Volatility in equity capital markets has been a key feature of the past year’s activity and factors such as COVID-19, geopolitical tensions, global economic growth, interest rates and inflation will all have an impact in 2022.

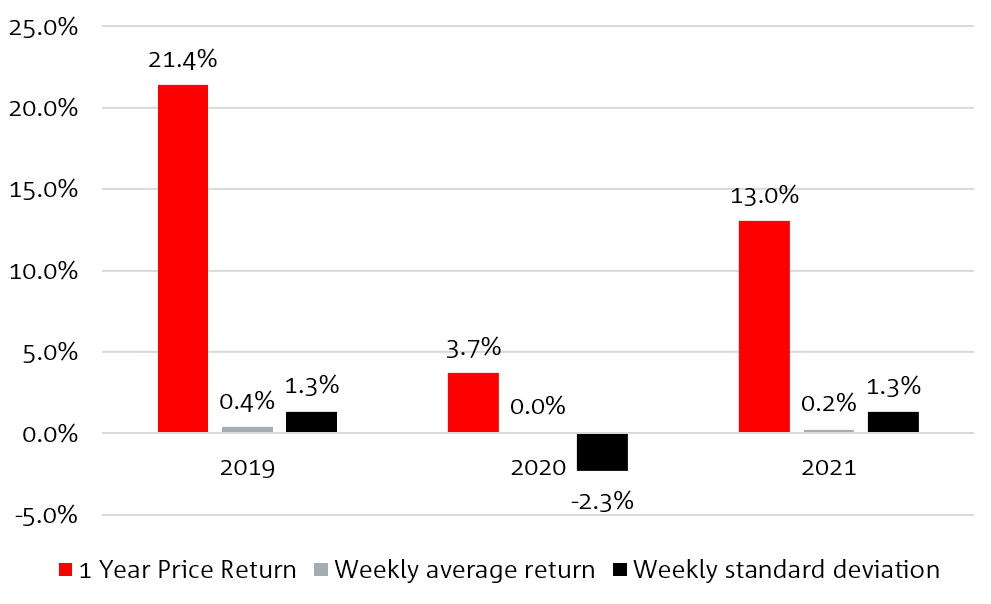

Over the past three years, equity market performance1 has varied considerably, with 2019 delivering strong returns with low volatility, 2020 poor returns with high volatility, and 2021 more stable despite dealing with ongoing COVID-19 lockdowns, labour shortages and supply chain disruptions.

ASX200 price index

Source: IRESS

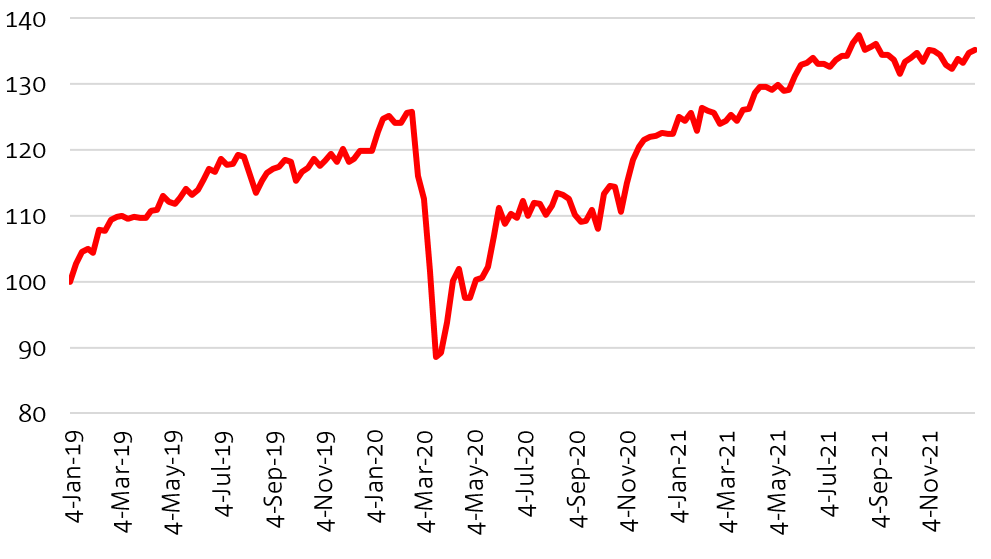

For those investors who were brave enough to buy equities during the March 2020 sell-off, the ASX200 price index has delivered more than a 50% return to 31 December 2021. More relevant however is that the three-year cumulative performance of the ASX200 is approximately 35%, a significant return for investors who were able to ride the volatility over the period.

