Hear NAB’s senior expert panellists discuss a range of topics to provide key insights to help you and your business prepare for the current property market climate.

Rising infection rates in US southern states hit equities hard on Friday.

https://soundcloud.com/user-291029717/virus-numbers-cause-concern-jobs-and-hong-kong-focus-for-the-week-ahead?in=user-291029717/sets/the-morning-call

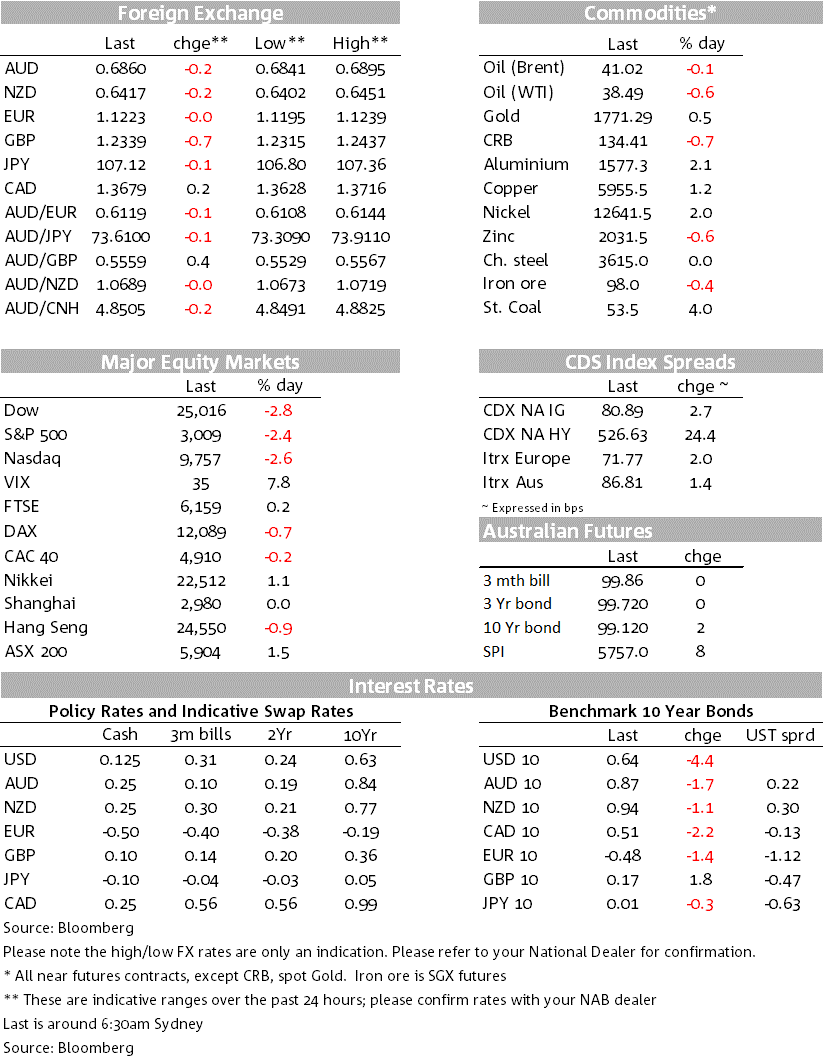

Texas and Florida reimposed some restrictions following the surge in new virus cases and high frequency data is also showing some deceleration in the speed of recovery (chart below). Equities fell sharply in response (S&P500 -2.4%) led by banking stocks, global yields fell as the curve bull flattened and the USD was little changed on net (DXY +0.1%), ditto the AUD (-0.2%).

“He’s tried to make me go to rehab; I won’t go, go, go; The man said, ‘Why do you think you here?’; I said, ‘I got no idea’” Amy Winehouse, 2006

Rehab was Amy Winehouse’s only US top ten hit (peaking at number nine on the Billboard Hot 100). Importantly though the song went on to win three Grammy awards including Song of the Year and is also an apt description of what drove markets on Friday with Texas and Florida reluctantly reimposing some virus restrictions amid a surge in new virus cases and hospitalisations. New daily virus cases have reached new, or close to record highs in all states and is at a record at the national level at 44,373 cases. Importantly hospitalisation rates are also soaring with Texas seeing a 57% increase in hospitalisations compared to the prior week and in Arizona the governor states his hospitals are “likely to hit surge capacity very soon”.

