remain in place for months. All non-essential shops will be closed, people ordered to stay at home unless absolutely necessary and households banned from mixing. Several European countries have announced a travel ban on the UK, in response to the fast-transmitting new variant of Covid-19.

Unfortunately, the worrying virus news have not been limited to the UK. In Italy, the government announced a full nationwide lockdown to cover most of the Christmas and New Years period. Virus stats in the US also remain out of control with California recording the worst figures per capita. According to Bloomberg, San Bernardino, Riverside and Los Angeles now rank one, two and three among big US counties with the highest rates of virus cases per capita in the past week. New cases, deaths and hospitalizations all hit records in Los Angeles this week – including 5,424 reported in hospitals Saturday.

Bad virus news unfortunately also include Australia with the Northern Beaches cluster resulting in Sydney now being isolated from the rest of the country. On Sunday all of the country’s states and territories imposed travel restrictions on its residents as a coronavirus cluster in the city grew to around 70. The Sydney cluster highlights the challenges with the proposed Trans-Tasman bubble, which NZ PM Ardern had earmarked for Q1 next year.

On a more positive virus news, Moderna vaccine will begin distribution across the US starting Sunday, after a Centers for Disease Control and Prevention panel recommended its use for people 18 and older

For now the market narrative has been that vaccine and stimulus will get us over the line with the near term virus infections and lockdowns only a temporary setback. That may be the case but it is certainly looking more challenging by the day and the economic impact from new lockdowns may prove to be bigger than what investors are currently pricing.

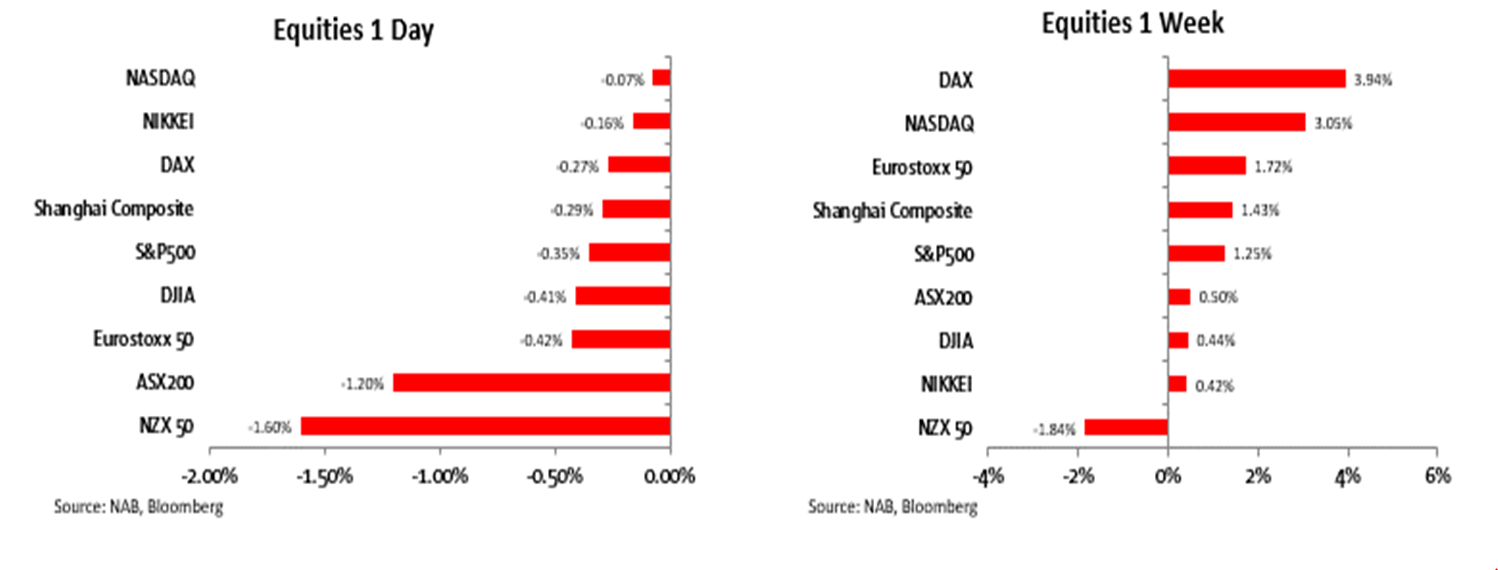

Looking at equity markets a cautious wait and see mode was pretty evident on Friday with the S&P500 and NASDAQ falling 0.4% and 0.1% respectively. Tesla joins the S&P500 today, as the 7th largest company in the index, with index rebalancing by fund managers on Friday resulting in huge trading volumes. Passive funds, estimated to be in the region of $70bn are likely to do their rebalancing on Monday, so some market volatility should be expected as the car/battery/rocket maker ‘s comes at the expense of several other big names.

