AMW – Deep Dive – Examining progress rebalancing demand and supply in Australia

The Markets Economics team looks at the progress rebalancing supply and demand in Australia and find that Australia is likely to lag the progress being made in the US on rents, energy and wages/services.

Australian Markets Weekly Deep Dive – Examining progress rebalancing demand and supply in Australia

It’s a different Australian Markets Weekly this week, where we take a Deep Dive into the progress made in rebalancing demand and supply imbalances in an Australian context in the form of a chart pack (see link above).

Australia, like many advanced economies, suffered five large, overlapping shocks over the past three years, each with complex economic impacts and a major associated inflation shock. In rough sequential order, these were:

A big lift in goods demand when production was hampered due to movement restrictions, and while consumption of services was restricted by lockdowns/border closures. This was evident in supply chains, freight rates and goods price inflation. This shock is clearly in remission, though backlogs in some sectors (e.g. tractors) remain.

A sharp recovery in services demand once restrictions eased. The recovery occurred at a time when the international border was still closed, impeding the ability of capacity (often labour) to respond. Prior decisions by firms to reduce capacity at the height of the pandemic also impacted the ability to ramp up supply (e.g. airlines).

The above two shocks saw a very significant acceleration in demand for labour relative to supply, reflected in low unemployment, elevated job vacancies and stronger wages growth. Strong demand was a common thread, while reduced migration was a significant part of this in Australia – in some other countries, it was reduced participation.

In housing, a significant jump in demand due to low interest rates and preference change for additional space (in part due to lockdowns) combined with interstate migration restrictions has resulted in very low vacancy rates and low levels of housing stock on the market. These factors are currently exacerbated by pent-up migration demand.

A significant global energy and food supply shock in early 2022 after Russia invaded Ukraine. This saw spikes in energy and food prices. While much of this shock has reversed, Australia will feel higher energy prices in 2023 due to lags in regulated energy prices.

