AMW: What happens to consumption as we learn to live with the virus?

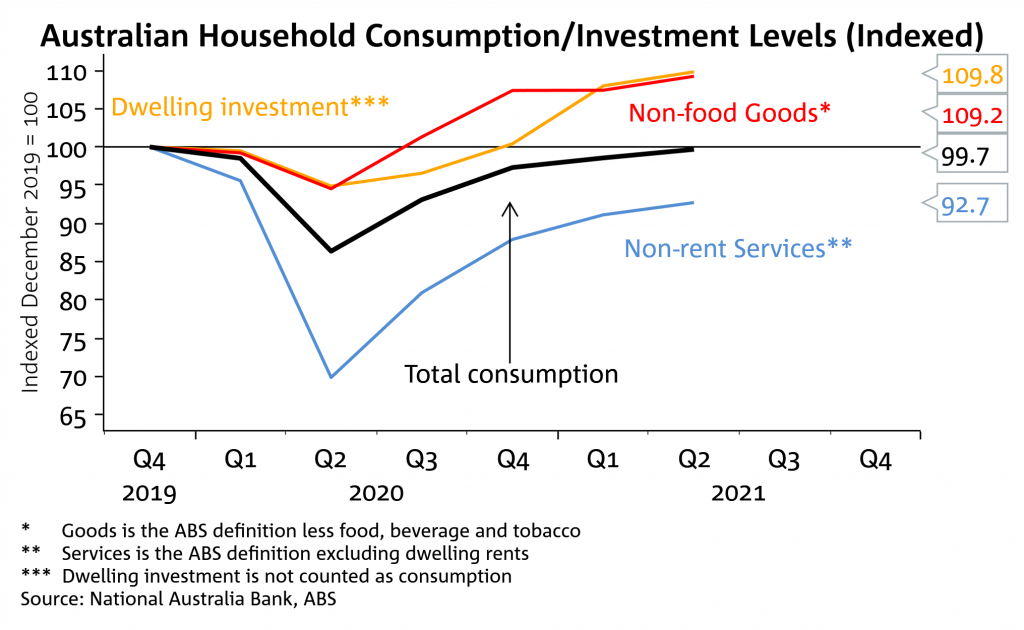

Household consumption is almost back to pre-pandemic levels in Australia with Q2 GDP figures showing consumption is now just 0.3% below pre-pandemic December 2019 levels.

Analysis: What happens to consumption as we learn to live with the virus?

Household consumption is almost back to pre-pandemic levels in Australia with Q2 GDP figures showing consumption is now just 0.3% below pre-pandemic December 2019 levels. On the investment side, household dwelling investment passed its pre pandemic levels in Q4 2020 and is currently 9.8% above pre-pandemic.

Non-food goods consumption has done most of the heavy lifting and is currently 9.2% above pre-pandemic levels, while non-rent services consumption is still recovering and is some 7.3% below pre-pandemic levels. Note non-food goods consumption comprises around 25% of household consumption, non-rent services 40%, while dwelling rents and other services are around 21% and food and beverage 13%.

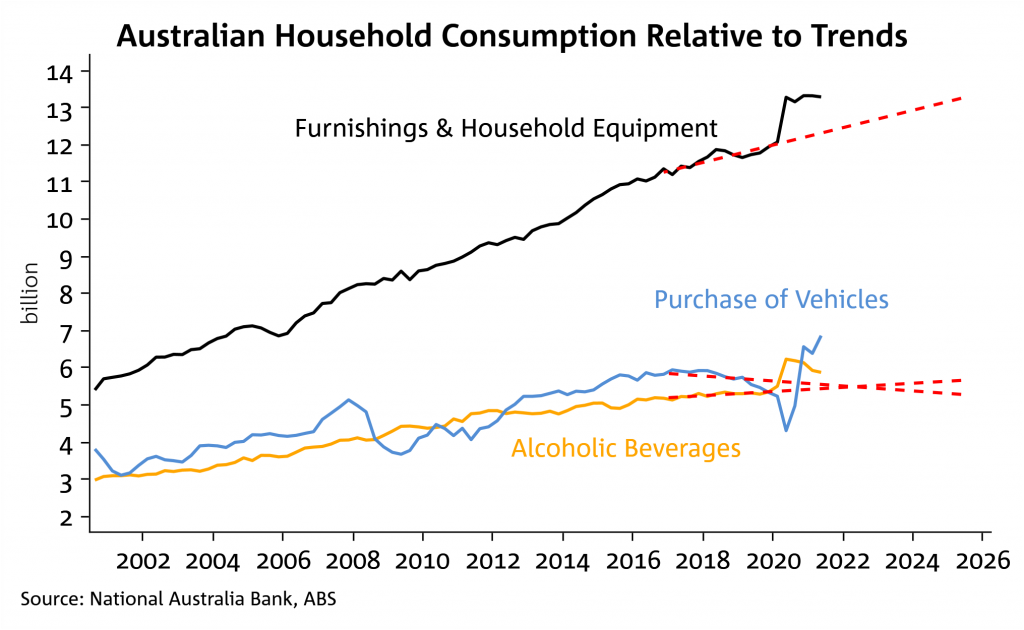

Some normalisation in goods demand (and in dwelling investment) is likely given how far above pre-pandemic levels they are. In this Weekly we estimate how much pull-forward and satiation of pent-up demand has occurred to give some indication of what 2022 may look like as consumers continue their pivot back towards services. We run simple linear trends from 2016 to 2019 and calculate the cumulative difference.

We find on the goods side the three categories that have seen the largest cumulative divergence to pre-pandemic trends are ‘alcoholic beverages’, ‘furnishings and household equipment’ and ‘purchase of vehicles’. Each of these categories is running 0.3-0.6 quarters ahead of pre-pandemic trends and indicative of a degree of pull forward of consumption. We would expect some reversal of these gains.

Interestingly there are also some goods categories where underspending has occurred. This is most prevalent in ‘clothing and footwear’ which is 0.5 quarters behind pre-pandemic trends. As people start to interact in person more fully again, it is likely some of this underspending will be made up and indeed that is what appeared to be occurring in Q2 2021 just prior to recent lockdowns.

On the services side, the largest underspending relative to pre-pandemic is in ‘transport services’, ‘hotels cafes and restaurants’, ‘recreation and culture’, and health. The implications of this underspending though are less clear given the adage “you can’t consume more than one haircut at a time”. So while some sectors may see a concentration of pent-up demand, such as for holiday and recreation as lockdowns ease and as border restrictions start to ease, others are more likely to revert to previous levels with little sustained overshoot.

Australia’s transition to starting to live with the virus is of course key to all these trends, particularly regarding services. NSW (and now VIC) have indicated that they will gradually ease restrictions once full adult vaccination reaches 70%. NSW has nominated mid-October for when restrictions will be eased and given high re-opening hurdles we think people will be willing to resume activity once restrictions ease.

Chart 1: Pivot to services underway and will likely build steam in 2022. What happens to elevated goods consumption and dwelling investment?

Chart 2: Pull-forward of consumption most evident in furnishings & household equipment, motor vehicles, and alcoholic beverages

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.