Hear NAB’s senior expert panellists discuss a range of topics to provide key insights to help you and your business prepare for the current property market climate.

Australia joined the bull run in the share market yesterday, clocking up 20.7 percent growth since March 23.

https://soundcloud.com/user-291029717/v-shaped-optimism-drives-shares-higher?in=user-291029717/sets/the-morning-call

“Don’t stop believin’; Hold on to the feelin’; Streetlights, people; Don’t stop believin’; Hold on”, Journey 1981

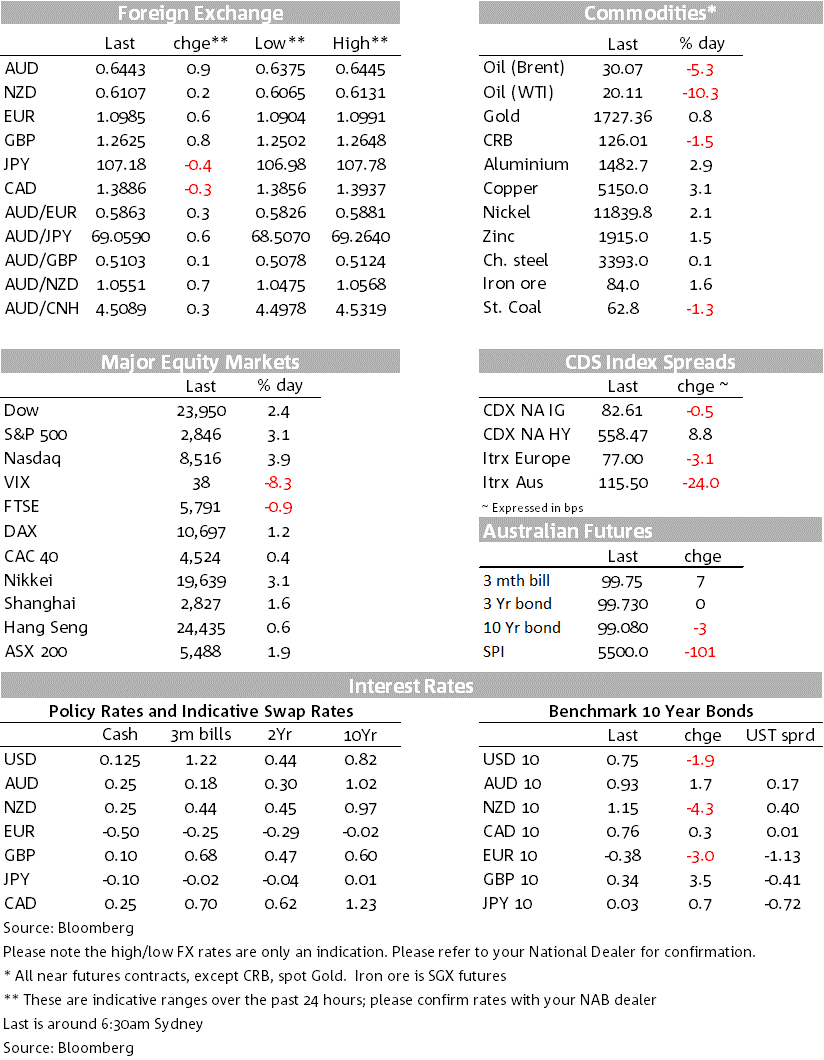

Equities surged overnight (S&P500 + 3.1%) as talk builds of more countries contemplating an easing of containment measures; gains coming even as bank earnings disappointed and as the IMF downgraded global growth forecasts to the weakest since the Great Depression. President Trump is planning an announcement in coming days, while 10-states that account for nearly 38% of the economy have also began working on their own separate resumption plans. Some European countries have already begun the process with Austria allowing the reopening of certain shops and Denmark allowing children under 13 years back in school from tonight. Closer to home, the Australian Cabinet is set to meet this week and will be discussing the path out of containment, though PM Morrison has emphasised an easing is “weeks away” and WA Premier McGowan has indicated May 1 as the earliest possible date.

The USD was on the backfoot with DXY -0.6%. Gains were led by the AUD (+0.9%) and GBP (+0.9%), with EUR (+0.6%) and Yen (USD/JPY -0.4%) also higher. AUD support driven by notions of China bouncing back strongly with yesterday’s trade data smashing expectations, following on from Friday’s credit figures. GBP gains probably linked to notions of Europe easing containment measures. Yields in contrast were little moved with US 10yr yields -1.9bps to 0.75%, though European peripheral yields moved sharply with Italian BTP yields +19.3bps. In credit the Fed’s commercial credit buying started today, bringing life to the market; investors are following the Fed with a Blackrock blog noting “we will follow the Fed and other DM central banks by purchasing what they’re purchasing, and assets that rhyme with those” (see link).

