Price growth edges lower despite reasonable economy

Insight

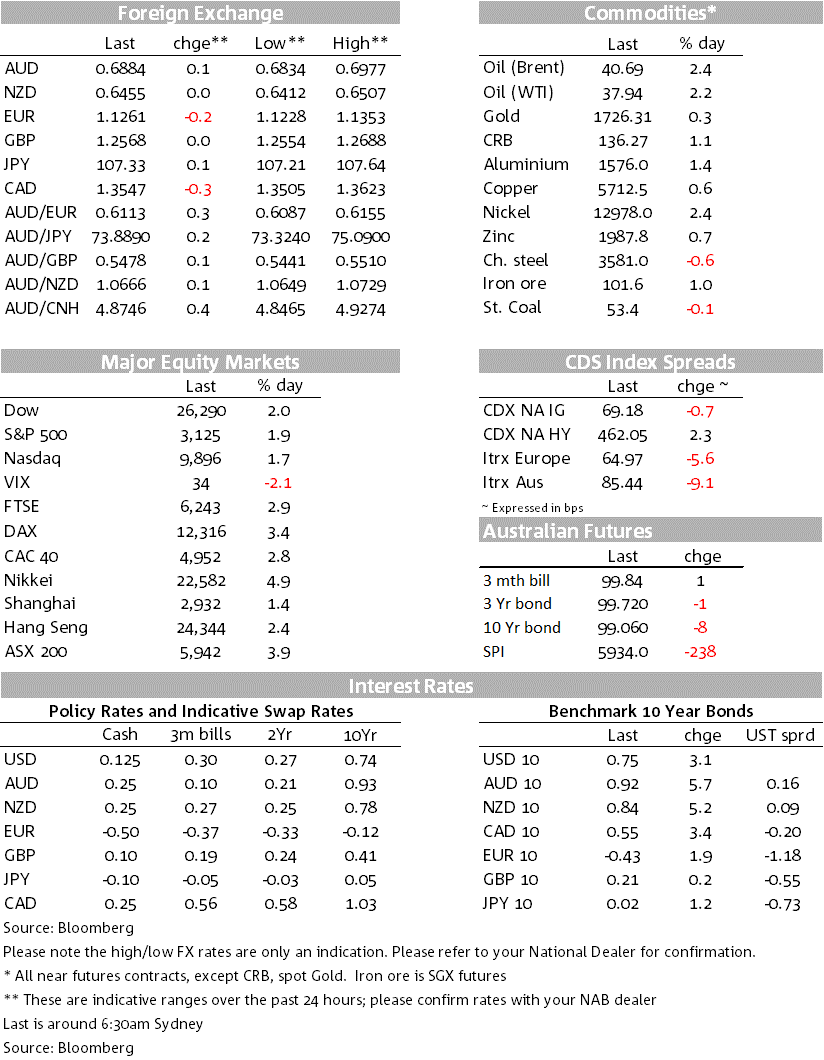

Market sentiment is higher again this morning from a surprise rebound in US retail sales, coupled with talk of a $1 trillion infrastructure program from the Trump administration.

“We just want to dance here, someone stole the stage; They call us irresponsible, write us off the page; Marconi plays the mamba, listen to the radio, don’t you remember; We built this city, we built this city on rock an’ roll” Starship 1985

The US consumer is back according to May retail sales with core control sales +11% m/m and more than double the market consensus of 5.2% and almost fully reversing last month’s ‑12.4% decline. Such a rapid turnaround has encouraged those hoping for a V-shape recovery (or at least reducing the risks of a U/L shape).

An effective treatment for severe cases of COVID-19 also bolstered sentiment (Dexamethsone, widely available, cuts mortality for those on a ventilator by one-third according to a UK study). The S&P500 is up 1.9% and is now up more than 5% above its intraday low on Monday before the Fed announced that it would start its corporate bond buying. Late headlines yesterday of the Trump Administration considering another attempt at a $1 trillion infrastructure package also saw yield curves steepen with the US 30yr yield +7bps to 1.53%; US 10yr +3.1bps to 0.75%. Powell’s remarks overnight were not market moving.

