Q2 CPI is just under four weeks away (on Wednesday July 28). In this week’s Weekly we have a first look at what CPI may print and highlight why we believe Core CPI is likely to remain subdued despite the pick-up seen in core inflation in the US, NZ and Canada.

Q2 CPI is just under four weeks away (on Wednesday July 28). In this week’s Weekly we have a first look at what CPI may print and highlight why we believe Core CPI is likely to remain subdued despite the pick-up seen in core inflation in the US, NZ and Canada. Subdued core inflation also means the RBA will lag the Fed, RBNZ and BoC in rates normalisation when it comes.

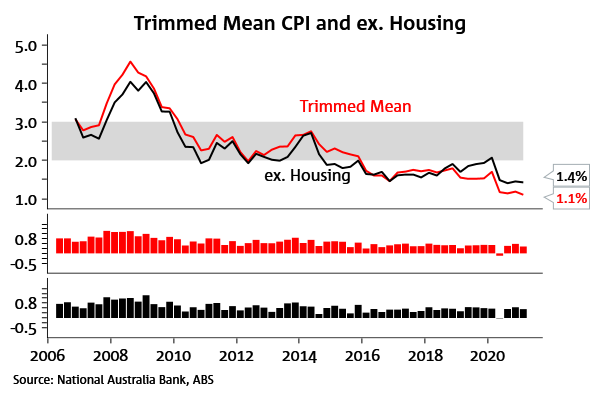

For Q2, our first look at Headline CPI is for a print at 0.7% q/q with Trimmed Mean edging higher to 0.4% q/q. Base effects will push annual Headline CPI to around 3¾% y/y in Q2 from 1.1% in Q1. The base effect on Trimmed Mean CPI is much smaller resulting in 1½% y/y from 1.1%. Even with base effects, underlying inflation in Australia is expected to be subdued. Note this preliminary forecast will be firmed up in a full CPI preview.

Why is underlying inflation so subdued in Australia when it is has picked up to at or above target in the US, NZ, Canada and the UK? The Australian CPI by construction is not subject to some of the factors that have recently pushed up monthly US inflation – namely used car sales between households are not included in the Australian CPI, whereas in the US used car prices have added 0.8 percentage points to inflation.

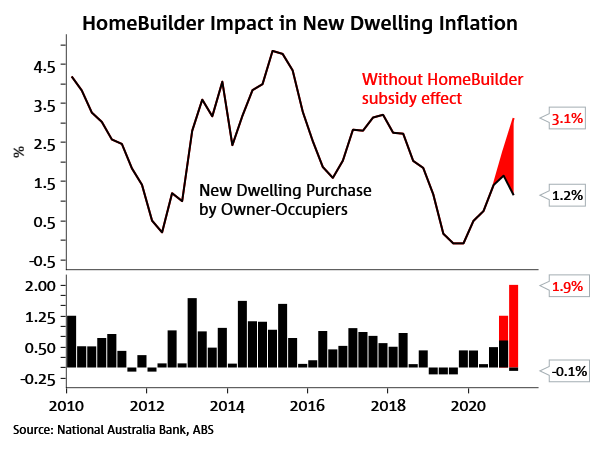

Government policies enacted in reaction to the pandemic have also been a factor in Australia, particularly for rents and purchase of new dwellings which together account for over 15% of the CPI basket (the government’s half price airfares scheme in Q2 is also another example). Rents have been subdued given the pandemic and the closed international border is also weighing on inner city apartment rents in Melbourne and Sydney. Government stimulus such as the HomeBuilder subsidy and other state-based grants are recorded as an effective price decline for households and the timing of payments means the subsidy is still likely to continue to weigh despite the scheme ending in early March – payments under HomeBuilder are made when construction starts with start requirements recently extended to September 2022. To illustrate how important rents and new dwelling costs are, we construct an inflation measure excluding housing, which shows underlying year-ended CPI runs around three-tenths higher.

Chart 1: Housing contribution to CPI has declined

Chart 2: HomeBuilder has mostly offset cost increases in New Dwelling Purchases

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.