NAB recently published its Australian Residential Property Survey where we re-affirmed our forecasts for house prices to decline by 10% by the end of 2023. This is in line with our outlook for interest rates where we see the RBA cash rate getting to 1% by year’s end and to 2.25% by end-2024. Markets of course are pricing a much more aggressive hike cycle with cash at around 2¼% by end 2022 and peaking at 3½% by August 2023.

In this Weekly we look at the potential impacts on theoretical borrowing capacity at different interest rates using a simple credit foncier model (principal/interest with constant total monthly repayments). The main conclusion is that theoretical borrowing capacity naturally falls with higher rates. Note a fall in borrowing capacity is unlikely to be fully reflected in dwelling prices given strong household balance sheets.

We model the credit foncier framework using average weekly earnings. We assume maximum annual repayment capacity at 30% of pre-tax income. We also use a variety of interest rate assumptions including NAB’s cash rate forecasts, market cash rate pricing, and the current 3yr fixed rate which has moved higher in line with 3yr swap rates. We assume average weekly earnings grow by around 3-3½% a year. We also incorporate APRA’s serviceability buffers as published by APRA, available since 2019.

Our main finding is under NAB’s cash rate assumption and assuming pass through to mortgage rates, theoretical borrowing power falls by around 13% by the end-2024, which is broadly consistent with NAB’s 10% fall in dwelling prices by the end of 2023. Note in our analysis we do not consider any changes in the spread between mortgage rates and cash rates, nor do we consider any potential macro-prudential changes.

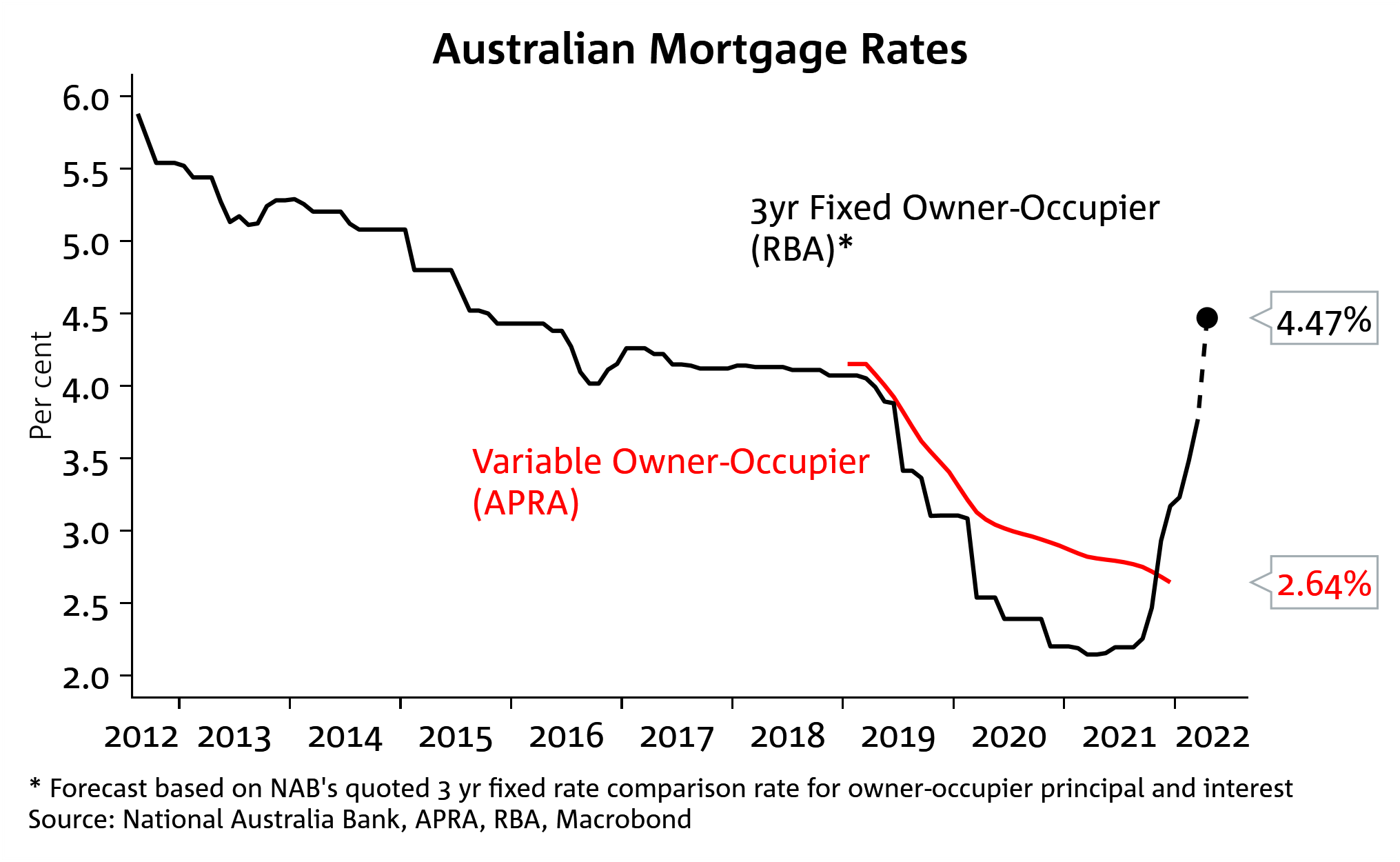

A steeper fall in borrowing capacity occurs using the 3yr fixed rate with a fall in borrowing capacity of around 22% on our estimate of the 3yr fixed rate for April. Note the 3yr fixed mortgage rate closely tracks the 3yr swap rate. In contrast, variable rates have not risen, and there has been a shift back to variable rates from new borrowers – as at Feb 2022 the fixed rate share had fallen to 28% from a peak of 46% in Aug 2021.

An even steeper fall in borrowing capacity would occur under market pricing given markets price the cash rate peaking at around 3½% by Aug 2023. Such a rate would imply a fall in borrowing capacity by around 24%. Combined with our prior Weekly on household interest payments, we still see market pricing as too aggressive in the near-term, unless there is a substantial acceleration in wages growth.

Our analysis reaffirms our view that we should expect moderate house price falls as rates start to rise. We are already starting to see very slight falls in Sydney and Melbourne, and we expect this to translate to other capital cities by the end of 2022. By the end of 2023 we see house prices broadly lower by 10%, only partly reversing the 25% rise seen during the pandemic.

With household balance sheets relatively strong, we see households being able to adapt to a higher rate environment. The analysis though does highlight the potential sensitivity of new lending to a higher interest rate path.

Chart 1: Fixed mortgage rates have been increasing

Chart 2: Market path for the RBA cash rate would imply a significantly higher mortgage rate if passed onto borrowers

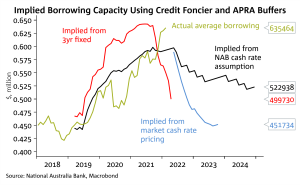

Chart 3: Implied borrowing capacity falls with higher rates