Although Friday was a down day for equities for the week most equity markets managed to record positive returns with the DAX leading the gains up 3.5% and the NASDAQ not far behind, up ~0.3%. NZ NZX 50 was the underperformer , down -0.50%.

After hours US equity futures jumped higher aided by gains in US bank stocks after the Fed said banks could resume share buybacks, with a number of big banks saying they intended to do so next year. News of an imminent US fiscal stimulus favour a positive opening later today.

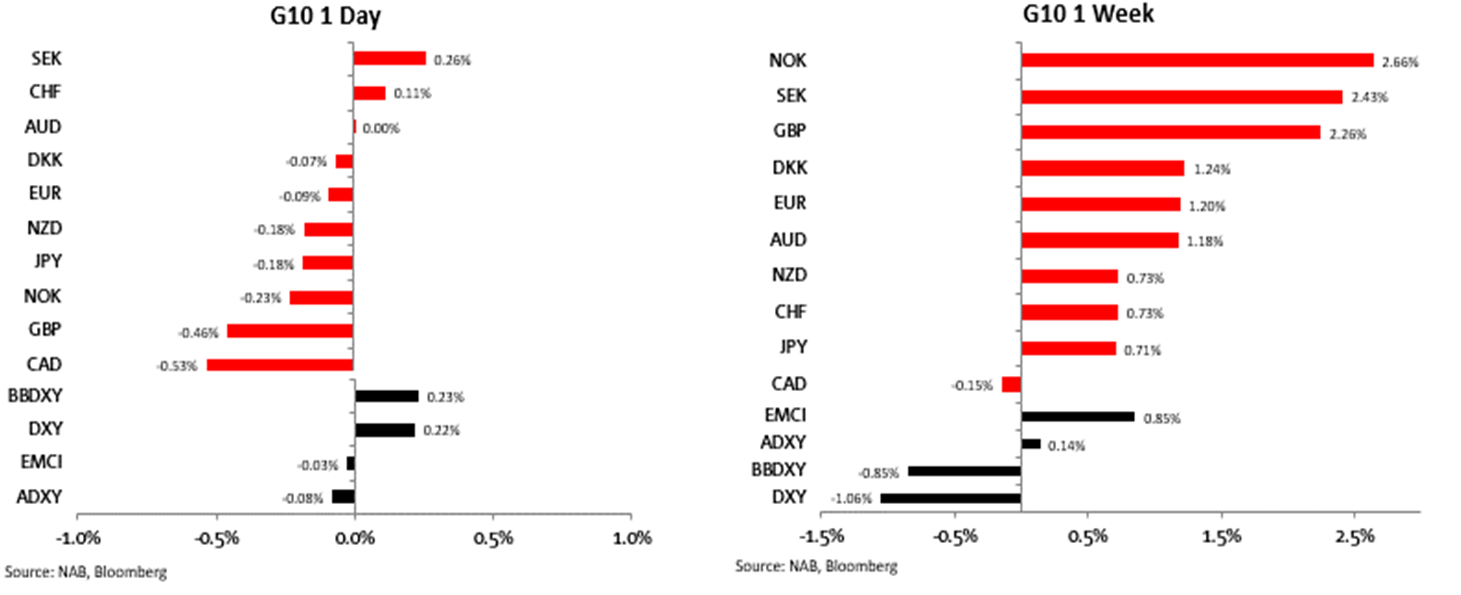

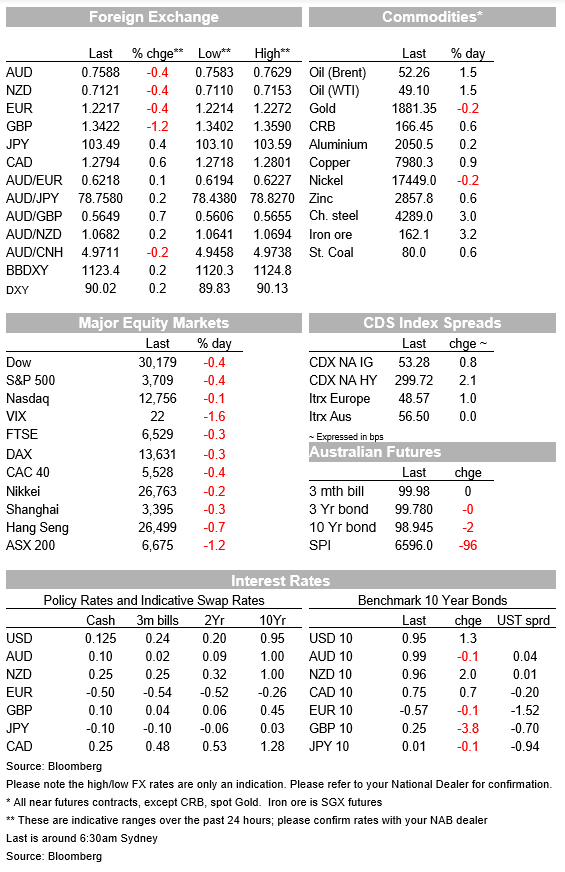

Moving onto FX, Friday’s uncertainties gave the beleaguered USD a breather with both BBDXY ( +0.23% and DXY( +0.22%) indices managing to scrape small gains for the day. This was a small consolation as the greenback was broadly weaker on the week, down between 0.85% and 1.06% in index terms. NOK was again the big winner, up over 2.66% aided by solid gains in oil prices and a Norges Bank sounding optimistic during the week. GBP was the other big winner, up over 2% as hopes of a EU-UK trade deal intensified. The AUD and Euro recorded gains over 1% and the NZD was up 0.73%. CAD was the only G10 losing ground against the USD.

That said, we have seen some decent FX moves at the open. GBP has gapped lower and now trades at 1.3432, lack of development on the Brexit front plus worrying virus news not helping cable. The Euro has fallen by around 30 pips to 1.2226, the AUD has also lost about 30 pips and now trades at 0.7588 while NZD has fallen by a similar amount to 0.7121. Interestingly USD/JPY has risen 15pips to 103.479, may be harbinger to a likely improvement in risk appetite as an when US equity futures open?