ASX200 Price Index

Source: IRESS

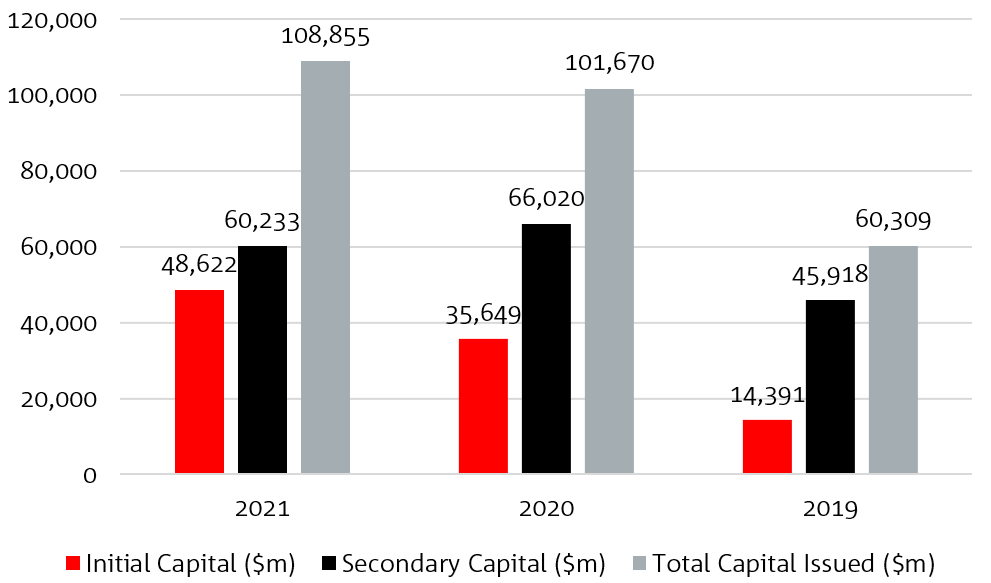

The past three years also provide an interesting snapshot in relation to capital raised on the ASX2.

Initial and secondary capital raised on ASX

Source: ASX Market Statistics

In 2019 approximately $60 billion was raised across the market, 76% of which was via secondary offerings made by ASX-listed entities, with limited capital raised in the primary market for new IPOs.

in 2020, we saw approximately $102 billion raised on the ASX, a 68% increase on 2019. 65% of the capital raised in 2020 was via secondary offerings, which included several large raisings for companies who looked to repair balance sheets on the back of COVID-19 impacts. In 2021 we saw $109 billion of capital raised, a new record for the ASX.

Only 55% of this capital came via secondary offerings as existing entities not only sought capital for balance sheet support but also to fund organic growth or make strategic acquisitions.

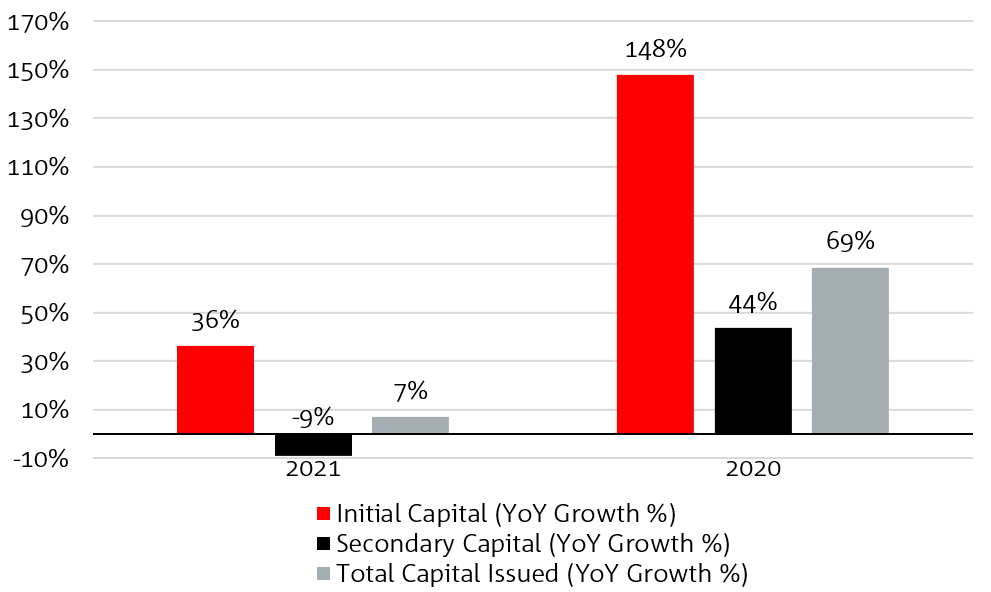

Initial and secondary capital raised on ASX – year on year growth %

Source: ASX Market Statistics

Interestingly in 2021, 45%, or $49 billion, was raised in the primary market for new IPOs. This represented growth of 36% year on year, as market conditions were amenable to new product and several IPOs of more than a billion dollars were brought to market as well as a long tail of small and mid-cap offerings.

