13 May 2026

13 May 2026

2026 Federal Budget: What it means for Business

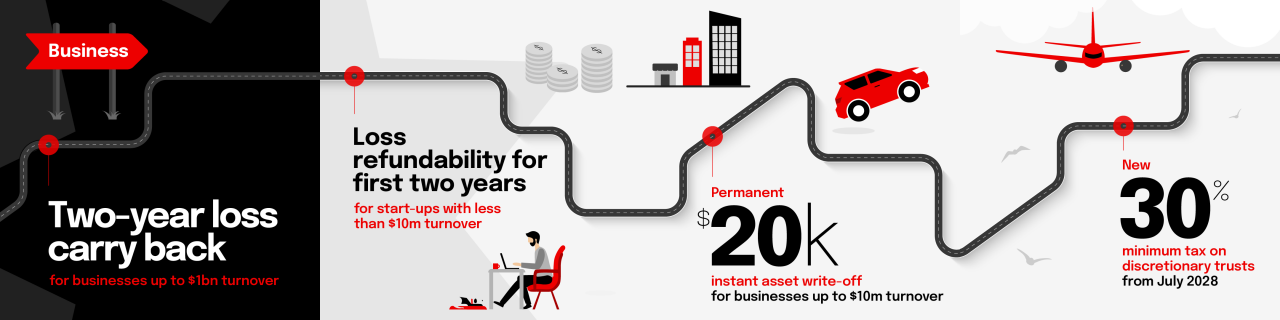

The reintroduction of loss carry backs for business was a significant feature of this year's Budget, while the instant asset write-off was made permanent.

Key Points

- Despite the energy shock and RBA tightening cycle, the cyclical starting point for the 2026-27 Budget was positive, with above trend GDP growth and a tight labour market. Relative to MYEFO, the deficits have improved by $45 billion over the forward estimates, as the government has elected to bank a portion of the improved revenue flows.

- The Budget forecasts that the underlying cash balance is likely to remain in deficit for the at least the next decade. The expected deficit for 2026-27 is $31.5 billion. The headline cash balance, which accounts for “off balance sheet” expenditure or investment, is forecast to be $64 billion in 2026-27, around 2.1% of GDP.

- Reform, restraint and resilience were the three self nominated pillars that were used by the Treasurer to frame the budget. Generally speaking, the Budget addresses all of these.

- Reforms were largely as pre-announced. Negative gearing has been removed except for investment in new builds. The CGT regime will move to an indexation framework, with a minimum 30% CGT tax payable on net gains. However, investors in new builds will have the option of choosing the indexation arrangement or the old 50% CGT discount.

- These reforms remove the incentive to deploy capital into low yielding/high debt investments in property. This is a benefit to broader financial stability, but will likely mean a small decline in house prices and near term upward pressure on rents.

- The government has been relatively restrained on cost of living measures, with the tax offset for working Australians small and not starting until July 2027.

- The government’s economic forecasts are broadly in line with the RBA’s and our own numbers. Growth will slow, inflation will rise and the unemployment rate will drift higher.

- We assess the stance of fiscal policy as neutral for the coming financial year, although this represents a change from expansionary fiscal policy in 2025-26. As such, the change in fiscal settings will better align with the RBA’s monetary policy ambitions.

What has the budget delivered for business

Concessional Capital Gains Tax (CGT) discount removed

From 1 July 2027, the 50% CGT discount will be replaced by cost base indexation for assets held for more than 12 months, with a 30% minimum tax on net capital gains. These changes will apply to all CGT assets, including pre-1985 CGT assets. Investors in new residential properties will be able to choose either the 50% CGT discount or the cost base indexation and the minimum tax.

Negative gearing

From 1 July 2027, losses from established residential properties will only be deductible against rental income or the capital gains from residential properties. Excess losses will be carried forward and able to be offset against residential property income in future years. Negative gearing will continue to be available for new residential property.

Discretionary Trusts

From 1 July 2028, the introduction of a 30% minimum tax on discretionary trusts.

Working Australians Tax Offset (WATO)

From 1 July 2027, a permanent annual tax offset of $250 for income derived from work.

Instant tax deduction

From 1 July 2026, an instant tax deduction of up to $1000, with no need to itemise and claim work-related expenses.

Instant asset tax write-off

From 1 July 2026, the $20,000 instant asset write-off for small businesses with turnover up to $10m will be permanently extended.

Tax loss carries back

From 1 July 2026, companies with turnover less than $1bn can carry back losses to offset prior tax paid up to two years earlier, capped by franking balances and limited to revenue losses.

Loss refundability

After 1 July 2028, start-ups with less than $10mn turnover can convert tax losses in their first two years into a refundable offset, capped by the firm’s FBT and wage withholding tax paid in that year.

National Health Reform Agreement (NHRA)

$18.1bn to increase Commonwealth funding for public hospitals.

Defence

Additional funding of $6.8bn over the next four years.

Fuel excise and heavy vehicle road user charge

From 1 April 2026, temporary reduction in the fuel excise and road user charge for heavy vehicle for 3 months.

Electric Vehicle Discount

EV tax concession to be scaled back based on vehicle value, with the full FBT exemption retained only for lower-priced cars (under $75k from 2027) before transitioning to a flat 25% discount for all eligible EVs by 2029.