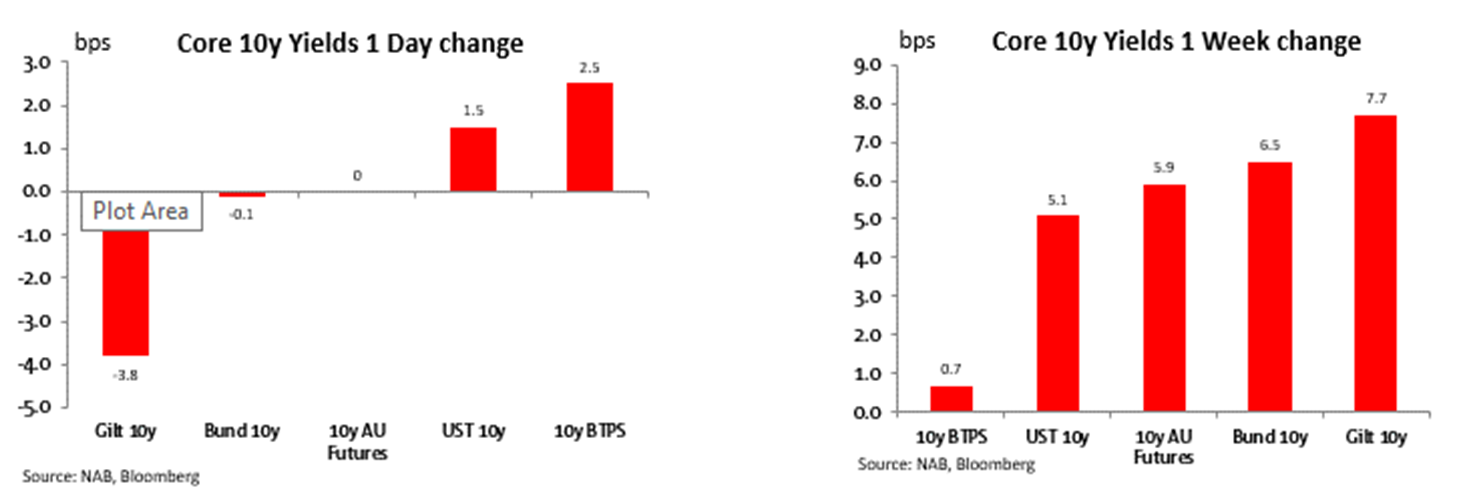

The US 10-year Treasury yield ticked up to 0.95% on Friday, near its recent highs. The recent rise in US rates has been driven almost exclusively by higher inflation expectations, with the US 10-year ‘breakeven inflation’ rate reaching a fresh 18-month high, at 1.96%, on Friday. This means US real interest rates have actually been falling over the past month, one factor contributing to the ongoing decline in the USD and continued ascent of equity markets. The US 10-year real rate is below -1% again.

Steeper curves was the theme for the week with longer dated yields moving up in the past five trading days.

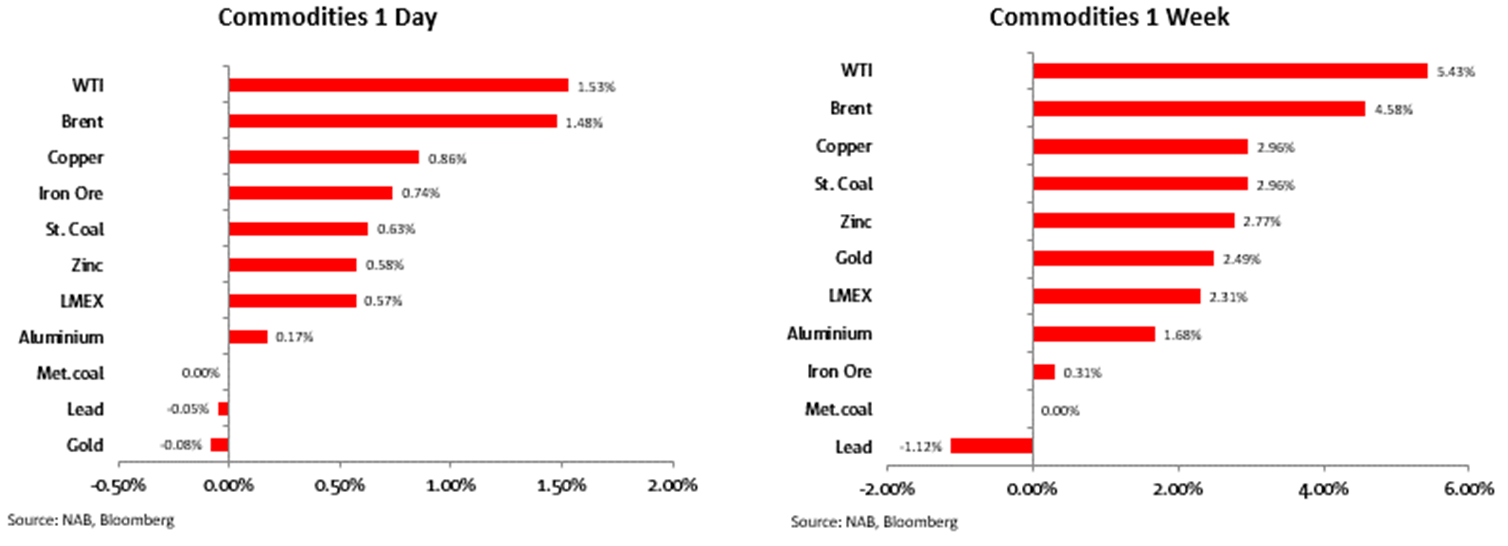

Commodity prices continue to push higher, consistent with the market pricing a more positive demand outlook. Brent crude oil reached $52/barrel on Friday, its highest level since March, while copper touched $8,000/tonne, the first time since 2013. Apart from oil, copper and aluminium had a good week while iron ore retained its previous week’s gains.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.