Equities surged overnight with the S&P500 +3.5% and since their late March low are up 27% and is just 15.9% away from its peak. The recovery in equities is being driven by three factors – (1) light at the end of the tunnel with more countries talking about easing containment measures; (2) Fed’s actions, particularly QE and its expansion to corporate credit with credit spreads contracting sharply and opening up the corporate bond market; (3) indications of China bouncing back sharply and adding support to notions of a V-shape recovery if countries can lift containment measures. The sharp rally in equities came despite disappointing earnings from JP Morgan and Wells Fargo with loan provisions being raised to their highest level since 2010 and likely to be raised further – JP Morgan’s provisioning was partly based on the assumption that GDP would fall -25% and unemployment would rise more than 10% in Q2, but their economists have recently amended their forecast to a 40% decline in GDP in the quarter and a 20% unemployment rate. No surprises then to see both JP Morgan (-2.7%) and Wells (-4.0%) down for the day and financials underperforming (S&P500 financials sub-index +0.3%). More earnings downgrades are likely in coming days and the latest ISM COVID-19 survey finds that almost one-half (47%) of respondents’ report reduced revenue targets of 22 percent on average (see ISM COVID-19 survey for details).

IMF forecast downgrades took a backseat to the possible easing of containment measures in the near future. For the record, the IMF now expects a global recession with a 3% contraction in 2020 and far exceeding the 0.1% contraction of 2009. The IMF though is projecting a v-shape recovery and is projecting growth to bounce back by 5.8% in 2021 aided by policy support. Amongst the larger economies, Europe is set to suffer more than the US (Euro area to shrink 7.5% in 2020 compared to 5.9% in the US), while China is expected to continue its v-shape recovery with positive growth pencilled in for 2020 at 1.2% and than bounce by 9.2% in 2021. For Australia, GDP is expected to contract 6.7% before rising 6.1% in 2021 – helped along by China’s aggressive recovery (see IMF forecasts for details). While the IMF growth forecasts are pessimistic, it is nothing new and markets are firmly focused on when we could start to see some lifting of containment measures.

COVID-19 curve flattening continues, adding hopes that some easing of containment measures is likely. President Trump is expected to make some “important announcements” on guidelines for states to reopen the economy – likely “rolling reopenings”, while ten US states that account for nearly 38% of the economy have begun working on plans to reopen for business. In Europe, Austria allowed the reopening of certain shops overnight, including DIY stores, garden centres and those shops smaller than 400sqm. Denmark will allow children aged 13 years and younger back to school tonight, while Poland has said it will unveil its re-opening strategy on April 19. In France, President Macron said the lockdown would stay in place for another month, to May 11th, but said restrictions would be gradually eased after that. Closer to home there is open debate in the NZ press about the need for containment measures and the NZ PM is giving an update on Thursday with their Cabinet meeting on April 20. Australia’s Cabinet is also meeting this week to discuss the possible path of lifting restrictions, though PM Morrison has emphasised it is still weeks away and WA Premier McGowan has indicated May 1 as a possible date for some easing in restrictions.

China’s trade figures yesterday played into the view of China bouncing back following the lifting of containment measures and provides support for the alternative high-frequency data that have been pointing to a recovery since early March. Imports were -0.9% y/y, well above the consensus estimate of -9.8%. Exports also beat at -6.6% y/y against -13.9% expected. Overall YTD figures suggests imports are now tracking closer to 2019 levels, while exports remain well below last years’ levels. The overall trade balance was broadly in line at $US19.9bn. Detailed trade data highlight the resiliency shown in imports. Commodity imports most linked to Australia were close to or beyond 2019 levels in YTD terms (iron ore +1.3% y/y and natural gas +1.8% y/y ).

Its no surprise than to the see the AUD 0.9% higher even after an unprecedently week NAB Business Survey (conditions -21 and confidence -66) and weakness in oil (see below). The AUD remains a clear China proxy and given its exposure to Chinese growth (more than 30% of exports go to China), Australia should benefit from China’s resumption of economic activity and from its stimulus measures which will target the industrial and fixed asset side of the economy.

Oil fell overnight (WTI – 7.4%) with Bloomberg reporting Saudi Arabia would maintain production at a very high level this month, ahead of the agreed supply cuts scheduled to take place from May, and reports of Saudi Arabia heavily discounting crude when selling into Asia. The decline in oil saw commodity currencies except for the AUD underperform.

Credit markets continue to improve following recent Fed action. BBB- rated Marriott, a hotel operator, is seeking to raise $1b in bonds today, a positive sign that investors are willing to lend to companies in those industries most affected by the Covid crisis (albeit at high rates – pricing is in the 7.25% area). The Fed’s recent announcement that it would buy so-called ‘fallen angels’ (i.e. those companies downgraded to high yield by rating agencies) as part of its corporate bond programme has reinforced investor demand for those companies with ratings just above the high yield threshold. In Europe, Credit Agricole and BNP Paribas reopened the primary market for senior bank bonds, issuing a combined €2.75b, the first deals in this space for around two months. The bonds priced between 30bps to 40bps lower than initial pricing guidance, a sign of strong investor demand.

A quiet day domestically with only consumer confidence measures on the radar. Focus than turns to the Americas with the US Retail Sales and Industrial Production, and than to the Bank of Canada meeting to see whether they follow the US Fed in extending asset purchases.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Hear NAB’s senior expert panellists discuss a range of topics to provide key insights to help you and your business prepare for the current property market climate.

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.