We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

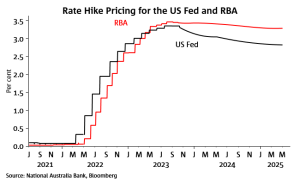

The RBA Board meets tomorrow in a meeting now widely expected to see the first increase in interest rates since November 2010.

Read our NAB Markets Research disclaimer

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

Economic and financial market update

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.