A shifting strategic outlook and ongoing funding gaps in the US are creating opportunities for private capital to invest in digital “AI factories” of the future and the energy infrastructure needed to power them.

Corporate and Institutional

June 16, 2026

Bank hybrid changes meet listed innovation

The listed instruments market has seen strong activity as investors continue to seek alternatives to bank hybrids, with NAB playing a leading role. Bernardo Roque and Stefan Visser explore recent developments.

The ongoing phase-out of bank listed hybrids has seen deal momentum continue from calendar year 2025 into the first quarter of 2026, with a range of potential alternatives coming to the listed instruments market for investors seeking the traditional benefits of steady income and liquidity.

The activity comes as significant capital is being returned to these investors after the prudential regulator’s decision in December 2024 to phase out Additional Tier 1 (AT1) capital instruments, also known as hybrid securities, as eligible regulatory capital.

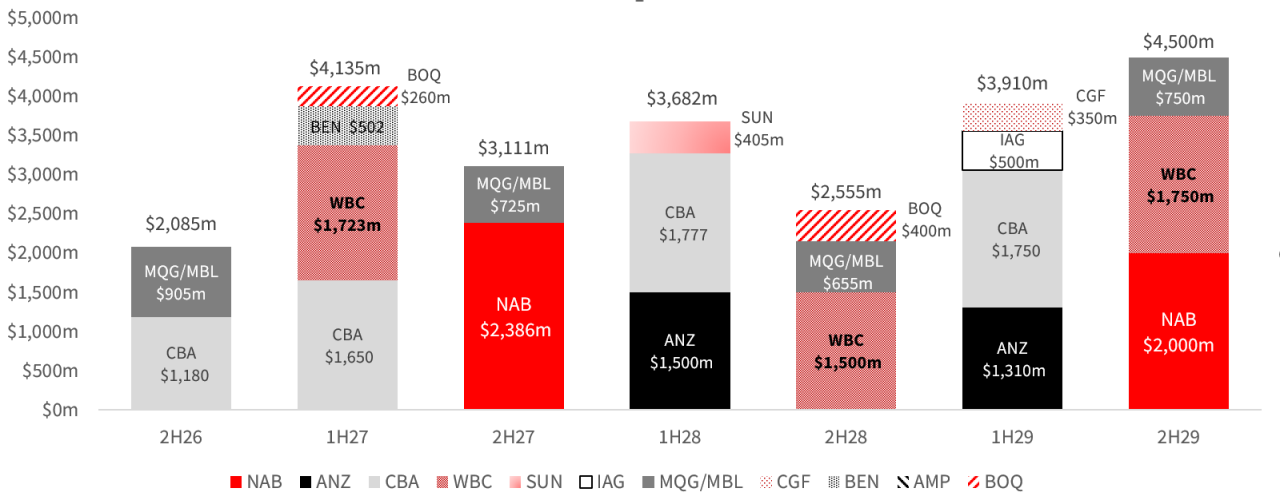

In practice this means the existing instruments are called by issuers without any forthcoming replacement, with call dates concentrated in May and June 2026 (see graph below).

Hybrids annual redemption profile until 2029

Source: NAB Capital Markets, company reports

The redemptions have been a key driver of positive market conditions in listed markets for issuers like Challenger, Revolution, MA Financial, Gryphon, Realm and more working with the NAB Capital Markets Origination team.

An elevated RBA cash rate since 2022 has also seen a continued cash build-up in investor portfolios and provided further liquidity tailwinds.

At the same time, a trend of long-term growth in the private credit space has introduced new investment opportunities underpinned by income-generating strategies with exposure to floating rate portfolios across corporate lending, RMBS/ABS, syndicated leverage loans and CRE (commercial real estate) debt.

The changing landscape has generated a range of new structures and innovative features in listed investment vehicles. One such innovation this year comes with ASX “listed notes”, spearheaded by fund managers such as Realm Investment House, Challenger Investment Management (CIM) and MA Financial.

These products provide investors with access to the underlying investment capabilities of professional managers by subscribing to a debt security, involving features like a fixed margin, monthly interest payments, equity enhancement contributions by the managers and a set call/maturity date.

Listed notes have appealed to a cohort of investors more comfortable with fixed income instruments having a set term rather than the permanent capital model seen in vehicles like listed investment trusts (LITs) and listed investment companies (LICs).

