Analysis: RBA Review? What it may recommend given Fed, ECB and RBNZ reviews

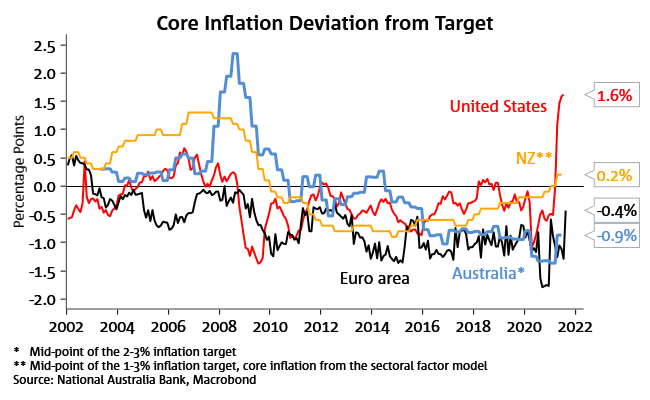

A review into the RBA gained significant momentum last week after the OECD stated “now would seem like an appropriate time for a review of Australia’s monetary policy framework” and that a review should be “…broad in scope, potentially including a review of the central bank mandate, policy tools, methods of public communication, hiring processes and structures”(see OECD: Economic Surveys Australia 2021 ). The OECD’s framing is about taking stock after the pandemic given changes in the economy and the use of unconventional policies, though the call comes in the context of a prolonged period of undershooting the inflation target since 2014.

The Federal Treasurer surprised last week by saying he is open to a review (as is the Labor opposition), but that if a review were to take place it would be after the next federal election which can be called anytime between now and May 2022 (see AFR: Strong support for independent RBA review for details). There is thus a possibility that a review into the RBA occurs from H2 2022, with potentially important implications around the RBA’s mandate, how the RBA interprets its mandate and board composition and transparency. It is unclear whether the review would be backward, or more forward looking given the aftermath of the pandemic.

In this weekly we look at the recent reviews done at the Fed and the RBNZ to glean what a review into the RBA may recommend. We assume a broad ranging review into the monetary policy framework. Our conclusion is that the RBA has already tweaked its approach since the beginning of the pandemic, wanting to see actual, rather than forecast, inflation sustainably higher before raising rates in order to achieve maximum sustainable employment. A review could also look into the board composition and transparency with this intersecting with the Treasurer given he appoints members.

As for recent reviews of the US Fed, ECB and RBNZ, they differ widely in terms of how they were conducted. The US Fed (2020) and ECB (2020) reviews were led internally with public consultation. The results of the US Fed review ushered in Average Inflation Targeting and a renewed emphasis on maximum employment. The ECB strategy review adopted a symmetric inflation target of 2% (instead of the formal 2% ceiling that had existed) (see Powell for US Fed Review and ECB for their Strategy Review).

The RBNZ Review in 2017 in contrast was more comprehensive and far ranging including:

(i) amending the objective of monetary policy to require the RBNZ to consider maximum sustainable employment alongside price stability when making decisions on monetary policy;

(ii) establishing a monetary policy committee which includes external representation; and

(iii) adding greater transparency with a formal remit, charter and code of conduct (see NZ Treasury for details).