Price growth edges lower despite reasonable economy

Insight

Earnings results have pushed US equities to record highs.

https://soundcloud.com/user-291029717/us-equities-ride-high-pound-dives-on-uncertainty

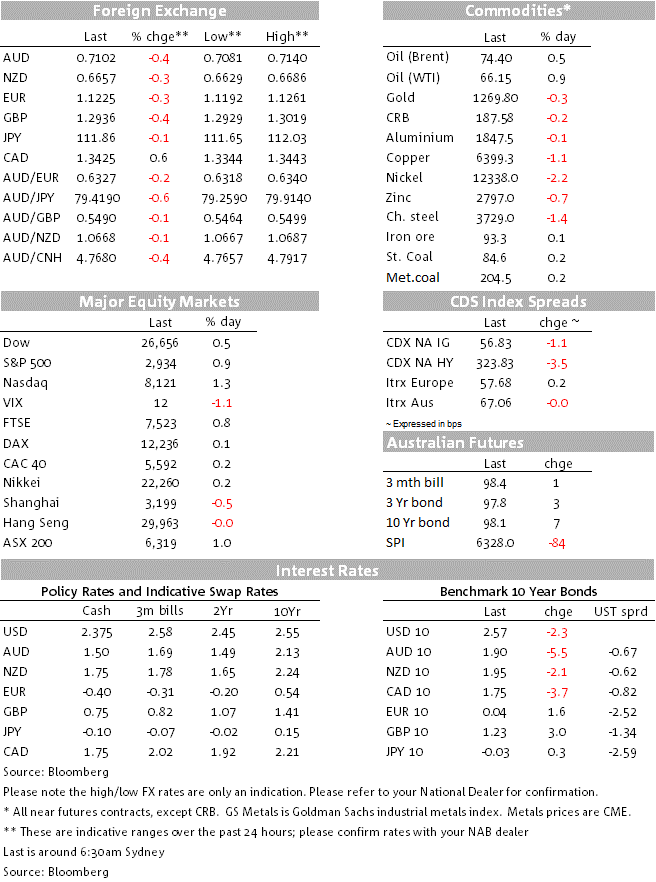

The S&P 500 has just closed at a new record high, with all but one sub-sector – the ultra-defensive Consumer Staples – in the green. Singled out for praise are Health Care stocks (+1.60%) recovering after their recent beating on concerns about the potential broadening of Medicare, and IT, the latter including a 15% jump in Twitter after reporting a higher than forecast daily user count of 134 million and revenue of $787m in the quarter, 16% up on a year ago. I’m looking at Twitter founder Jack Dorsey on TV at the moment. My son sports the same beanie; unfortunately that’s where the similarity ends. Back to the day job.

Yesterday energy was the big outperformer on the surge in oil prices following the news that the U.S. planned to cancel all waivers granted to countries reliant on Iranian oil imports from May 2. Today the energy sector is close to flat, apparently on stronger belief that other OPEC+ members will step up production to fill any void left by reduced Iranian exports, though this is not reflected in oil prices where Brent crude added 46 cents to Monday’s gains, now at $74.50 and WTI crude another 77 cents to $66.32. China for one is up in arms about the proposed cancellation of its waiver (like most others, it never supported the US pulling out of the Iran nuclear treaty) though it remains to be seen if this throws a spanner in the works regarding further progress in Sino-US trade talks.

US bond yields have given back Monday’s gains, 10sd -2.5bps to 2.565%, this despite a 1bp rise in break-even inflation rates, the latter presumably off the back off higher oil but which didn’t show up much on Monday when most of the oil price surge occurred.

Notwithstanding the strength in oil prices so far this week, the US dollar is stronger against all G10 currencies bar the JPY where USD/JPY is close to flat into the NY close. The BoJ meets tomorrow. The narrow DXY index has posted its highest intra-day level since 20th June 2017 at 97.777 (versus prior highs of 97.71 on both 7th March this year and 14th December 2018). DXY has since slipped back and is ending NY just shy of its March 7th close. Broader indices haven’t quite made new local highs but are perilously close (our own live version of the Fed’s ‘majors’ index – the latter published only with a one week lag – is currently less than 0.1% away from surpassing its March 7th high.

Latest USD gains preceded what was a mixed bag of very much second tier US data. The Richmond Fed April Manufacturing Index printed at 3 from 10 last time and an expected 10, the FHFA version of house prices rose 0.3% in February against 0.5% expected while March New Home Sales jumped by 4.5% in contrast to weaker Existing Home Sales earlier this week but for what is a highly volatile series.

AUD was languishing during our time zone yesterday and has lost further ground overnight (low of 0.7081) in front of this morning’s CPI report. It is only sitting mid-pack amongst G10 peers though, with NOK and CAD both giving back a good chunk of yesterday’s oil price inspired gains to sit at the bottom of the league. GBP, EUR and NZD are all lower but not quite as much as AUD.

Not helping GBP is the FT reports of little confidence in Downing Street that the negotiations between the Conservatives and Labour will yield a breakthrough and that some of PM May’s aides believe the talks could collapse this week. We also have hard-Brexit supporting Tory MPs conjuring up new ways of challenging Mrs May for the party leadership before the current 12-month moratorium expires in December. In the circumstances, GBP isn’t faring too badly.

Eyes down for AU Q1 CPI at 11:30 AEDT.

NAB forecasts weak headline inflation of 0.2% q/q, 1.5% y/y (consensus 0.1% but also 1.5% y/y), as a large fall in fuel prices (forecast at -8% q/q) weighs on price growth. Partly offsetting the impact of fuel has been higher fruit and vegetable prices, the result of floods in Queensland. NAB also expects core inflation softened in Q!, with another 0.4% print for the trimmed mean measure, bringing annual core inflation down to 1.7% from 1.8% (market consensus also 0.4%/1.7%)

Today’s outcome will be assessed in the context of commentary in the latest (April) RBA Minutes which notes that “Members also discussed the scenario where inflation did not move any higher (my emphasis) and unemployment trended up, noting that a decrease in the cash rate would likely be appropriate in these circumstances”. On the RBA’s preferred trimmed mean measure, CPI needs to print at 0.5% just to be standing still. So 0.4% or less means it has moved away from the 2-3% target.

Even if this proves to be so, it remains probable that the RBA will still await evidence that its second condition for a lower rates – unemployment trending up – is being met before any decision is taken to cut rates – NAB expects not before July (and so with the benefit of both April and May labour market data).

This evening and after last week’s further German PMI disappointments, there’ll be keen interest in the latest IFO survey (18:00 AEDT) where the overall business climate index is expected to lift slightly, to 99.9 from 99.6.

Also up is the Bank of Canada’s latest rate decision, confidently expected to be unchanged but where markets, already flirting with the notion of a rate cut before year-end, will be keen to see if the Bank retains its public tightening bias, albeit it doesn’t pretend rates are going up anytime soon.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.