Analysis: Headline CPI of 7% over 2022 looks reasonable

The RBA has upgraded its inflation forecasts, now seeing headline inflation at 7% by the end of 2022. The upgrade was on the back of higher fuel and energy inflation and along with the low level of rates was a key factor in the decision to move by 50bp in June. It’s clear that the RBA’s willingness to look through supply-side inflation is limited in an environment of tight labour markets and a strong demand back drop.

Central banks had previously been comfortable setting policy on the strongly held expectation that an easing of supply side drivers would attenuate the task at hand of moderating nominal demand. The clear message from the Federal Reserve is that restoring price stability is non-negotiable.

The recent drivers of the sharp lift in inflation have been unusual. Strong demand is a factor, but two waves of supply shocks, the pandemic and the more recent energy and food price shock, have combined to create an environment that is much more inflationary than the strength of demand alone would imply.

In this Weekly, we take a bottom-up view of the inflation outlook over the remainder of this year as a complement to aggregate model-based forecasts. Our analysis suggests the RBA’s nominated peak of 7% y/y in Q4 is reasonable.

The current major drivers of higher inflation in Australia and globally would be an unlikely source of a sustainable lift in inflation but are still likely to keep pressure on inflation in the near term. The peculiar inflationary environment of the past 18 months can be described by 5 main themes:

High goods spending into constrained supply.

Increased demand for residential space/property.

Frictional reopening pressure as pent-up demand faced into reopening frictions and ongoing pandemic impacts across service and travel industries.

Most recently, additional large energy and food price shocks emanating from Russia/Ukraine.

Reduced labour supply & tight labour markets.

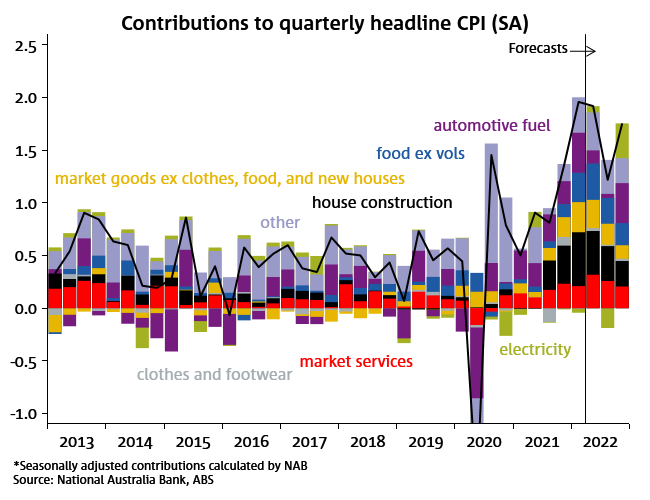

The NAB Survey continues to point to very elevated inflation pressures. We expect goods price inflation to remain elevated in Q2 and ease back gradually through the course of the year amid renewed pressure from energy and fuel. Wholesale energy costs will flow through to retail prices with a lag, and rebate schemes in WA and Queensland are likely to offset the round of price increases in Q3. Combined with the end of the temporary fuel excise cut, that sets up a blockbuster Q4 quarterly CPI print.

We will publish a full Q2 CPI preview in the coming weeks ahead of the 27 July release. These preliminary estimates point to a 1.8% q/q for headline and 1.4% q/q for trimmed mean.

A major global investment fund is using NAB’s financial innovation for derivative portfolios to help incentivise sustainability goals in a new deal for the Australian market.