Long-term signal vs. Short-term noise

Insight

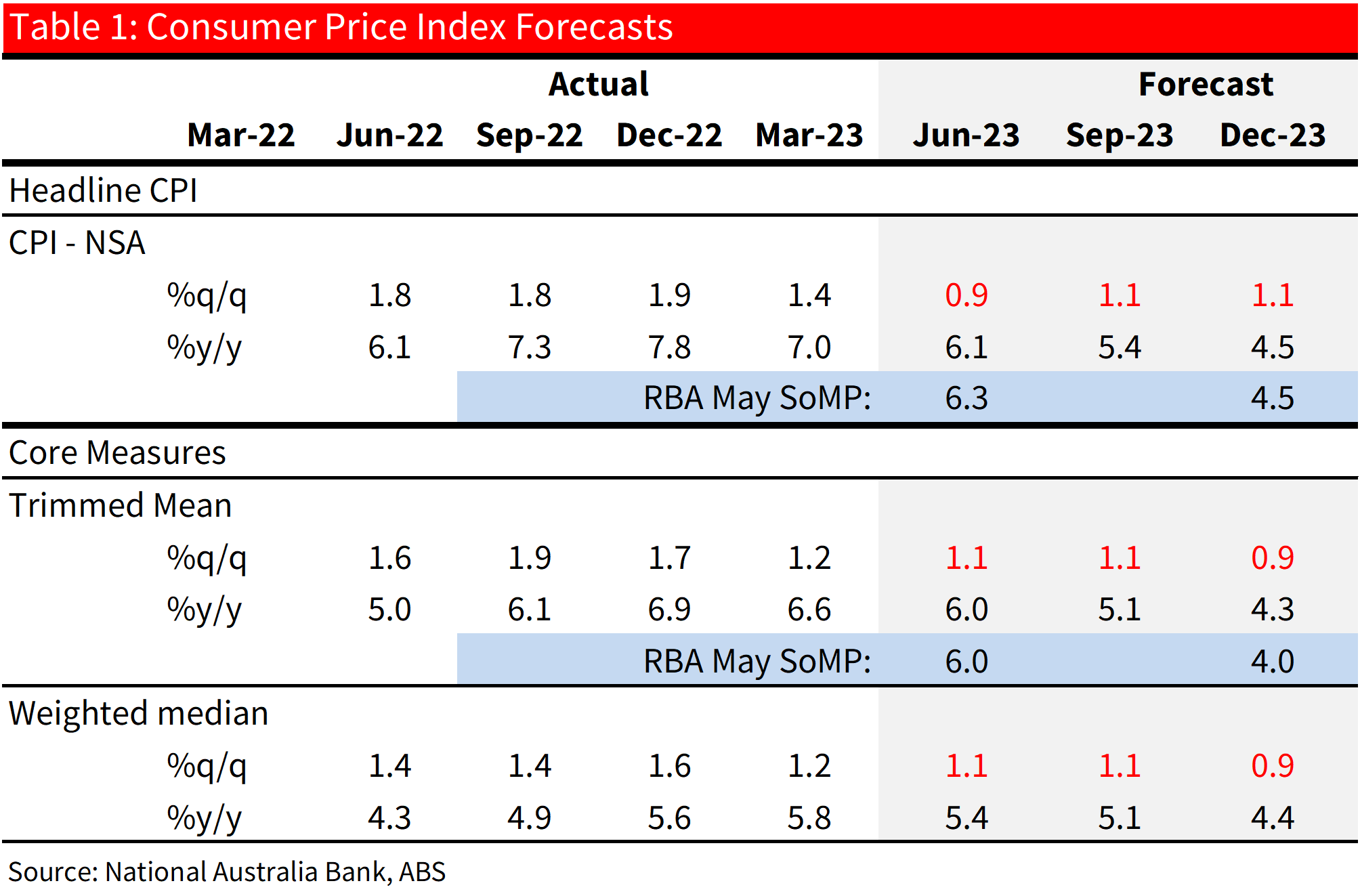

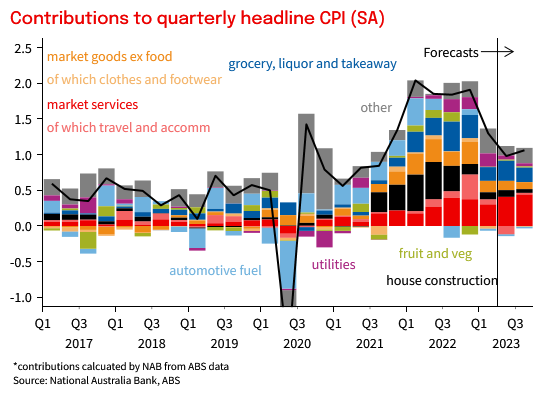

We expect Q2 CPI next Wednesday (26 July) to show little sequential progress reducing underlying inflation even as y/y rates move lower

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets. Read our NAB Markets Research disclaimer.

Long-term signal vs. Short-term noise

Insight

Welcome to NAB’s newsletter on the Sustainable Finance market from an Australasian perspective.

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.