Labour market strong, housing supply falling behind

Insight

A blue day on the global markets.

https://soundcloud.com/user-291029717/blue-day-after-a-blood-moon

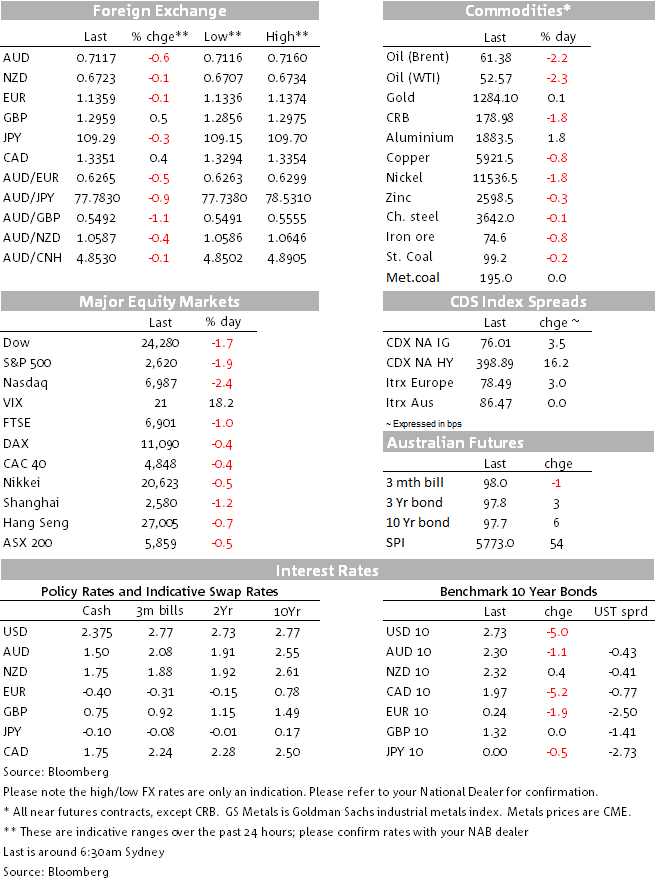

After observing MLK day on Monday, US equities have opened the week sharply lower reflecting a change in market sentiment amid a flurry of headlines suggesting US-China trade talks are not heading in the right direction, China’s president speech stressing the need to maintain political stability has been interpreted as a worrying sign over the country’s slowing economy while US data also printed on the softer side of expectations. UST yields are lower across the board and in spite of the risk off tone USD indices have edged a little bit lower weighted down by GBP’s outperformance (driven by data and Brexit news) while JPY benefited from a safe haven bid and its link to UST yields. AUD is the G10 underperformer not helped by the China news and a softer commodities backdrop with oil and copper leading the declines.

The recovering in risk assets has taken a breather this week, China’s data on Monday raised concerns over the degree of slowdown in the world’s second largest economy and yesterday’s speech by President Xi, at an unusual meeting of China’s top leaders, added further fuel to the notion that China may be slowing faster than what the official numbers suggest. In his speech President Xi stressed the need to maintain political stability adding that the Communist Party needed greater efforts “to prevent and resolve major risks”. The speech has been interpreted by many as a sign the party is becoming more concerned about the social implications of a slowing economy.

The US-China trade war remains front of mind as well with Trump tweeting yesterday for China to “stop playing around” and “do a real deal”. The WSJ reports that in a joint report to the US Trade Representative, the US Chamber of Commerce and the American Chamber of Commerce in China say Beijing’s ambitious plan to become a global technology leader is being widely implemented, casting doubt on efforts by Chinese officials to play down its significance.

News overnight that the US will pursue the extradition of Meng Wanzhou, China’s Huawei Technologies CFO, has been an additional factor adding to concerns over US-China trade tensions while early this morning the FT reported the US negotiators turned down an offer of preparatory trade discussions. Overnight market were already trading with a risk off tone, but the FT news accelerated the deterioration in risk sentiment.

So given the above mentioned backdrop, US equities have opened the week sharply lower with the S&P500 currently down 1.82%. IT, telcos and consumer discretionary sectors have led the decline. The NASDAQ is -2.35% and the Dow is -1.7% with Caterpillar and DowDuPont the big underperformers. After closing Friday with a 17 handle, the VIX has been on a steady upward trajectory overnight and currently sits at 20.62.

USD indices have edged a little bit lower (DXY now trading at 96.282) reflecting outperformance by GBP and JPY while commodity linked currencies have underperformed with AUD at the bottom of the pile.

The pound is up 0.56% to 1.2960 supported by a strong labour market report (see more below) and increasing optimism that a no-deal Brexit can be ruled out. there are continuing signs that the UK Parliament will be more in control of the Brexit process with a number of amendments proposed by various MPs, including staying in a customs union with the EU, a second referendum on Brexit, an Article 50 extension which would significantly delay any Brexit outcome, and ruling out of a no-deal outcome. The speaker will decide which amendments can go to a vote. The FT reports that the Cooper-Boles amendment to stop a no-deal Brexit looks to have a good chance of being selected next week and voted on in early February.

In addition to the China and trade news above, the decline in commodity prices led by falls over 2% in oil and copper have weighted on the AUD. The pair currently trades at 0.7116, 0.50% lower relative to yesterday’s level. Ahead of the CPI release this morning, NZD has had a pretty steady night, the pair currently trades at 0.6711, about 0.1% lower over the past 24 hours.

Our BNZ colleagues note that NZ’s Headline CPI inflation for the quarter should be very soft – close to flat – weighed down by much lower petrol prices and seasonal factors. But we expect core inflation to show signs of holding up. Indeed, the risk is that non-tradeables inflation overshoots the RBNZ’s estimate of 0.4% q/q. NZ inflation tends to be a good guide for Australia’s CPI, due for release next week.

UST yields have move lower across the board with the 10y note currently trading at 2.7338%, 5bps lower relative to Friday’s close.

Labour market strong, housing supply falling behind

Insight

Discover how to take advantage of opportunities in the US Private Placement (USPP) market.

Video

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.