We've captured the standout insights from the event series in an investor-ready eBook.

Report

Markets remain at the high end for valuations, but significant sell-off in select stocks creates potential opportunities for investors

Executive Summary

Equity markets fell in March, with the S&P/ASX 300 Accumulation Index down -2.50% and the US S&P 500 index down -6.16%. Markets were down sharply at the start of the month before recovering some losses by month end. The primary cause of the broad-based weakness was concerns about US economic growth, driven by tariff uncertainty and the impact of higher bond and credit yields. The tech-heavy NASDAQ benchmark was down -8.14% for the month. European markets fared slightly better, benefitting from ongoing rotation from investors seeking alternatives to the US. The STOXX Europe 600 benchmark was down -3.72%.

Bond yields rose slightly in March. The US 10-year bond edged up 1 bps to 4.21% but was higher mid-month. In Australia, the 10-year bond rate was up 13 bps to 4.42% bps. In Australia, the key economic data was the release of February CPI numbers that came in broadly in line with market expectations.

The numbers continued to show lower inflation, however, the services-based component continues to print above 3% levels and remains stubbornly sticky. The impact of fuel rebates continues to favourably distort headline CPI numbers. Unemployment numbers were also released in March, showing a surprising fall in employment numbers, with older workers more impacted. The market will continue to monitor these numbers to determine if there is a new downward trend in employment.

The RBA has previously noted that the enduring strength in employment was a potential roadblock to further rate cuts. In the US, the Federal Reserve maintained rates at the current level with minimal changes to the dot-plot projections. The dollar index continued to weaken.

Commodity markets were generally positive in the month, benefitting from a lower US dollar. Copper was up strongly on concerns that President Trump may look to impose tariffs on copper imported into the US. The US currently imports more than 45 per cent of its copper requirements. Gold continued to hit record highs with the yellow metal topping US$3000 for the first time and closing about US$3100. US deficit fears, higher inflation and ongoing geopolitical concerns contributed to its strength. Oil was stronger despite the increased supply expected to flow from more favourable operating conditions in the US and concerns of lower demand from a slowing economy. Iron ore was broadly flat, continuing to hover around the US$100 level.

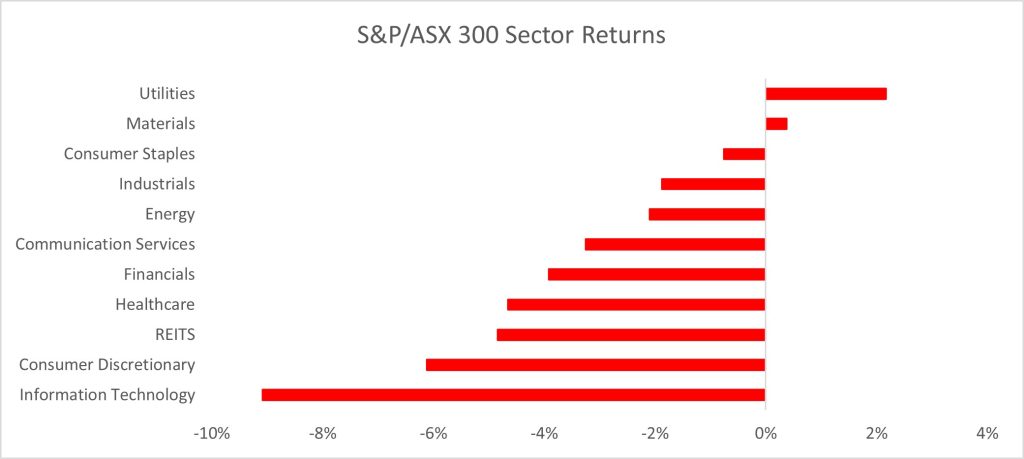

In Australia, defensive sectors such as utilities and consumer staples were among the better performing sectors in March, reflecting the defensive characteristics of these sectors under more volatile market conditions.

Materials were boosted by strong moves in gold and copper prices. A rotation out of banks into resources also helped the sector. The IT sector was weaker on negative leads from the US NASDAQ benchmark amidst concerns of over-valuation and a general market rotation from growth stocks into value stocks.