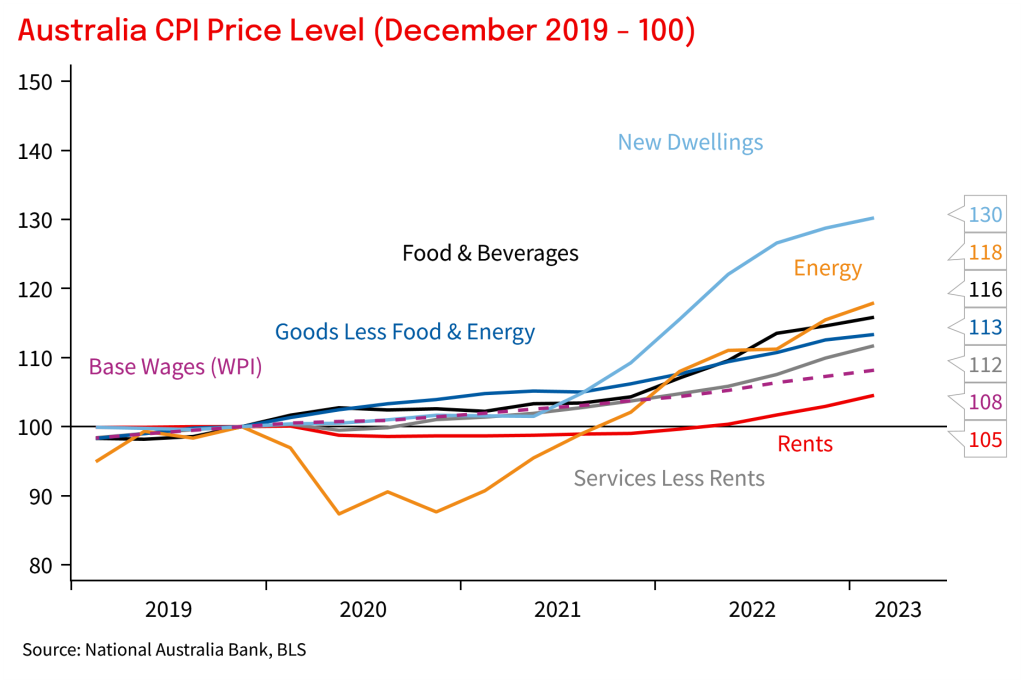

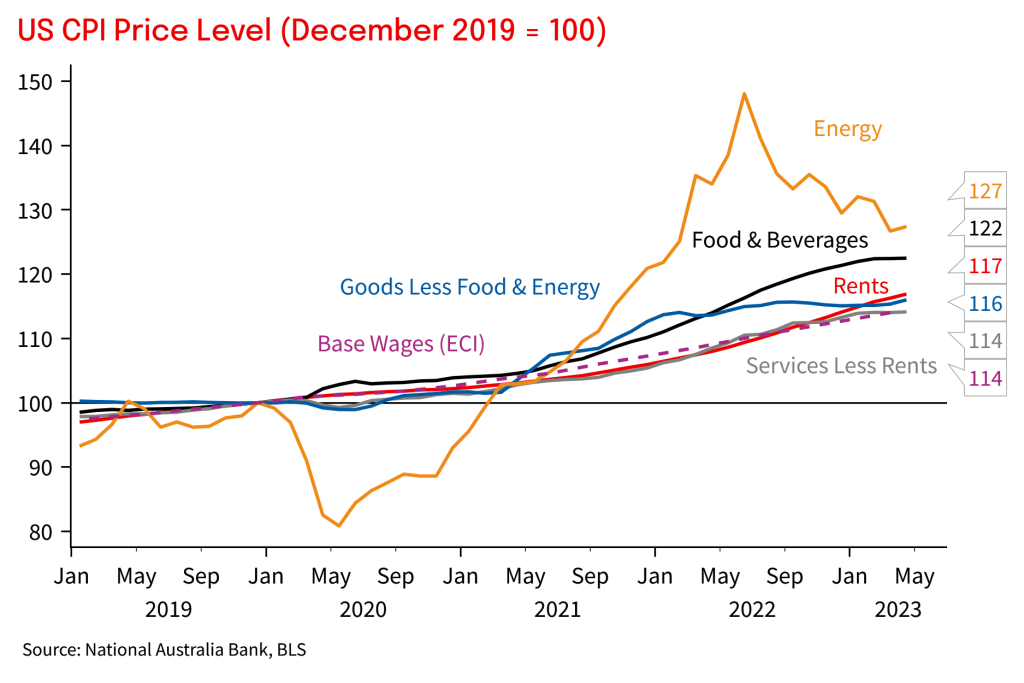

We can see the sequence of these shocks first impacting prices in goods and housing construction markets, then labour markets, then services markets and finally energy and food markets. This is a slightly different sequence than in the US.

Chart 1:

In examining the progress of demand and supply rebalancing in Australia, we’d make the following important points:

Rebalancing of demand and supply is clearly underway in many markets as higher interest rates and in some cases previously pulled forward demand begin to impact the demand side.

Importantly the supply side is also adjusting. The process is most advanced in goods markets globally (industrial production is 2% above pre-pandemic), but less advanced in services so far.

Australia’s labour market remains tight, but it is loosening with migration having picked up. It is clear migration will loosen up the labour market, but with vacancies still high it is likely to take a few more quarters.

While income growth is set to slow, a key uncertainty is the extent to which Australian households are willing to run-down accumulated ‘excess’ savings during the pandemic.

The slow rebalancing in labour markets to date, is sustaining overall consumer demand, causing central banks to worry about services inflation pressures remaining elevated.

This concern is compounded in Australia by the lagged response of wages (and also of rents and energy prices), meaning the RBA likely has a little more work to do to ensure inflation returns to 3% by mid 2025, the target it has set itself.

Housing markets are mixed. In Australia, the additional demand for space stemming from the pandemic persists, but migration and higher rents will likely see household size rise.

We’ll continue to monitor developments in US indicators and US inflation closely as a long lead on how inflation will ultimately develop in Australia as the US does seem to be around 6 or so months ahead of Australian inflation developments in this cycle. There are encouraging signs in some of these components in the US CPI, with many components close to flat in recent months (goods excluding food and energy), energy prices falling and signs that asking rents are moderating, which should show up in lower increases in the large Owner Equivalent Rents component of the CPI.