Firmer consumer and steady outlook

Insight

Investors are seeking diversified unique investment alternatives more than ever, with further opportunities opening up this year as managers deploy a range of actions to provide value.

2021 capped off an incredibly active equity IPO market and with it a busy year of capital raising for existing Listed Investment Companies and Trusts (LIVs).

After the volatility of early 2020, the ASX continued to experience substantial investor growth for pooled investment vehicles, both via ETFs as well as LIVs. Investors are seeking diversified unique investment alternatives more than ever.

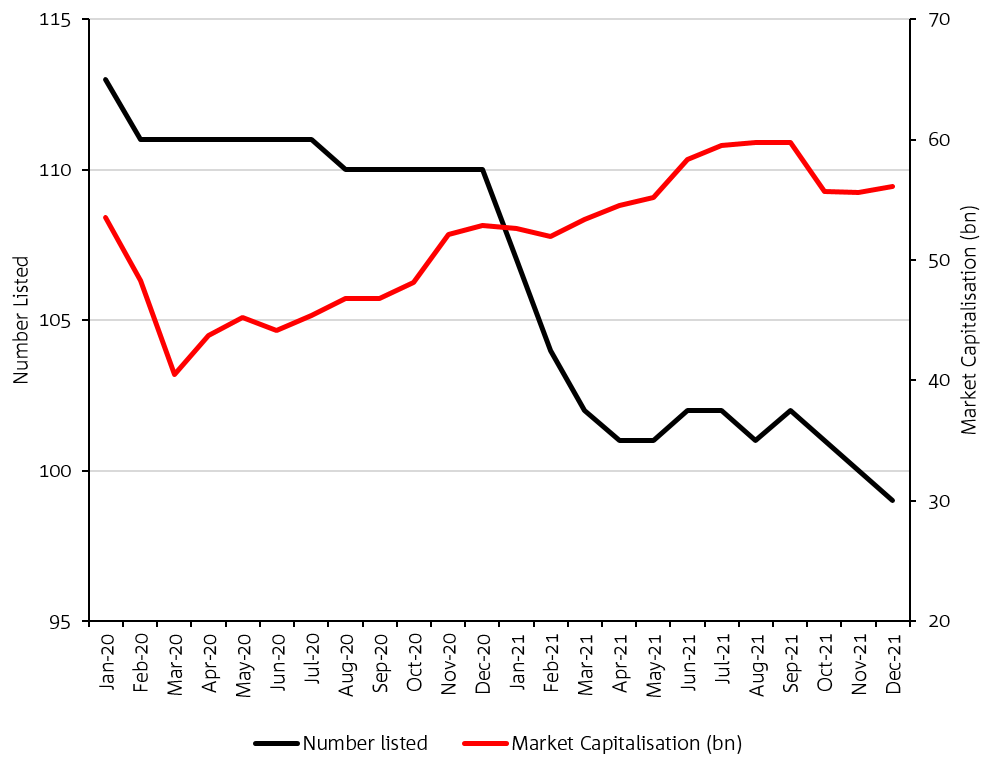

Based on reports provided by the ASX1, as at the end of March 2020 a total of 111 LIVs were listed on the exchange for a total of $40.46 billion, with growth tracked in the chart below.

Market summary: LIC Market Growth

Source: NAB graph based on ASX Investment Products Reports2

Though not in a linear fashion, what has transpired is that managers who provide a clear value proposition to investors have been given the opportunity to continue to grow their investor base.

As at the end of December 2021 (from ASX reports), the market capitalisation of the LIV market grew to more than $56 billion.

In addition to capital growth and general investment performance, the growth in market capitalisation has been because of several capital management alternatives deployed by successful managers to continue to grow their vehicles (underpinned by investor demand).

These alternatives include:

It is also worth acknowledging that the Australian market is not unique in our experience of increased capital raisings for existing managers, with similar trends being observed in the “LIV” markets in the UK.

In addition to the number of fundraising alternatives undertaken by existing vehicles trading at premiums, 2021 also saw the IPO of a specialist LIC to the value of $225 million3.

Though admittedly this vehicle was raised by an experienced LIC manager, it has certainly provided another data point that investors continue to be supportive of managers where the value proposition fits the closed-ended nature of LIVs and where managers can provide a differentiated, proven strategy.

The growth seen since March 2021 for individual successful managers is even more notable, especially considering we have seen a number of LIVs required to take steps to manage unitholder and shareholder interests appropriately, leading to the 111 LIVs as at March 2020 reducing to a total of 99 as at December 2021 per the ASX reports.

There is a clear bifurcation during this period where the winners have been rewarded handsomely compared to some of the less loved having to take steps in the other direction.

Examples of capital management actions taken by this latter cohort included:

No doubt 2020 was a consolidation year for a vehicle/market that has been around for about a century, with trading price discounts versus NTA at the peak of COVID blowing out to levels never seen before on all managers – even those well-proven and successful.

However, the divergence after that point is further illustrated with the list of vehicles now trading at premiums once again continuing to grow, including in both the equity-based sector as well as fixed income-based LIVs (as seen in monthly reports from Independent Investment Research4).

Admittedly the same data shows not all participants currently in the LIV market are in this beneficial position, with some LIVs on market continuing to trade at discounts to NTA, thus leading them to continue to deploy buybacks, substantial founder investment in the secondary market and increased marketing resources in an attempt to liaise with existing holders to gain back support.

Based on the LIV market growth illustrated above and high levels of capital raising activity observed in late 2021, it would seem a good bet that 2022 will realise continued capital raising activity by managers trading at premiums (though investors will continue to carefully scrutinise the appropriateness of existing investment opportunities for those managers).

The growing momentum and supportive data points noted above would also suggest that opportunities again exist for very high quality new entrants to consider the Australian LIV market. Although after the experience in 2020, scrutiny from investors on vehicle structure (including management of discounts to NTA), investment benefits of a closed-ended nature and a manager’s experience in managing a retail vehicle will be higher than ever.

____________

1, 2 https://www2.asx.com.au/issuers/investment-products/asx-funds-statistics

3 https://www.theaic.co.uk/aic/news/press-releases/investment-company-2021-review-0

4 https://independentresearch.com.au/

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.