Price growth edges lower despite reasonable economy

Insight

It’s a significant day for Australian news, in a period where little else is driving markets in the rest of the world.

https://soundcloud.com/user-291029717/world-on-hold-except-in-australia

It’s been a quiet night of news, markets seeing some support for the USD re-emerge, US Treasury yields ticking back higher, but not sufficient to do any damage to stocks, the US main board indexes making some gains during the afternoon session, led by the tech stocks.

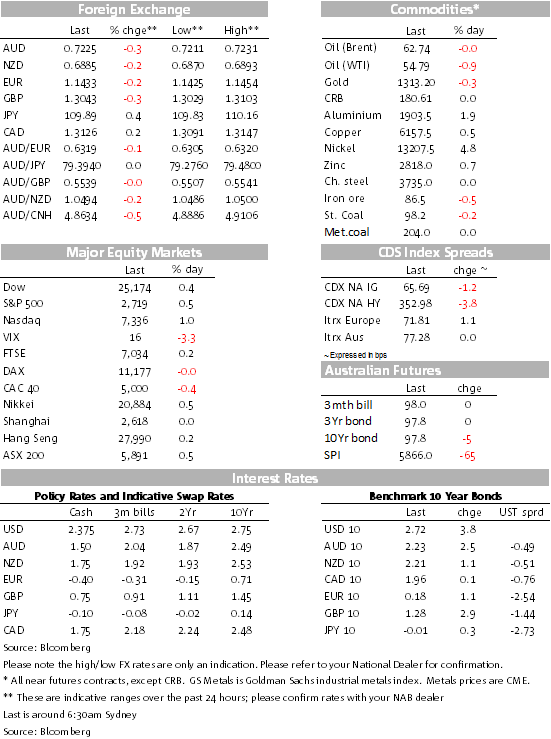

The AUD took a mini hit yesterday after the release another very weak Building Approvals report, the second in a row, this one for December, the data point revealing a 22.5% decline over the course of last year, confirming the coming decline in residential dwelling investment. After seeing a small rally into the number, the AUD lost 20 pips, ending the local session only a little above its session lows. It’s lost a little more ground overnight, but more from the move back toward the USD. It’s hard to see too much of a move higher – it’s likely to remain capped – ahead of today’s key event risk, first with Retail Sales at 11.30 (Trade too) that we expect will be on the soft side, followed by reference to an expected downward revision to growth and a less assured outlook to be outlined by the RBA at 2.30. (More on both of these below.)

The Financial Services Royal Commission was released yesterday after the local stock market has closed, receiving wide press coverage overnight, but no discernible currency impact.

RBA pricing has moved away from a mild tightening bias to an easing bias, the market yesterday factoring in just over a 50% chance that the Bank would ease by the end of this year. Understandably, that’s an about face from the expectation last year that there was an equivalent chance that the cash rate would rise.

German Chancellor Angela Merkel is urging creativity to unlock the UK-EU Irish backstop impasse. “There are definitely options for preserving the integrity of the single market even when Northern Ireland isn’t part of it because it is part of Britain while at the same time meeting the desire to have, if possible, no border controls,” Merkel said. “To solve this point you have to be creative and listen to each other, and such discussions can and must be conducted,” she said at a news conference with Japanese Prime Minister Shinzo Abe in Tokyo. Merkel said the backstop could be solved as part of a discussion over the separate “future relationship” agreement. Even so, EUR/GBP has been gaining a modicum of support overnight, though there’s not too much in it, the Euro gaining a net 0.12% since late APAC time yesterday.

As further background to Brexit, a FT story released overnight says that the UK government had promised Nissan circa £80mn in return for the car maker to invest and expand a new SUV model in Sunderland as well as Qashqai and X-Trail models. At the weekend Nissan said it would produce the new SUV in Japan. UK Business Secretary Greg Clark has said overnight that Nissan will need to reapply if it wants a U.K. financial grant, after it decided not to produce the X-Trail model at its Sunderland plant. PM May is travelling to Northern Ireland for a speech today (Tuesday).

Most high credit quality bond yields have ticked higher overnight in a mild risk-on session. The German 10y bund yield is up a net 1.1bos to 0.177% while the 10y Treasury yield is also ticking back higher to 2.72%, up 3.58bps with 2s also higher by 2.44bps to 2.5263%. Very small moves but hints of yields having overdone it on the downside after the FOMC and Powell press conference.

With China out this week, the Dalian exchange is closed, limiting true price discovery on the bulk commodities until next week. Oil is softer ahead of weekly inventories, crude stockpiles expected to rise another 1.2mb after last week’s reported 0.919 gain. WTI is down 1.19%, only partly reflecting the big dollar’s uptick. Brent is down a lesser 0.25% as we go to print. Base metals on the LME have posted good gains (led by nickel +4.74%; copper +0.47%), the jump in nickel on the back of lower stockpiles in Shanghai and the LME. Among the softs, sugar prices rose 1.98%, US wheat futures also making some gains.

There is little to report with US Factory Orders the only release of note and follow the release of already-released Capital Goods Orders. Headline Factory Orders missed estimates, orders down 0.6% against expectations of a 0.3% gain. These moves are well within normal monthly volatility and don’t suggest any underlying shift in momentum. Core Capital Goods Orders for November were left unrevised at -0.6%. Noting to trouble the scorers from this report.

The UK Construction PMI was much weaker than expected at 50.6 from 52.8 prior and 52.5 expected. Anecdotes suggested Brexit-related anxiety and associated concerns about the domestic outlook continued to weigh on client demand. Of note the Employment Index hit a two and a half year low with concerns about the near-term outlook for new projects resulting in more cautious staff hiring.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.