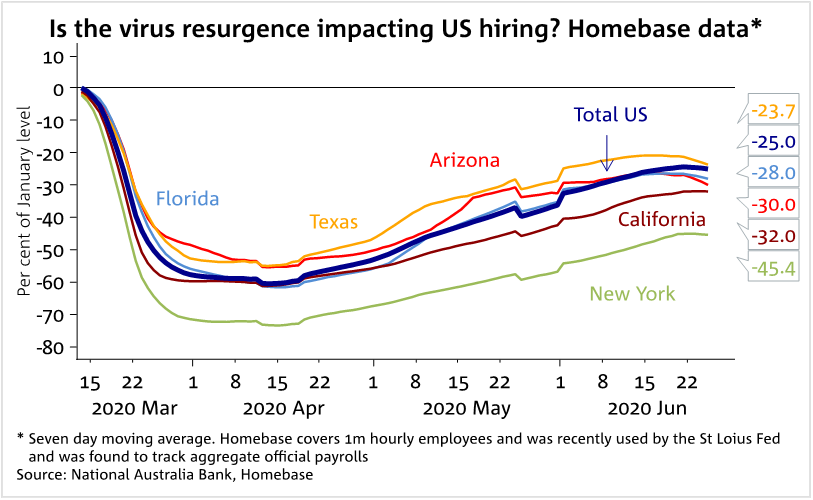

Texas has re-imposed some restrictions including closing bars, imposing 50% capacity limits to restaurants and postponing elective surgery in a number of counties. Florida is also banning the serving of alcohol and closing beaches in Miami for five days around Independence Day. Importantly the re-imposition or halting of re-opening plans is expanding beyond Texas and Florida with Washington State and San Francisco saying they are pausing the next phase of re-opening amid the rise in infections. The mean incubation period of the virus of 5-14 days also means it will be some time before we see the impact of tighter restrictions and could see a negative tone for markets this week. The re-imposition of restrictions also has the potential to slow the sharp rebound seen in the high frequency data to date. Late last week we saw some evidence of that with restaurant bookings across the Open Table platform dipping in Dallas, Houston and Phoenix. That dip in activity looks like it may spill over to the labour market with Homebase data showing a dip in the number of hourly employees in Arizona, Florida and Texas (Chart above).

Equities fell sharply in response with the S&P500 closing down -2.4% with losses lead by banking stocks and communication services. Banking stocks fell -3.7% in reaction to late Thursday’s stress test results and the Fed restricting buybacks (and dividends – capped at current levels) before Q3 at the earliest. Note the big US banks were down -7%, though the fall on Friday merely reverses the 6% rally seen on Thursday. Detailed pandemic scenarios showed under a severe scenario capital levels at several banks fall close to regulatory minimums. ‘Communication services’ stocks fell 3.1% led by losses in Facebook (-8%) and Twitter (-7%) with a number of companies announcing a pause on advertising on social media platforms amid a “polarised election period”. Those announcing a pause included Unilever, Coca-Cola, Levi’s and Hershey’s with Unilever’s pause said to last until at least the end of the year. As noted above, with the mean incubation period of the virus of 5-14 days means a negative tone to markets could persist for the week.

US 10-year yields fell 4.4bps to 0.64%, its lowest level since mid-May, while the 30-year yield fell 6bps to 1.37%. How far bonds could rally should risk sentiment continue to deteriorate is perhaps given by the low end of the recent range in the US 10yr yields being 0.55%. Without a commitment to yield curve control, or willingness to take rates into negative (both being pushed back by the Fed and we will hear from Fed Chair Powell on Wednesday), a rally beyond this may be more difficult

The USD (DXY) rose just +0.1%, though is close to its four week high, while USD/Yen fell just -0.1% to 107.12. Interestingly the most risk-sensitive currency pairs were also little moved with the AUD -0.2% along with the NZD. It is not clear why the AUD and NZD have been insulated from the deterioration in risk sentiment.

The US PCE numbers while mixed, still showed a story of activity bouncing back in May and incomes being supported by government payments. Overall personal spending rose by a record +8.2% m/m after last month’s -12.6%, while personal income did not fully reverse last month’s gains with income -4.2% m/m from last month’s +10.8%. The moderate income decline means the savings rate is still at a very high 23%. Core PCE inflation was a tenth higher than expected at 1% y/y, but is showing little in the way of inflationary pressure. The two important implications from the data continue to be: (1) the fall in Q2 GDP is likely not as severe as previously though with the Atlanta Fed’s GDP Now revised to -39.5% annualised; (2) the data shows there is strong pent-up demand with a strong distinction to the GFC experience being household income and spending have not fallen in line with each other due to government stimulus. That puts the emphasis back on a mooted stimulus package by the end of July.

The WSJ reported China has warned the US that pressure over the HK Security Law and other matters could jeopardize the phase-one trade deal. Note China’s Standing Committee of the National People’s Congress is meeting this week (June 28-30) where they could vote on the proposed security law. Also in the news is China’s Global Times accusing Australia of “waging an intensifying espionage offensive against China” (see link). While sensational, the article illustrates the continued deterioration in the Australia-China political relationship.

This week in Australia we get ABS Payrolls on Tuesday which may show a further recovery in the number of jobs given the pick-up seen in high-frequency indicators to date. Also on Tuesday is a speech by RBA Deputy Governor Debelle who is speaking on “the Reserve Bank’s policy actions and balance sheet”. There is also a smattering other data pieces that while is unlikely to be market moving in this environment will be important for the outlook, including Building Approvals on Wednesday, Trade Balance on Thursday and Credit States on Friday.

International focus will remain on the path of the coronavirus, particularly in the US in a holiday shortened week (it’s Independence Day on Friday). Key data pieces for the week include the China PMIs on Tuesday, FOMC Minutes on Wednesday and any elaboration on yield curve control possibilities, US Payrolls and Manufacturing ISM on Thursday, while Fed Chair Powell and Treasury Secretary Mnuchin are testifying on Wednesday. Geopolitics could also re-emerge around the proposed HK Security Law with China’s Standing Committee of the National People’s Congress meeting from June 28-30.

It is very quiet with only the COVID-19 Household Survey domestically and the German Flash CPI of note. Full details below:

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Hear NAB’s senior expert panellists discuss a range of topics to provide key insights to help you and your business prepare for the current property market climate.

Price growth edges lower despite reasonable economy

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.