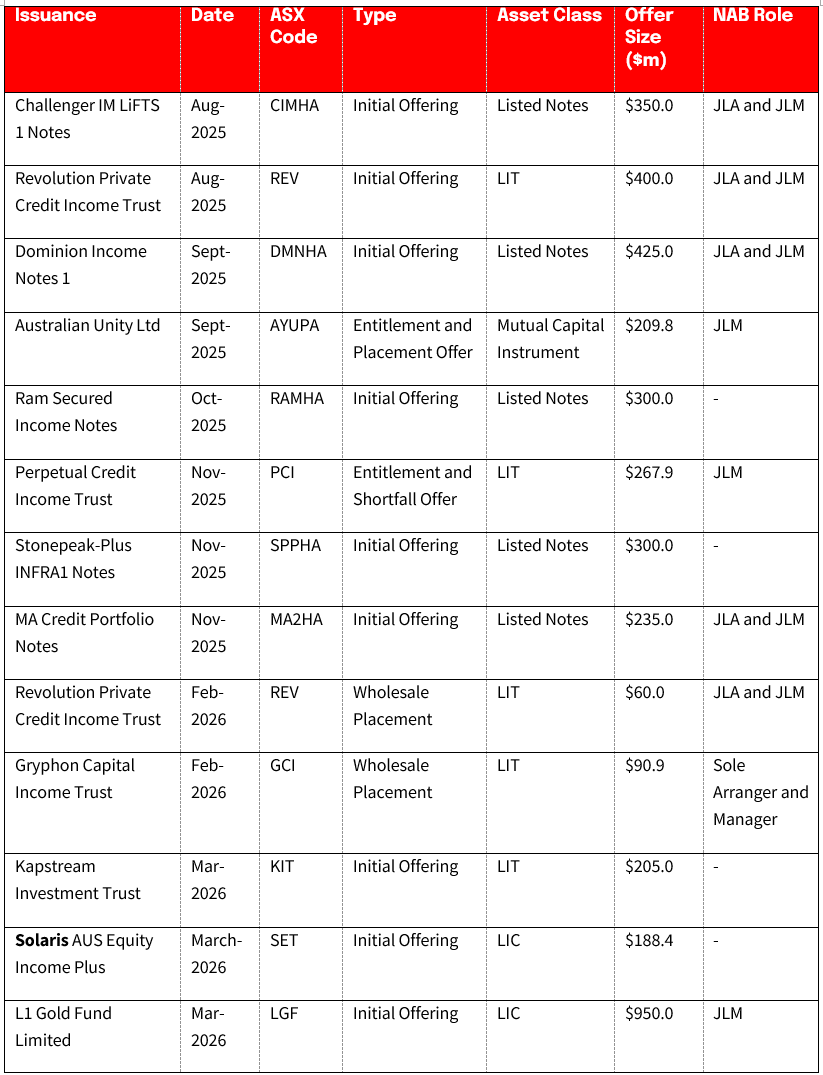

Following the Realm and CIM transactions, the market has seen issuances of listed notes from RAM, Stonepeak and MA Financial. There have also been new liquidity features in the LITs launched in CY2025 by Pengana, MA Financial, Latrobe, Revolution, and Kapstream.

Select transactions. Source: ASX reports.

The innovation includes limited quarterly off-market redemptions facilities available to investors, and the ability for managers to provide on-market support to trust units. The aim of these new features is to help mitigate the risk of these vehicles trading at a persistent discount to the underlying net asset value (NAV) per unit for extended periods.

Emerging challenges

Although activity has remained strong leading into 2026, a few headwinds started to emerge from the last quarter of calendar year 2025.

These came from both a sector and regulatory perspective and translated into slower bookbuilds and deals being printed at wider margins and smaller sizes when compared with previous months (see below).

*Margin bps over 1-month BBSW. Source: ASX reports

Relevant factors for these results include:

- Deal fatigue after a relatively large number of new issuances compressed into a short period;

- Some disturbance in market following the release of ASIC’s report on private credit in Australia, which while welcomed by the industry has led to investors taking some time to digest;

- General volatility and gated redemptions experienced in global private debt markets;

- Subdued secondary market liquidity for the newly established listed notes after strong support of the IPO bookbuilds;