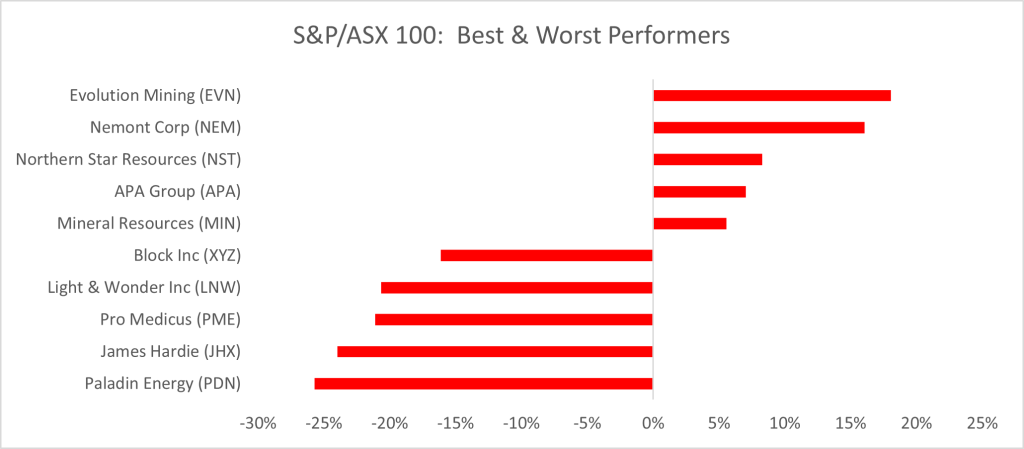

Stronger commodity prices and the rotation into banks boosted resources. Record gold prices boosted gold miners including Evolution Mining, Newmont Corporation and Northern Star. Mineral Resources bounced off February lows, despite another incident on its troubled Onslow Mine road.

James Hardie was down sharply after announcing the acquisition of AZEK, a US-based building supplies company focusing on outdoor building materials. Although analysts acknowledged the strategic rationale, there were concerns that the company had overpaid. The AZEK acquisition will also lower James Hardie’s margins and return on capital metrics. Pro Medicus was down as the market rotated away from expensive growth stocks, preferring more defensive, cheaper names.

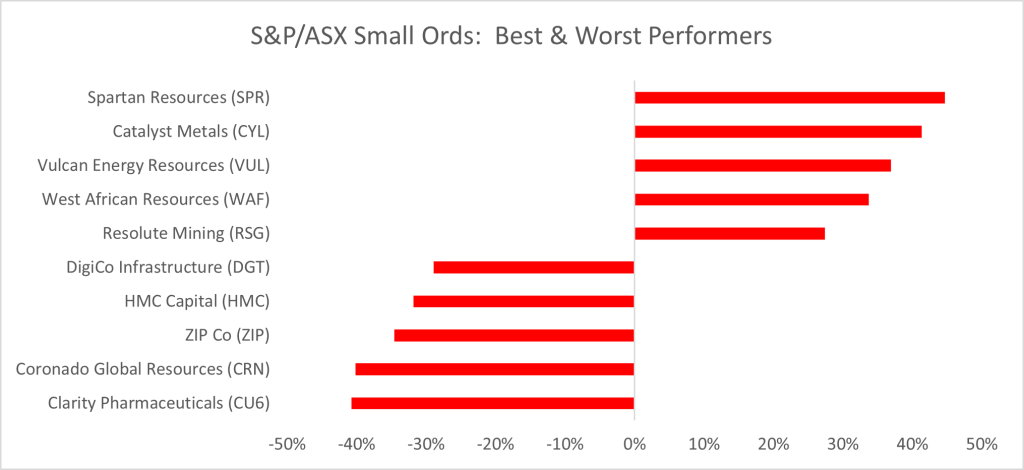

Gold miners again dominated the best performers list for small-caps with 4 out of the top 5 being gold producers. Concerns on the US-consumer saw ZIP continue to weaken. Mortgage insurer Helia Group announced that Commonwealth Bank has entered exclusive negotiations with an alternate provider of mortgage insurance services. CBA contributed 44 per cent of Helia’s gross written premium in 2024, highlighting the significant drain on the company. HMC Capital continued to weaken on concerns of the quality of some private credit assets.

From a US style perspective, low-volatility factors performed well, reflecting the more volatile market environment. Value-based factors also delivered solid performance. Momentum and growth factors underperformed reflecting the market rotation away from expensive growth names.

