On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

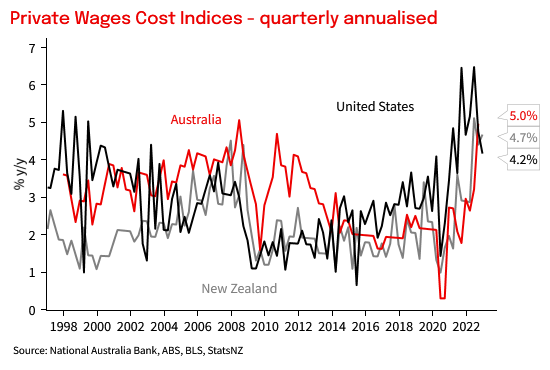

Yesterday's Minutes make clear the RBA’s priority is inflation. While the Board is seeking to return inflation to target while keeping the economy on an ‘even keel’ it will do what is necessary to return inflation to target. The wages backdrop is a key risk.

Chart 1: AU wages growth has caught up to others

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

On a seasonally adjusted basis, the NAB Online Retail Sales Index recorded a drop in growth in July

Insight

Firmer consumer and steady outlook

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.