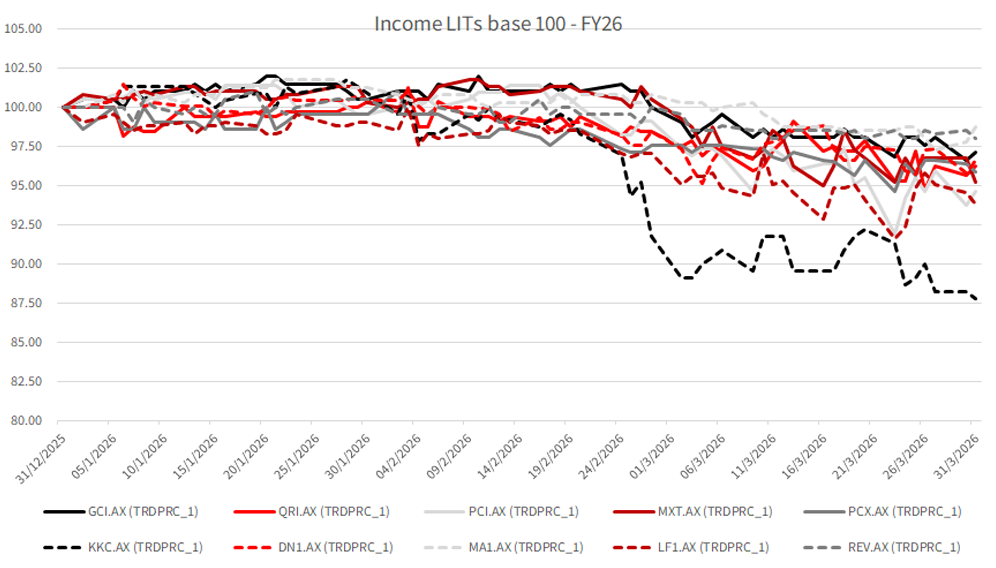

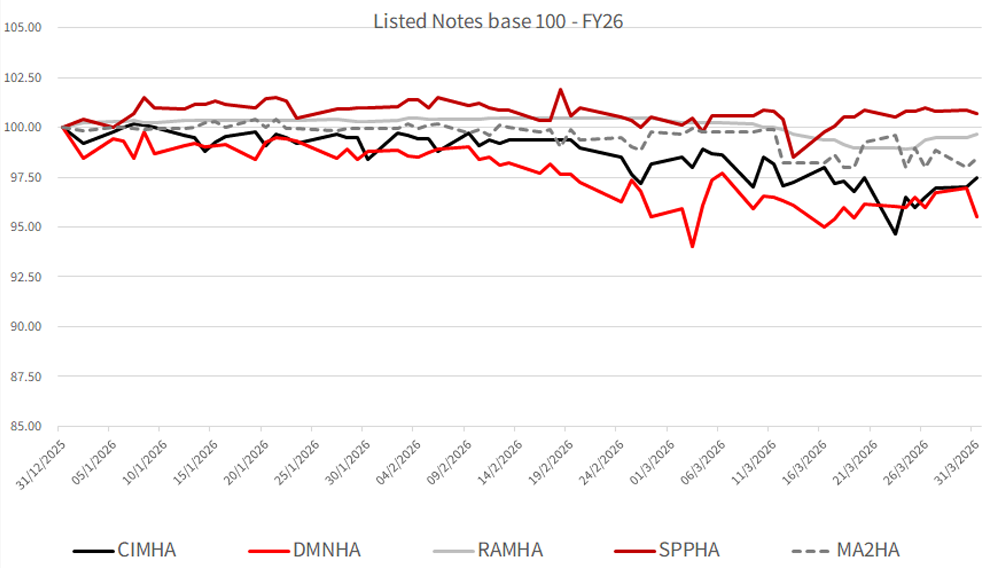

- General market volatility in listed markets with the Middle East conflict, has seen both LITs and listed notes trading at a discount to underlying net tangible assets (NTA) from late February (see following graphs), but with the notes generally performing relatively better.

Source: ASX, March 31, 2026

Source: ASX, March 31, 2026

In addition to the smaller price discounts relative to the LITs over the period, the notes have also demonstrated the benefits of extra product features including the value of the equity buffer.

All notes except ASX:DN1 (which is an LIT that invests into a note) have sustained a level of equity/first loss higher than their minimum requirements (see below).

1 As of 28 Feb 2026. Source: ASX Reports

Although acknowledging notes are still a small sample of recently listed securities, the resilience of the equity buffer in a period of volatility is an early proof point of how these structures can protect investors and support coupon payments and the NAV.

Market outlook

The subsequent trading of new listed investment vehicles (LIVs) that came to market during March and listed on the ASX in April also highlights the ongoing challenges for newly-established private credit vehicles.

The Kapstream Investment Trust, which has underlying exposure to global fixed income securities and private ABS, has faced some early challenges since listing when compared with equity-based vehicles L1 Gold Capital and Solaris Equity Income Plus, which both commenced trading at a premium to their IPO prices.

Ongoing concerns on geopolitical risk and uncertainty have weighed on activity in recent months, with deals being delayed through March and April.

Coupled with overseas market sentiment on private credit, the months ahead will need some careful navigation.

Given this environment, we expect investors to be increasingly selective with their new private credit allocations and continue to look to diversify their exposures into different asset classes like infrastructure and specialist equity exposures (both private and public).

We look forward to further helping our customers as these conditions continue to play out. Please get in touch with your banker for more information on the latest market developments and opportunities.

Bernardo Roque and Stefan Visser are Directors in the NAB Hybrids and Equity Capital Markets Origination team.

Topics

Small steps pay off for better insurance experience

ARTICLE

Real-time payment solutions offer the insurance industry a way to leap ahead on customer experience and retention by first solving key pain points before committing to larger scale transformation, NAB’s insurance specialist team says.