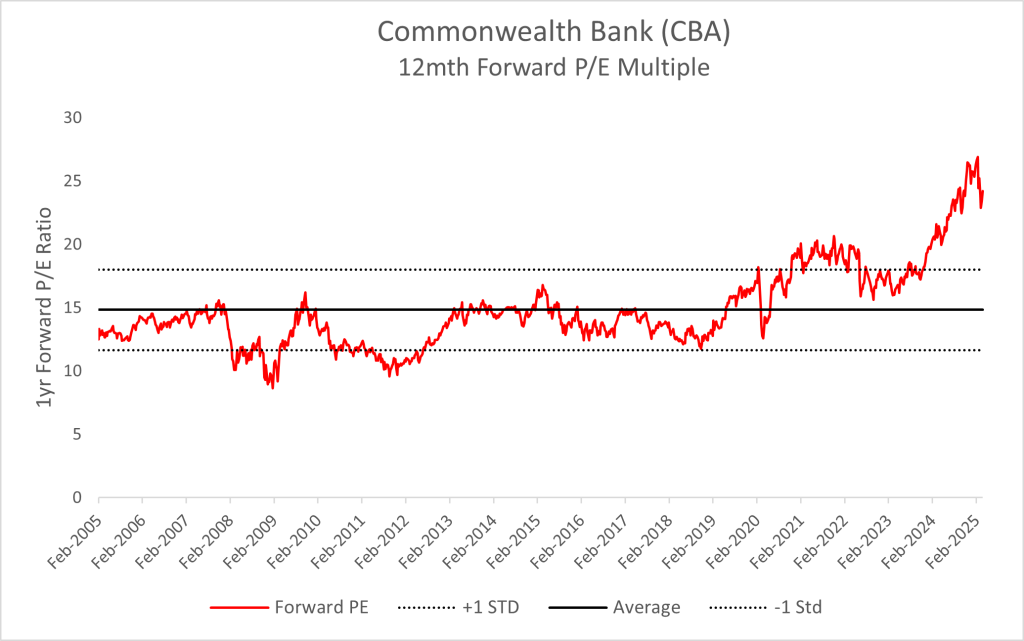

After a stellar 2024, banks fell again in March. The catalyst for the weakness was a combination of:

Despite these falls, Commonwealth Bank (CBA) still appears to be expensive compared to historic multiples.

* Further escalation of global trade tensions, particularly in light of the upcoming ‘Liberation Day’ announcements.

* Persistence of inflation above central bank targets.

* Deterioration in credit quality across Australian banks.

* Resource sector volatility due to fluctuating Chinese demand.

* Ongoing weakness in growth stocks as the market rotates to cheaper segments of the market.

The Australian market continues to be dominated by geo-political themes and Trump policy concerns. The upcoming Australian election will also prolong uncertainty. Although valuations have retreated slightly due to falling share prices, the Australian market remains fully valued at current prices. However, there are many stocks that appear to have been oversold, creating opportunities for investors.

To discover more call 1300 683 106 or email us on investordesk@nab.com.au

The information contained in this article is believed to be reliable as at April 2025 and is intended to be of a general nature only. It has been prepared without taking into account any person’s objectives, financial situation or needs. Before acting on this information, NAB recommends that you consider whether it is appropriate for your circumstances. NAB recommends that you seek independent legal, property, financial and taxation advice before acting on any information in this article.

©2025 NAB Private Wealth is a division of National Australia Bank Limited ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.

The information contained in this article is intended to be of a general nature only. It has been prepared without taking into account any person’s objectives, financial situation or needs. NAB does not guarantee the accuracy or reliability of any information in this article which is stated or provided by a third party. Before acting on this information, NAB recommends that you consider whether it is appropriate for your circumstances. NAB recommends that you seek independent legal, property, financial and taxation advice before acting on any information in this article. You may be exposed to investment risk, including loss of income and principal invested.

You should consider the relevant Product Disclosure Statement (PDS), Information Memorandum (IM) or other disclosure document and Financial Services Guide (available on request) before deciding whether to acquire, or to continue to hold, any of our products.

All information in this article is intended to be accessed by the following persons ‘Wholesale Clients’ as defined by the Corporations Act. This article should not be construed as a recommendation to acquire or dispose of any investments.

We've captured the standout insights from the event series in an investor-ready eBook.

Report

The level of bonds in an investment portfolio will be determined by your asset allocation strategy combined with risk preferences and income needs

Article

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.