Total spending grew 0.9% in June.

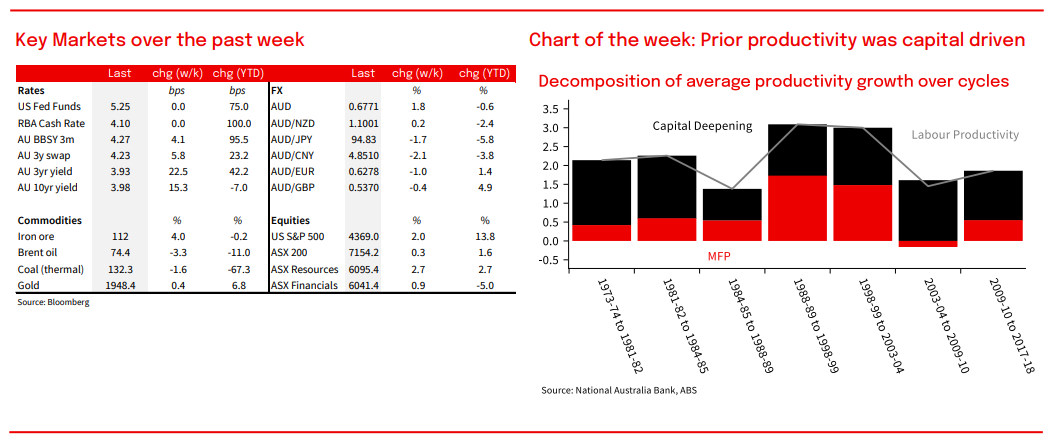

In today’s Weekly, we delve into Australia’s productivity and labour cost data given the RBA’s recent focus on these metrics, and explain why timely signals on the inflation outlook may be better found elsewhere.

For the full report, see attached.

Total spending grew 0.9% in June.

NAB client Zenith Energy’s innovation is helping decarbonise the mining sector through providing efficient hybrid generation solutions in remote areas.

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.