Robust growth for online retail sales observed in June

Insight

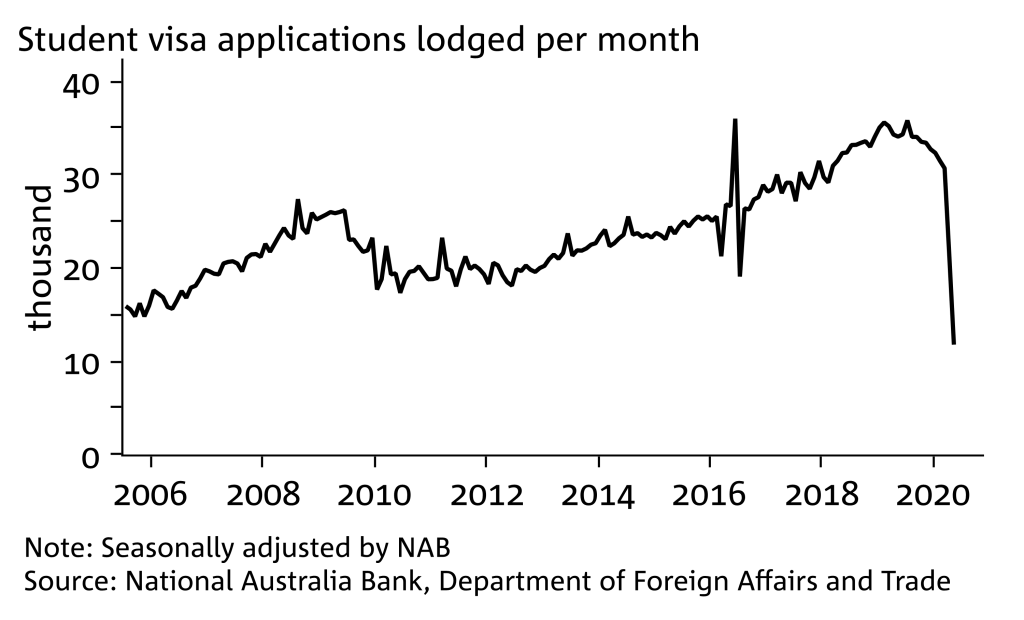

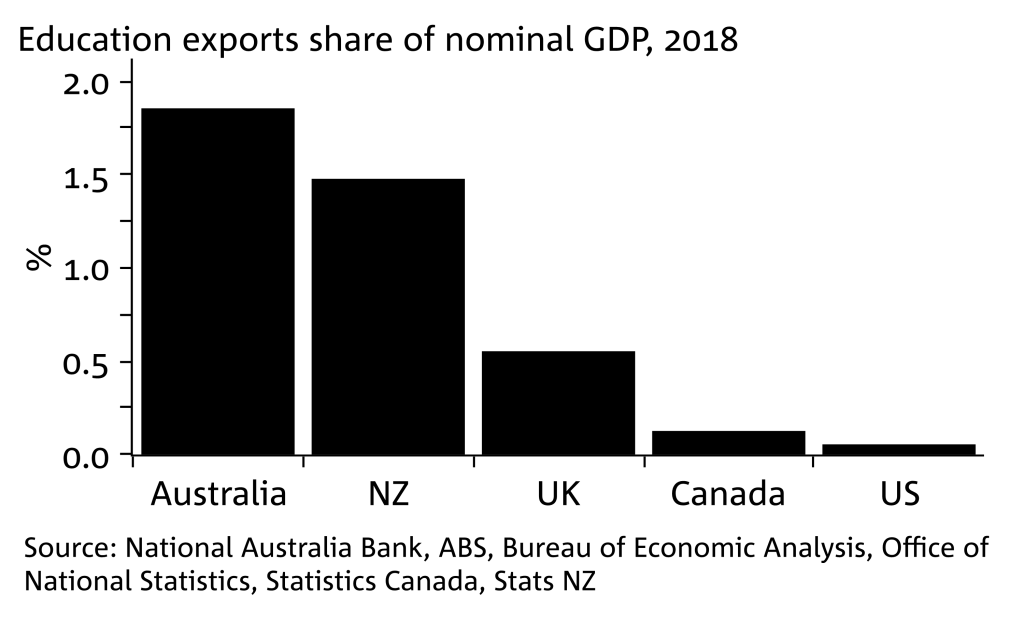

Education exports are likely to remain weak as international travel remains difficult and the global economy slowly recovers from a deep recession.

Australia. The focus is on COVID-19 case numbers, where markets are monitoring the outbreak in Victoria and whether this has spread to NSW. Thursday’s labour force data should show employment in June partially recovered some of the 835k jobs lost in April and May. We forecast a +175k rise in employment, but for even more people to re-join the labour force, such that unemployment will rise to 7.8%. Payrolls data will provide a timely indicator of labour market conditions in late June. NZ: Thursday’s Q2 CPI will show the start of a general decline in annual inflation over coming quarters. We look for -0.7% q/q, 1.3% y/y.

Global. US: COVID-19 numbers in southern states will remain a focus. Thursday’s retail sales for June is expected to rise 5.6% m/m after the big 16% leap the previous month. CH: Q2 GDP and June activity data are out on Thursday. Consensus for Q2 GDP sits at 9.6% q/q, a sharp rebound from the fall of 9.8% q/q in Q1 (annual growth 2.4% y/y). EU/UK: Trade discussions between the UK and EU continue. EU leaders will meet on Friday and Saturday to find an agreement on the EU Recovery Fund. The ECB meets on Thursday, but we expect no major news other than an economic assessment.

Student visa applications have collapsed; education exports are important for Australia

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.

Robust growth for online retail sales observed in June

Insight

Coming in for landing in a heavy cross wind

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.