As we look to the future, it is clear that 2022 will be another fascinating year for equity capital markets. This year will be different however given new drivers which the market faces. Geopolitical tensions in Europe, new variants of COVID-19, global inflation, changes in monetary and fiscal policy globally and domestically, currency fluctuations, employment, wages growth and interest rate movements will have a meaningful impact.

With these factors in mind, here are five important thematics for both investors and issuers in the ECM space to consider in 2022:

Key issuer thematics

Interest rates: Movements in interest rates will have an impact on a company’s profitability, as cost of capital rises over time. Careful attention will be required to manage this risk to ensure cash flow stability, appropriate reinvestment into the business and maintain shareholder returns.

Timing is everything: There will be limited windows of opportunity throughout the year to raise capital, due to distractions such as reporting season(s), public holidays, school holidays, a federal election and the unknown next iteration of COVID-19. After a very busy 2021, it feels like it may be another big year for capital raising across the market, so be prepared and flexible in relation to any equity capital needs.

Strategy is critical: This may sound obvious, but the current climate calls for additional focus on items such as COVID-19 contingencies, ESG strategy, supply chain logistics, workforce planning, geopolitical risks and fiscal and monetary policy settings and currency fluctuations for import/export businesses or businesses with offshore exposures.

ESG focus is a must-have: In recent years, debt capital markets issuers have developed frameworks and products to meet various ESG principles and strategies. This focus will become equally important in equity capital markets, as investors continue to screen companies based on ESG principles, particularly in relation to decarbonisation, board and management diversity and socially responsible business practices.

Alternative sources of capital: Given the complexities of raising capital at particular points in time, 2022 may present an opportunity for alternate sources of capital for some businesses. Depending on the maturity of a business, pre-IPO capital, private equity structures, convertible notes, strategic cornerstones and more may prove appealing this year.

Key investor thematics

Interest rates: Importantly, interest rate rises are normally linked to a desire to slow a rapidly growing economy, and a growing economy is generally a positive environment for investing in equities. However, we must acknowledge that interest rate rises in 2022 will potentially impact an investor’s required rate of return, asset allocation, sector allocation and security valuations. Now is the time to consider the implications of rate rises and what that may mean for your portfolio.

Why investing in equities still makes sense: If interest rates do rise in 2022, forward curves predict a modest increase in line with pre-pandemic levels. These levels are still very low in a historical context. Volatility in equity markets due to interest movements may in fact provide opportunities to acquire shares in companies with good long-term prospects, at reasonable prices, particularly for investors with a long-term investment horizon. With cash rates predicted to remain at historic lows for 2022, and inflation rising, investing in equities still makes sense.

Stock selection: Growth stocks have delivered very good returns over recent years, particularly in the technology sector. They have benefited from cheap and plentiful capital, high valuations and changing consumer preferences driving revenue, albeit profitability is sometimes uninspiring. Value stocks have tended to underperform, however the outlook for 2022 appears brighter as a rotation towards value during uncertainty is likely. Style aside, stock selection will be critical in 2022 and picking the beneficiaries of the current market environment will be a major focus for investors. Covid impacted sectors such as airlines, travel firms, hotels, and certain retail may start to look appealing at some point.

ESG: Investors will be more focused than ever on ESG principles in 2022. This will drive investment decisions and access to capital. We may well see new “climate technology” companies emerging focused on renewable energy, batteries, hydrogen, and other forms of decarbonisation and emissions management.

Property (excluding residential): Australian investors are typically overweight in property and so this sector will be topical. For commercial property, investors typically have exposure via listed or unlisted REITs. Upward interest rate movements ordinarily have a negative impact on commercial property values over time, as discount rates and capitalisation rates increase. However, a stronger economy should ensure that rent levels and occupancy remain strong, so income should be sustainable and growing. Volatility in pricing of listed REITs is likely, however unlisted REITs will remain stable from a pricing perspective. It is likely that property subsectors will perform differently this year, with industrial/logistics and healthcare remaining strong, office at an interesting inflection point, and retail performance being dictated by the discretionary or non-discretionary nature of the tenants.

____________

1 Data sourced from IRESS 2 Data sourced from ASX.com.au Market statistics, accessed February 8, 2022