Price growth edges lower despite reasonable economy

Insight

Markets adopted a mild risk-off mood overnight.

https://soundcloud.com/user-291029717/will-human-rights-bill-scupper-a-trade-deal?in=user-291029717/sets/the-morning-call

Slip slidin’ away, Slip slidin’ away. You know the nearer your destination the more you’re slip slidin’ away – Simon and Garfunkel

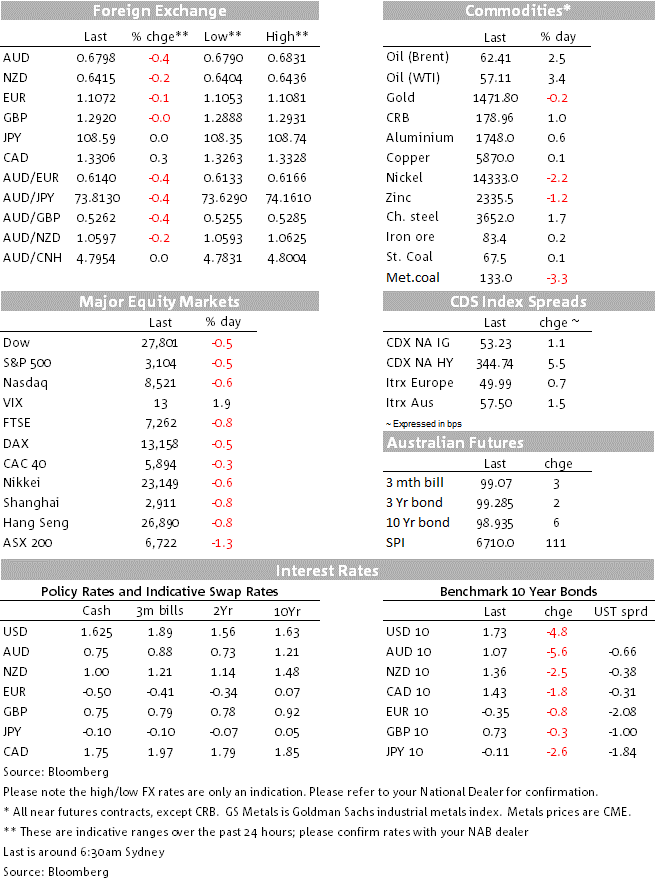

There is little doubt that China-US trade headline fatigue has started to set in in the past week or so, but market are nevertheless showing more sensitivity to news stories that cast doubts on the likelihood of a near term deal, in whatever form. Thus overnight we have seen the CNH, AUD, NZD and CAD all weaker, together with lower US equities and bond yields. First this was on new yesterday afternoon our time that the Senate have comfortably passed their version of bill that would require Congress to attest on an annual basis whether Hong Kong still qualifies for special administered status independent of Chinse influence. Then in last few hours, a Reuters report suggesting that a Phase 1 deal may not be completed this year has played with the grain.

‘May’ is a ’weasel’ word frequently used by analysts to give themselves an out when they get their calls wrong (as in ‘I only said it “may” happen”) but China’s strong response to the HK bill news is something to be taken seriously in terms of how it impacts on the trade discussions (just as the earlier introduction of alleged human rights volitation with respect to Muslim minorities in the Xinjiang province introduced a new dimension a month or so back). A “Trump aide’ has just been out saying progress is being made on Phase 1 deal text, and reports yesterday were that the two sides were going back to where they were in May when, recall, ‘90%” of a trade deal text was said to have been agreed.

All we’d say for now is that we have a good idea where markets will re-price if and when a Phase 1 deal get done and depending on whether it include some tariff roll-backs, but what happens between now and then is frankly anyone’s guess.

Minutes of the October FOMC Minutes just released show that most members thought that policy would be ‘well calibrated’ following their decision to cut rates by 25bps, though there is a comment that ‘some who voted for a cut said that it was a close call’. This tends to corroborate the market’s interpretation of the October 30th FOMC decision and surrounding Fed narrative of this being a ‘hawkish cut’. US interest rate markets and the USD are little changed out of the Minutes. Move on.

The main data point of note overnight was Canada’s CPI, which printed in line with expectations at an unchanged 1.9%. This is close to the mid-point of the Bank of Canada’s 1-3% CPI target range, so suggest that the bar to the BoC acting on its new found easing bias is still quite high, especially as – and as the BoC noted last week – wages growth are currently running above 4% a year.

Though CAD took a hit on Tuesday on some dovish BoC comment and news of labour strikes in the rail sector, latest weakness in CAD should be seen purely though the prism of the hit to all commodity/growth sensitive currencies on US-China trade deal doubts, down 0.4% in the last 24 hour, versus losses of 0.3% for NZD and 0.5% for AUD (so AUD sill just shading it as he most sensitive of this triumvirate to negative trade headline). Thus AUD/NZD has broken below 1.06 for the first time since late August.

GBP was little moved following yesterday’s Johnson-Corbyn TV debate, which a post-debate YouGov poll scored 51-49 to Johnson. A weaker AUD/GBP this morning is therefore purely a function of a lower AUD.

US equity indices are showing losses of ±0.5% with the energy sector the best performing, +1.1% thanks to a near $2 bounce back in WTI crude. This is on a reported 2.3mn barrel draw on crude stocks at Cushing, Oklahoma and also the weekly EIA inventory stats. showing a smaller 1.4mn barrel rise than the earlier reported, and less reliable, API stats showing a 6mn barrel inventory build.

US Treasury yields are currently about 5bps lower at 10 years and 3bp lower for 2s, after European benchmark yields earlier finished mostly less than 1bp down on the day.

Nothing of note during our time zone

Offshore, we get EZ consumer confidence, ECB minutes, Bundesbank financial stability and the OECD Europe outlook. The US has the Philly Fed survey and weekly jobless claims.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.