Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

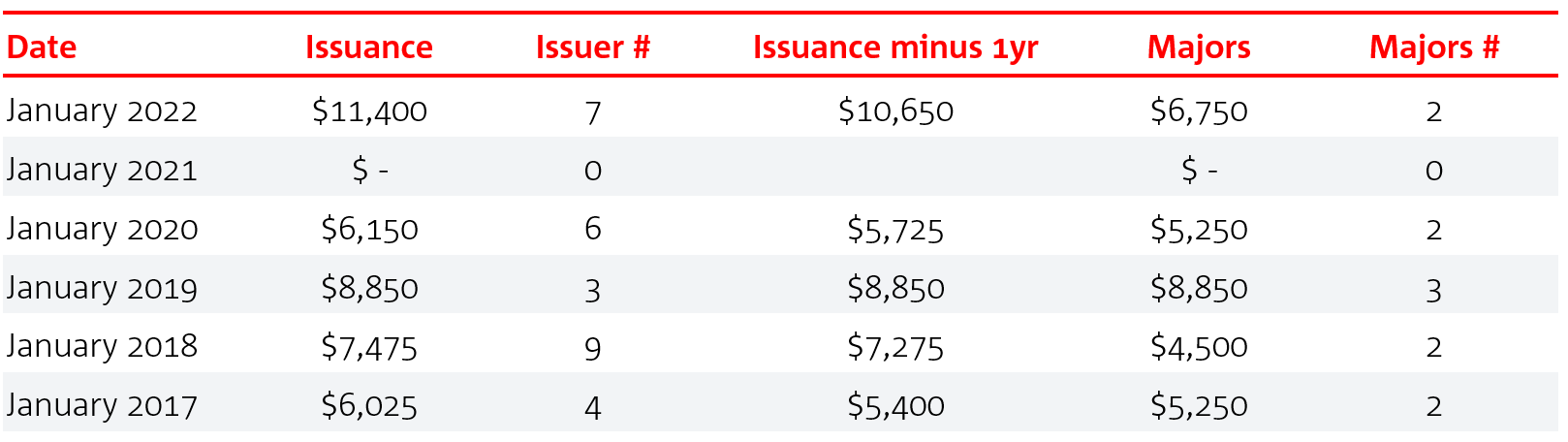

Business is already off and running for financial issuance as another fast-paced and active January kicked off the year.

If you’ve followed the Australian primary bond markets in the past six to seven years, you would know that January has become an active month for financial issuance. Corporate and securitisation issuance may be “parked” until February but bank issuance certainly isn’t.

The Australian dollar bond market is considerably bigger these days and this requires the attention of bank issuers, intermediaries and investors from the first week of the new year. This is especially so if you are a bank issuer with an expanded wholesale funding task this year.

This January has seen A$11.4 billion of financial issuance printed, NAB data shows, but except for the broader number of issuers, the month was simply a bigger version of the trend seen in previous years.

Even if we strip out one-year issuance, which has a different set of issuer and investor drivers, the issuance numbers in recent times are still impressive.

AUD Primary Bond Issuance – Financials – each January 2017-2022

Source: NAB

Large deals from the Australian major banks at the start of the year set the price and tone for the broader market. The momentum from these large deals usually carries the market along successfully until Easter. This year the positive sentiment from the CBA five-year print has allowed other issuers to swiftly follow into the market and most of these deals have been rewarded with respectable price and volume outcomes.

The exception in 2021, when zero issuance for financials were recorded, stems from when the term funding facility (TFF) was expanded and extended for ADIs1. The Australian dollar wasn’t as attractive at the time on an arbitrage basis for kangaroo bank issuers and the incentive to issue for domestic and kangaroo issuers just wasn’t there.

But back to 2022 and the question of why we have had more volume so far.

One answer is the banks drawn to the market all have more to fund and many decided it wasn’t worthwhile testing the market later with the greater event risks. According to our analysis, the greatest perceived risk has been how the US Federal Reserve will tackle rate hikes in 2022. Longer-dated US Treasury bonds were already sold heavily in January and issuers decided to fund while credit was holding in.

In addition, the RBA assessment of inflation, wage growth and underlying employment conditions in Australia, coupled with the unwinding of bond buying programmes also created uncertainty.

In the end they were correct.

So where does this take credit? There is still some uncertainty, but it is unlikely we will be pivoting 20 basis points either side of +50 for five-year senior unsecured major banks. As seen in market, the +70 level funded recently by CBA and Westpac for five-years feels like more of a midpoint than the higher end of the range as Australia heads back to more “normal” yield and economic structures.

The three-year RBA term funding facility rolled off in June last year2 and the banks who used the facility jumped back into the wholesale markets to lengthen their maturity profile. Despite the pandemic, mortgage origination at most Australian banks has multiplied significantly and there has been a big push into business banking as the economy recovered from the initial pandemic hit.

