We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

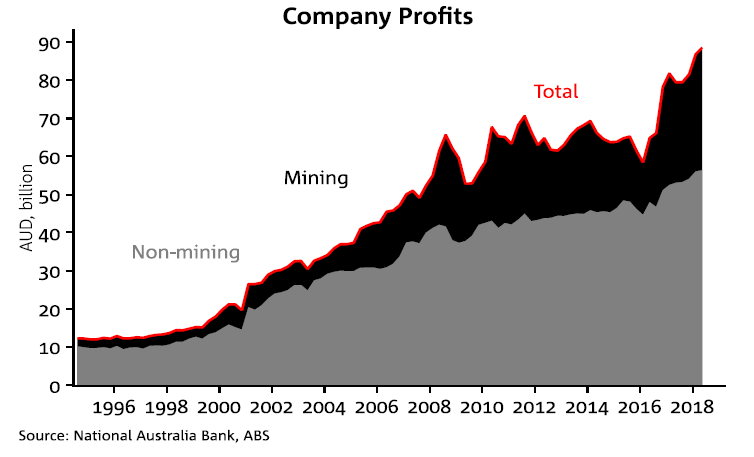

The Weekly delves into trends in profitability following the release of ABS quarterly Business Indicators data,

Chart of the week: Mining profits surge

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

We expect NAB’s Non-rural Commodity Price Index to fall by 4.9% in Q2

Insight

We hear from NAB’s new Chief Economist, as she unpacks the latest economic data with Deb Knight, Host of Money News – 2GB. Watch now.

Video

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.