Concerns remain in the background around the spread of the coronavirus in the US (Texas coronavirus hospitalisations are now up more than 66% since Memorial Day), while in China some Beijing districts have shut schools in order to contain the latest outbreak.

FX moves were modest with the USD (DXY) up 0.2% in reaction to the strong retail numbers and some concern around the virus. EUR is down 0.2%, while USD/Yen is broadly unchanged. The AUD was also little changed on net, but did reverse yesterday’s intra-day gains, falling 1.4% from its high of 0.6977 to be at 0.6880.

Headline retail sales rose +17.7% m/m with the core control measure that feeds into consumption +11% against 5.2% expected and -12.4% previously. Both sets of growth the strongest in the history of the data that dates back to 1992. The bounce in retail sales is remarkable and confirms the narrative seen in high-frequency data of activity having troughed in mid-April and recovering ever since. Two big implications from the number are that; (1) Q2 GDP may not be as weak as first thought given the strong bounce in May and a likely repeat in June; and (2) for advanced economies consumption might recover faster than the industrial side due to government payments offsetting lost income (a big contrast to the experience seen in China). Some notion of that thesis was reflected in industrial production which rose 1.4% m/m against 3.0% expected.

The US Administration has again floated the prospects of a $1 trillion (5% of GDP) infrastructure plan that may be released in July. According to sources the Department of Transport has reserved around 75% of the proposed funds for projects such as roads and bridges, but is also setting aside 25% for 5G infrastructure (see Reuters for details). The announcement late yesterday saw longer-end bonds sell-off with the 30y yield rising 7bps to 1.53%. While mooted previously, higher infrastructure spending is also a policy of the Democrats and in an election year could gain traction.

Was the finding of an effective treatment for severe cases of COVID-19, and potentially a game changer for mortality rates. A UK study finds dexamethasone, a widely available steroid, is effective in reducing mortality for patients on ventilators by one-third and for those receiving oxygen only by one fifth. Note there is no benefit for milder cases which do not require respiratory support (see link to the study). The results of the large scale study have been viewed positively by the medical community.

Data elsewhere was on the positive side with the German ZEW expectation rising to 63.4 from 51.0. Headline UK unemployment was also lower than expected at 3.9% against the 4.7% consensus, though the claimant count rose the 7.8%.

Causing some intra-day volatility has been a pick-up in the spread of the virus in parts of the US and in China. Texas hospitalisation associated with COVID-19 is now up more than 66% since the Memorial Day holiday and at least 10 other states are showing a rise in hospitalisations according to CNBC. Nevertheless, Texas’ Governor Abbott downplayed the rise, saying hospitalisation is still a small percentage of the state’s total available hospital beds and Texas will continue to re-open its economy. A WSJ article also implied there is a high bar for any re-imposition of lockdowns. In China, some Beijing districts have closed schools in order to contain the latest outbreak. Also concerning, but not market moving, was the report of 20 deaths in border clashes between India and China, while North Korea blew up a liaison office near the border.

Though he maintained his dovish tone. While acknowledging that “some indicators have pointed to a stabilisation and in some areas a modest rebound in economic activity” he cautioned that the economy was still well away from where it was pre-COVID and there was significant uncertainty about the shape of the recovery. Powell said the Fed was at an “early stage” in thinking about the possibility of applying Yield Curve Control in the US (whereby the central bank targets a longer-term interest rate, such as the RBA and BoJ have in operation). On its corporate bond buying, Powell said the Fed would adjust its purchases to market conditions, so purchases would be increased in stressed markets and reduced when credit markets are stronger.

More signs are emerging of the economy recovering faster than expected. Weekly Payrolls data yesterday showed payrolls have recovered about 1.5% from the April low in unadjusted terms. The largest gains in unadjusted payrolls from the national low in April have been in hospitality (11%), retail trade (4%) and education (4%). Hospitality jobs are now about 30% below their pre-virus peak, while retail trade is 9% below and education is 5% lower. The data will likely bolster the more optimistic tone coming from the RBA and Treasury recently, the RBA Minutes yesterday repeating the line that the recession could be “shallower than earlier expected”.

It’s very quiet both domestically and offshore. There is nothing scheduled for Australia. Internationally hard May data is starting to be published with the UK CPI and US Housing Starts/Permits.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.