Capital Markets

January 13, 2026

Takeaways for the A$ corporate funding menu

By Brad Peel

A stellar $33 billion year for corporate issuance, coupled with an expanding investor base, range of issuance and overall capacity has the Australian Medium-Term Note (AMTN) market well-placed as a core funding source moving ahead.

Hybrids and high-yield bonds have helped drive a banner $33 billion year of Australian corporate issuance[i], with expanding investor breadth, issuance range and market capacity all offering key insights for 2026.

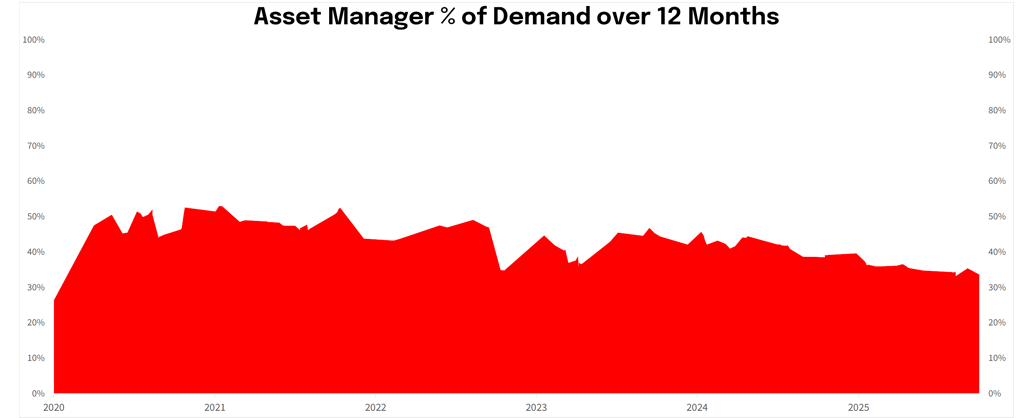

The broadening investor base has been an ongoing theme for Australian Medium-Term Note (AMTN) market participants for several years now, adding valuable new perspectives as much as the extra money in the mix.

Depending on the sector and structure, the traditional domestic asset manager bid is today regularly augmented by domestic aggregators or brokers, such as JBWere.

At the same time, Asia-based investment is providing additional asset managers, bank balance sheets and private banks, all joining the hedge fund and securities house interest traditionally underpinning demand.

Looking proportionally, this array of offshore investment has in fact more than doubled in the past decade, up from 25% in 2015 to 53% today[ii]. The past 12 months has also seen the middle market rise from 6% to 14%[iii].

Source: NAB-led corporate bond orderbooks

The changes come as domestic fixed income balances in Australia’s superannuation system have also grown by 5.1% in the past year[i].

What this means is every existing demand segment today has more money dedicated to the market, at the same time as more investors are coming in – particularly those from neighbouring economies in Asia.

PwC’s report Digital and wealth opportunities in Asia Pacific, cites the region as having more than 290 million mass affluent investors, who together account for about 45% of the world’s wealth[ii].

The team at NAB see Australia’s proximity geographically, high-quality credits and rapidly expanding bond market as a key opportunity to grow the AMTN market, with the demographics of multi-generational wealth creation set to drive ongoing demand for fixed income product.

It’s a reason we’re holding the NAB Capital Markets Singapore Forum again in February this year, with the Asia financial hub and investor base tipped as an engine room for market growth in coming years.

Range of issuance

Of course, for the market to be meaningful to global investors there needs to be real opportunities across as much of the ratings, sector and structural spectrum as possible, which is something NAB continues to support.

Using a grocery analogy, investors need to be able to do as much of their shop as possible in the AMTN market without ducking over to the Reg S, SGD or HKD markets to pick up their subordinated notes.

Over the past year, we’ve seen hybrids again dominate the news cycle and mindset of many an investor, with 2025 achieving $7.6 billion[iii] of issuance. We also again saw a smattering of high yield and unrated issuance adding to the standard investment grade flow.

Kiwi, Euro and US borrowers again came to market and provided investors with $7.9 billion worth of opportunity for geographic diversification[iv].

Curves continued to flatten as we saw hybrid issuance push from the traditional five-year non-call period out to 10 and French utility EDF shattered tenor norms with a standout 20-year tranche.

We also saw more cyclical BBB- credits come into market, as well as some of the more ESG-challenged sectors, from gaming to commodities, find a bid that had been previously the domain of the Reg S investor base.

Looking at the mix and to use an apt Singapore reference, it’s like the six-dish express menu offered to investors in the 2010s now has tasting options to rival the entirety of the canal side restaurants lining the famed Boat Quay precinct.

Expanded capacity

There are many issuers who have historically looked towards the euro or US dollar through the ETMN (Euro Medium-Term Notes) or 144A markets respectively, simply because of the perceived lack of capacity in Australia.

While actual capacity is difficult to determine, a traditional market reference point seen in the early to mid-2010s put it about A$2 billion for total issuance by a single name.

Looking again today, however, the story may be somewhat different, with NBN Co alone having $6.55 billion[v] outstanding. While this figure is often dismissed as an outlier for what can be seen as a quasi-government issuer, it’s worth noting Transgrid also printed $2.2 billion[vi] in subordinated format in a single year.

We feel this instead points to the growing breadth of investors reshaping capacity constraints to put the market today at about five times the assumed maximum of a decade ago.

The main reasons for this include the growth in superannuation assets in domestic fixed income, a rough proxy for Australian fixed income funds under management (FUM) – up by 115%[vii] in the past decade.

And in the same period, the Asia and middle markets combined have increased from a quarter to two-thirds of market demand[viii].

So, while the domestic asset manager FUM base has more than doubled, the portion of demand has more than halved, meaning the total market should be almost five times bigger.

Even scaling some of the Asian and middle markets for more bearish conditions, or assuming a lower allocation rate, we’re still looking at a multiple of at least three times that of the 2015 market backdrop.

This shift means issuers in 2026 who are looking at $6 billion plus in total capital markets debt do not necessarily have to go to offshore markets like the EMTN or 144A unless this suits their needs.

Instead, the AMTN market has now clearly moved from being a source of diversification to being a core source of funds, with the extra “hometown” discount from better understanding the drivers of the credit, brand recognition and functional currency funding.

With this in mind, here’s to a prosperous new year while taking a fresh look at the dynamic ATMN market. We look forward to working with you further, whatever your funding needs or investment plans are for 2026.

Brad Peel is NAB Executive Director, Capital Markets Origination

[i] Quarterly superannuation statistics | APRA

[ii] PwC: Digital and wealth opportunities in Asia Pacific

[iii] NAB deal records

[iv] Ibid

[v] Bloomberg

[vi] Ibid

[vii] Quarterly superannuation statistics | APRA

[viii] NAB orderbooks

Corporate and Institutional