Price growth edges lower despite reasonable economy

Insight

Markets have been choppy on the back of surprisingly poor retail numbers from the US.

https://soundcloud.com/user-291029717/hours-from-the-shutdown-solution-us-retail-shock-may-defeated

In the past hour, US Senate Majority Leader McConnell announced that President Trump plans to sign a bipartisan spending deal and then declare a national emergency to fund his border wall, averting another government shutdown Friday. “He is prepared to sign the bill,” McConnell said. “He will also be issuing a national emergency declaration at the same time.”

It’s a little bit of late tonic for the markets that have been on the defensive overnight. Stocks are off their session lows, the Nasdaq getting support from a good Cisco earnings report. Late in the session, equities are closer to square taking more heat earlier in the session from the big retail sales negative print, getting some renewed support from lower bond yields later in the session. US retail sales come in as a shocker, jobless claims ticked higher and the trade talks are not near being resolved as China printed a larger than expected trade surplus in January. UK PM May loses another vote in the House, but it seems inconsequential for now as she endeavours to re-fashion a deal with the EC, deadlines fast approaching.

The wire services were reporting yesterday that the 1 March increase in US tariffs on Chinese imports might be extended by 60 days, but overnight, the news flow has been pointing to a lack of fundamental progress on the US-China trade talks.

Amidst this now evolving least-bad contest of news and economic performance, there has been some tilt since late yesterday toward the JPY and the CHF, the NZD has made up some ground against the USD too, the DXY slightly lower. Even the Euro made some ground up against the USD, despite the German economy near to technical recession late last year. Sterling is lower on the Brexit political news, despite the likelihood still of either a deal or extending Article 50 for some months when push comes to shove in coming weeks.

The main news has been the “unbelievable” and shocking US retail sales release for December that fell 1.2% in headline terms, -1.4% excluding autos and gas and -1.7% for the so-called Control Group that feeds into GDP Consumption estimates. The Atlanta Fed slashed their estimate of US December quarter GDP from 2.7% to 1.5% in what was expected to be a good quarter for the economy into the distorting effects of the government shutdown and the polar vortex.

Many analysts were left dumbfounded by the release, it caught the attention of Fed Governor Brainard who was speaking, running counter to what’s been a still strong labour market. The equity meltdown? Maybe there is something in that perhaps, as there was from the apparent inability of seasonal adjustment factors to cope with the now-pervasive bring forward of (on line) sales into November from Black Friday and Cyber Monday. Perhaps revisions are pending.

The data though does open a risk the US economy might be slowing faster than commonly expected, also coming with a further tick higher in weekly jobless claims to 239K from 235K. Late last year, jobless claims were tracking to and testing 200K.

The German economy saw no GDP growth in Q4 after -0.2% in Q3, flat-lining, skirting technical recession. Euro GDP growth was left unrevised at a meagre 0.2%, Germany, France, and Italy all having a very soft second half, Italy having two negative quarters.

Besides the ongoing Brexit uncertainty (with the UK parliament voting against the government on a motion to support Theresa May’s approach to leaving the EU), dovish comments by BoE MPC member Vlieghe contributed to the fall in the GBP. Vlieghe said he thought the appropriate response to a no-deal scenario would likely be for either a rate cut or an extended pause, and even in the event a deal can be reached, signs of slowing in the global economy and weakness in UK domestic data meant that the Bank could “probably wait to see evidence of growth stabilizing and inflation pressure rising before considering the next hike in bank rate.”

US Treasury yields moved sharply lower after the retail sales release, with the 10 year rate falling from 2.7% to 2.64%, although it has since bounced back to 2.66%. Influential Fed Governor Brainard commented that the release had “certainly caught my eye”. Brainard noted that “it’s one month of data, so I don’t want to take too much signal from it. It certainly adds to a story where we want to take on board that there are some downside risks.”

Fed rate expectations fell, with the market pricing-out the few basis points of Fed tightening for 2019 and building in greater chance of rate cuts for 2020 (around a 2/3 chance of a rate cut is now priced by mid-2020). Elsewhere on the data front, weekly jobless claims were higher than expected, with the four week moving average moving up to 232k. Jobless claims appear to be trending gradually higher, indicative of some slight softening in the US labour market, although they remain at very low levels on a historic basis.

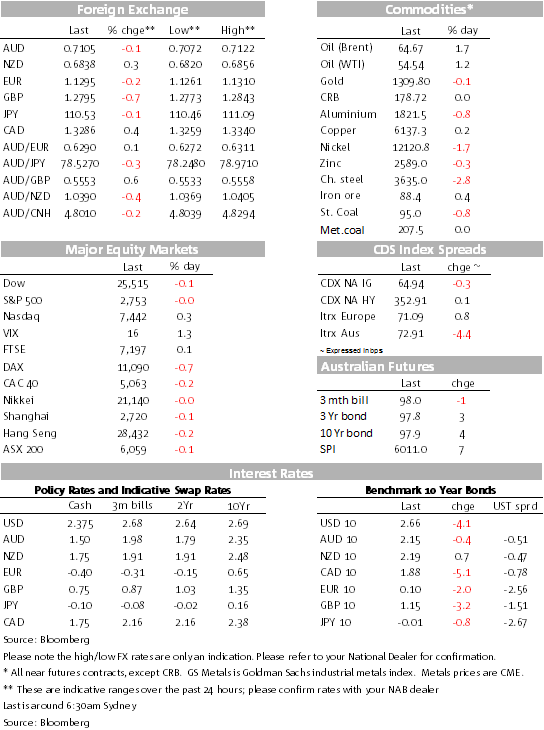

There haven’t been big moves overnight, oil getting some more support, iron ore seemingly finding a base in the high 80s for now, base metals mixed , gold square.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Price growth edges lower despite reasonable economy

Insight

Our view for the global economy is unchanged – we expect global economic growth to slow to 2.9% in 2024

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.