We noted in a prior Weekly that one consequence of the RBA pursuing ‘maximum sustainable employment’ was that macro-prudential policies may have to be utilised more to control financial stability risks, including in the housing market. Recent comments by APRA and the RBA suggest house price dynamics are not yet overly concerning, that house prices are not the responsibility of either body and that lending standards are not deteriorating.

Overall, regulators appear not to be pushing to tighten macro-prudential rules on house price rises alone. APRA Chair Byres emphasised that “we have no mandate to target the level of housing prices, or act to improve housing affordability. For us, housing prices are a risk factor, not a goal”. Similar comments have been echoed by RBA Governor Lowe. NAB’s analysis of house prices suggest they are broadly consistent with the low interest rate environment with a credit foncier model suggesting theoretical purchasing power has increased by up to 21% since mid-2019.

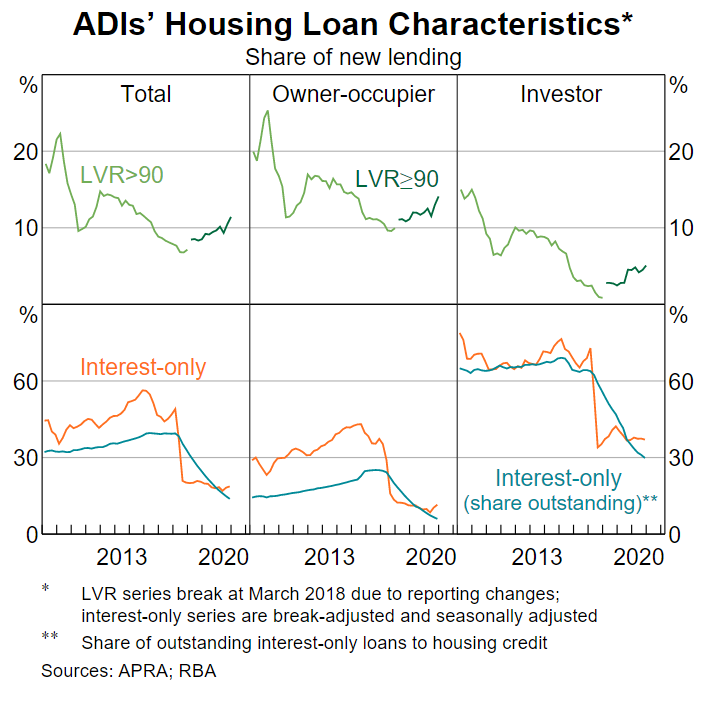

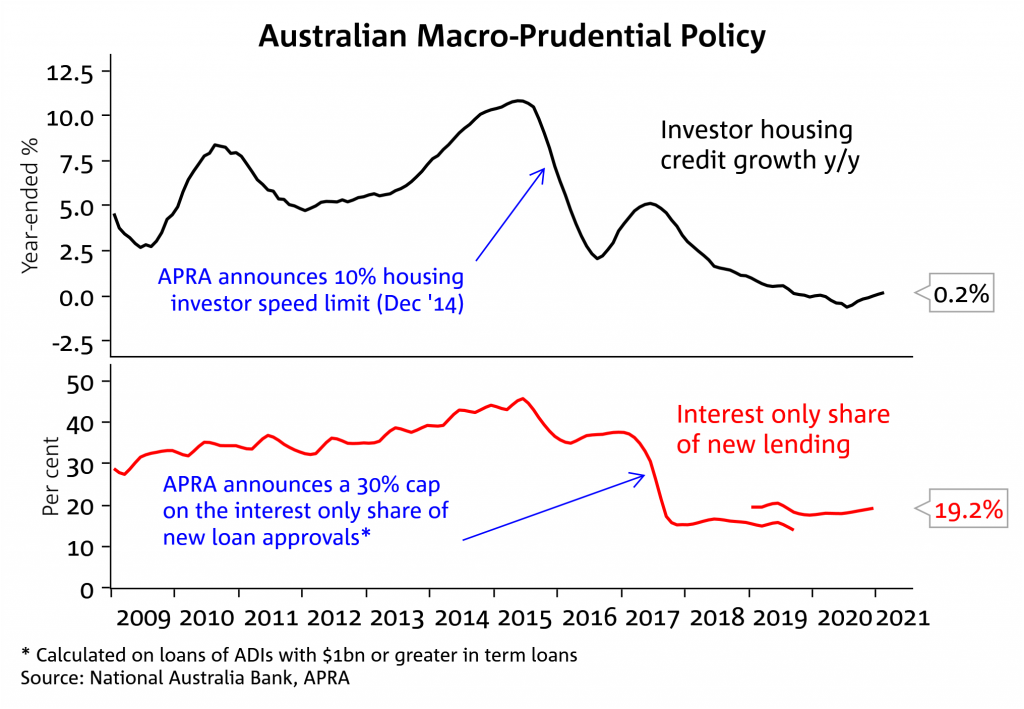

Instead, regulators are watching lending standards. Here APRA notes “at an aggregate level, lending statistics do not show major signs of a return to higher risk lending”, with the RBA agreeing in its recent bi-annual FSR . Importantly investor lending and interest only lending remains well below the levels that previously drove macro-prudential changes in 2014. A recent tick up in higher LVR loans is being attributed to higher LVR first home buyers being drawn into the market due to government incentives. Such pull-forward is likely to reverse once incentives end. Regulators will keep watching to ensure lending standards are maintained.

We conclude that a tightening in macro-prudential rules is unlikely in the near term. Where we are in the cycle also matters with the RBA unlikely to want to hamper the housing transmission channel of monetary policy until the Bank is more confident in achieving full employment and at target inflation. In H2 2021, when the RBA is more confident in the recovery, it is possible regulators may feel more compelled to act if very strong house price growth continues, taking that as a sign of increased risk taking and borrowers being too optimistic, as hinted at in the recent RBA FSR. For this reason investor mortgage approvals and credit growth will be watched closely.

The week ahead

Australia: Aussie jobs data for March on Thursday is the key event for Australia with NAB seeing upside risks to the consensus and pencilling in jobs growth of +55k (consensus 35k) and for the unemployment rate to decline two-tenths to 5.6% from 5.8% (consensus 5.7%). Also out in the week is the NAB Business Survey on Tuesday (no hints here) and the W-MI measure of Consumer Confidence on Wednesday.

International: Offshore the focus is on the US, China, and the Q1 earnings season; the RBNZ also meets but no change to rates or guidance is expected at this ‘interim meeting’. US: March CPI is on Tuesday and will be watched closely for any signs of inflationary pressures, retail sales the data event to watch. CH: Aggregate Financing due anytime in the week and Q1 GDP on Friday. UK: Monthly GDP on Tuesday.

Chart 1: Lending standards are being maintained, lessening the risk of a near-term tightening in macro-prudential rules

Chart 2: Recent outcomes are still better than prior prudential benchmarks that were implemented in 2014 and 2017 (note these benchmarks formally ended in 2018)

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.