Coming in for landing in a heavy cross wind

Insight

Corporates will need to be nimble and be ready to access issuance windows at short notice in 2019.

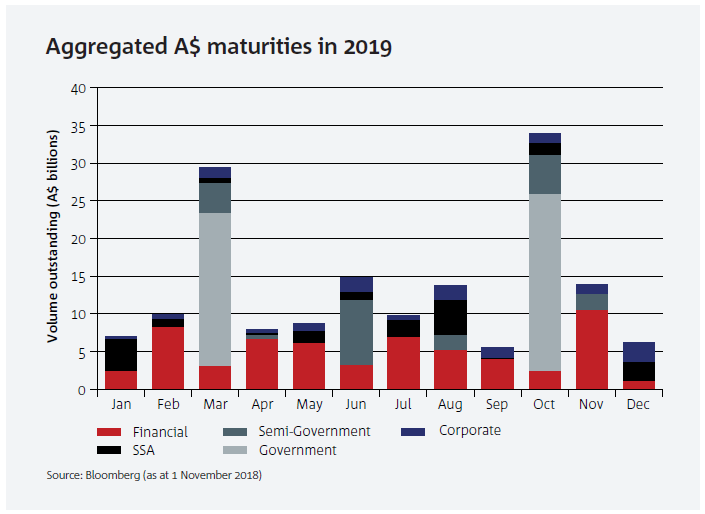

Australian high grade and credit markets have much to look forward to in 2019. We have been disturbed in 2018 by bouts of volatility that temporarily closed down activity. By the end of June, volumes were down about 25% year-on-year. However, the Australian new issue market roared back from mid-July and by the end of October was only about 7% below last year’s volume. Steady redemptions into year-end may not be converted to material issuance volume. However, the steady amounts of cash re-entering the system will leave the market technically short in the coming months. Next year, AUD bond maturities are better spread across the months further assisting the process. Unless macro factors complicate the picture – and the risk of this is now elevated — we see the Australian credit markets biased slightly tighter in 2019.

After the record supply in the A$ corporate bond market in 2017, 2018 has seen a lower level of supply closer to mean averages, and 2019 should be similar if volatility persists next year.

It has been a year of transition for the A$ corporate market, where issuance was ‘barbelled’ between the positive start to Q1, a slow Q2, and the rebound in Q3. While the record A$20 billion printed in 2017 was always going to be a hard act to follow, the return of rate and geopolitical volatility fostered a defensive investor mindset. The volatility tempered issuance from local and Kangaroo corporates. Softening A$ investor appetite for tenor combined with a mid-year widening of spreads led to many corporates accessing the USPP or bank loan markets. The sharp rebound in corporate bond supply in Q3 from various sectors (A$8.5 billion) nevertheless served as a reminder of the latent potential investor demand for A$ credit when markets are conducive. This bodes well for 2019 and beyond.

Looking ahead to 2019, we expect the following trends to emerge for domestic corporate MTN issuers:

• Market rotation: NAB expects the A$MTN space to benefit from some debt capital market rotation in 2019, implying activity levels may be more steady, subject to local markets being cost and tenor competitive versus alternatives;

• Nimble issuer mindset: Should volatility persist and mindful of next year’s Australian Federal election, corporates will need to be nimble and be ready to access issuance windows at short notice, and avoid planning deals close to such events.

• Asian investor marketing remains important: Asian based investment into the A$ bond market has been one of the biggest defining changes in the past decade. At a time when global rates are rising and local yields are not, issuers should nonetheless step-up marketing efforts to consolidate investor demand from Asia as well as domestically.

The 2018-19 Semi Government budgets estimated a total issuance requirement of around A$30 billion for the year of which A$7.8 billion was new funding. Whilst the expected requirement was similar to the issuance volumes of 2017-18, for many issuers it was lower than expected based on previous updates to the market. Balance sheet management strategies, asset sales, delays to infrastructure spending and improved operating positions have all helped lower requirements across the respective issuers.

By the end of October, and buoyed by high amounts of investor liquidity, the sector has been very active, with a number of issuers already well progressed through their FY18-19 funding requirements.

Looking ahead, we expect issuance to continue at a steady rate as the sector works through its requirement. What’s interesting to note is the material lift in supply that is anticipated for fiscal 2019-2020. Gross issuance is projected to rise to as much as A$51 billion in that financial year with approximately A$18 billion of this to be net new issuance. Therefore, we expect no letup in supply over the near-term.

This uplift in issuance comes at a time where Australian Commonwealth Government issuance is expected to decrease, which should ensure an interesting spread dynamic between the high grade sectors over the near term. Compression between the AA and AAA ratings has been a key feature of the market in recent years. Whether we are at an inflection point on this spread will certainly be keenly followed by the market.

Whilst both global and A$ credit markets provided supportive demand dynamics for the vast majority of 2018, Australian financial institutions faced rising cost of funds pressure through a variety of different mechanisms. In the short end money markets, banks have faced a volatile BBSW, elevated repo markets and record high cross-currency basis markets. All of which has resulted in a rising cost of funds environment for domestic lenders. Conversely, the higher cross-currency basis meant the A$ market looked attractive for many Kangaroo issuers and we saw both inaugural and repeat issuers tap the Australian investor base.

Credit spreads on new issues for financials has been remarkably stable over recent months with Major Bank 5-yr issues trading within a 5-10bps range since mid-May. Nonetheless, we do not expect these benign conditions to continue. With economic and geopolitical risks on the rise, there is an expectation that the next 12 months will present more challenging market conditions with issuance windows narrowing and volatility increasing.

Pleasingly, the A$ market has matured substantially over recent years and now offers Financial issuers from Australia and around the world issuance opportunities in a variety of formats, tenors and structures. This will ensure the Australian market remains a core funding tool for global banks and a valuable source of liquidity under all market conditions.

This article was first published in 2019 Outlook Creating Opportunities. Read more articles from the magazine.

Speak to a specialist

Coming in for landing in a heavy cross wind

Insight

Conditions again fell in Q2, but confidence stabilising

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.