AMW: How big will the RBA’s QE program have to be?

The RBA is widely expected to ease policy further in November by cutting the cash rate to 0.10%, along with the 3-year yield target (YCC) and the TFF rate.

We expect the RBA to announce QE purchases in the 5-10 year area of the curve.

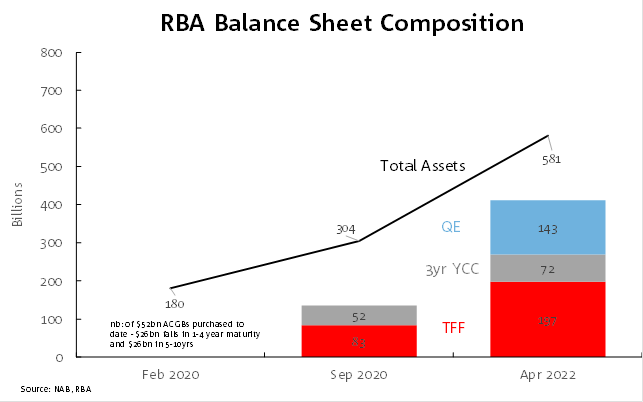

While there remains uncertainty over what will be announced in regards to QE, our analysis published in a cross-market note on Friday suggests the RBA would need a QE program of $143bn in order to return to full employment and inflation to target (the total balance sheet expansion would be $277bn when incorporating the TFF expected $114bn drawdown and $20bn in purchases for keeping yields at the 3yr YCC target).

In estimating the size of a potential QE program we used three approaches:

Using the RBA’s MARTIN macroeconomic model and international comparisons, NAB estimates that the RBA will have to expand its balance sheet by 14% of GDP (or $277bn) to achieve its target of full employment and target inflation. Taking into account TFF expansion and YCC purchases gives a QE program of $143bn.

Looking at the relative balance sheet expansion of central banks since the start of the COVID-19 pandemic. To match the increase in balance sheets since the pandemic would require an expansion of $275bn, and to match the total overall balance sheet size requires $491bn. Taking into account TFF/YCC, suggests QE of $141bn-357bn.

Looking at bond buying programs by the Fed, BoC and RBNZ, which suggests the RBA would need to get overall holdings at or above 30% of outstandings.

Week ahead

Australia: CPI is on Wednesday and while historically this has been the most market sensitive piece of data for Australian markets, is unlikely to be this time given the RBA’s explicit forward guidance. NAB forecasts Headline CPI will rise a sharp 1.9% q/q, reversing last quarter’s 1.9% fall, due to the expiry of pandemic-related government subsides, as well as petrol prices. Annual Headline CPI though will remain subdued at 1.0% y/y. Trimmed Mean (core) is expected to rebound 0.6% q/q and 1.4% y/y.

International: NZ: ANZ Business Survey is Thursday. US: Now just eight more days to the Presidential election where Biden continues to lead. Markets are focused on the chances of the Democrats gaining a Senate majority and the implications for spending, inflation and yields. As for data, Q3 GDP is on Thursday and the Atlanta Fed’s GDP Now is pointing to growth of 35.3% annualised (equivalent to 7.9% q/q), partially reversing last quarter’s -31.4% contraction. EU/UK: ECB meets Thursday and while no change is expected a steer to more QE in December is possible. The Euro Area also has Q3 GDP figures, with consensus at 9.4% q/q from -11.8% in Q2. UK-EU trade negotiations also continue, although a deal may not be forthcoming until November.

Please see attached for further details

Charts of the week:

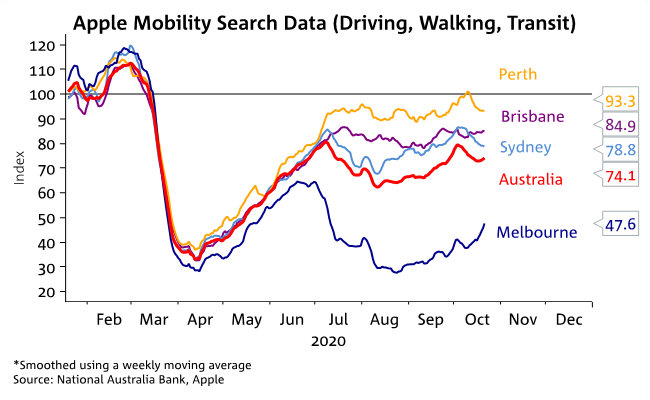

Chart 1: Melbourne mobility bouncing back

Chart 2: RBA’s balance sheet set to expand under QE

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.