Senior unsecured spreads widened 25 basis points last September with the announcement that the committed liquidity facility (CLF) was being phased out, NAB data shows. Without the base of ADI investors, senior unsecured spreads funding levels have had to meet the wider investment targets of Australian funds and Asian commercial banks.

This year, despite the volumes issued and some offshore volatility in equities and rates, the tone still feels good. Asian investors have re-engaged, which is a positive. Without the ADIs buying each other’s paper and using the CLF, Asian commercial banks are a good alternative to provide a respectable base of orders which complements the larger tickets from the onshore accounts.

However, it does feel that AUD investment grade credit markets have to go a little wider still to fully engage the Australian asset managers who have been cautious so far.

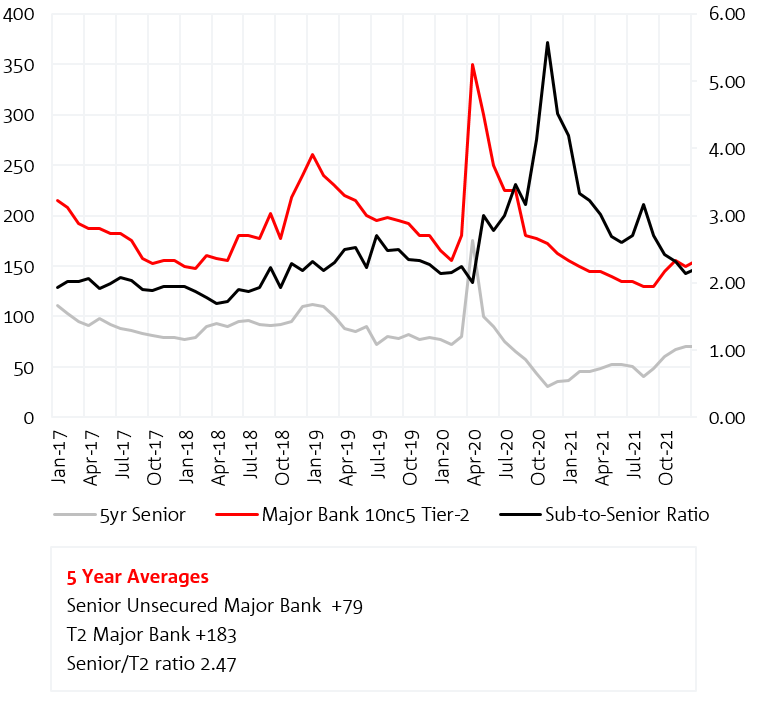

With all the activity in senior unsecured funding, it’s interesting to note it hasn’t affected tier-two levels. The recent APRA announcement of extended capital requirements3 didn’t disturb sentiment as the Australian banks have a high degree of natural capital generation.

The amount of issuance under the ALAC regime has been easily absorbed and issuers have refocused on funding a significant increase in senior unsecured. So there has been relative scarcity again in T2 product.

The majors, Macquarie and the regional banks will have T2 to print. However, the market hasn’t adjusted much to the widening of senior unsecured in recent months. The levels look attractive to fund at in absolute terms and on a ratio basis.

Source: NAB

It’s good to see that the Australian market has really locked into building trade momentum in a more organised and transparent manner.

Clear signalling to investors of book size, expected print volumes and timing is all helping to drive the movement. In Australia we are not lining deals up 15 to 20 basis points back from expected final landings. That adjustment is the norm in US dollar and euro senior deals for well-rated IG banks. A more manageable 5 basis points for senior unsecured deals is the current differential and the market feels more balanced for it.

Many years before the mandate/IOI process was established, we launched at the expected landing level and any basis points inside were hard fought for. That created much uncertainty as the deals were built. Now at least it is clearer to the issuer and investor how the deal is unfolding and what the likely outcomes will be. It provides issuers with greater volume/price options and investors clarity of issuer intentions for the benefit of all participants.

Bearing all this in mind, the industry looks forward to continuing the deal momentum into the rest of 2022 and beyond.

____________

1 NAB data

2 Reserve Bank of Australia media release 3/11/2020, Term Funding Facility – Reduction in Interest Rate to Further Support the Australian Economy

3 APRA letter 2/12/21 Letter – Finalising loss-absorbing capacity requirements for domestic systemically important banks (apra.gov.au)

Fiscal stimulus likely too late to boost 2024 growth, but may add some upside to 2025 forecasts

Insight

Sharing experiences and leadership lessons to help promote gender diversity across the property finance and infrastructure value chains has been in focus at recent flagship events for NAB Corporate and Institutional Banking customers.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.