Change is a constant in our global environment, but that's all the more reason to keep moving forward on your terms.

Article

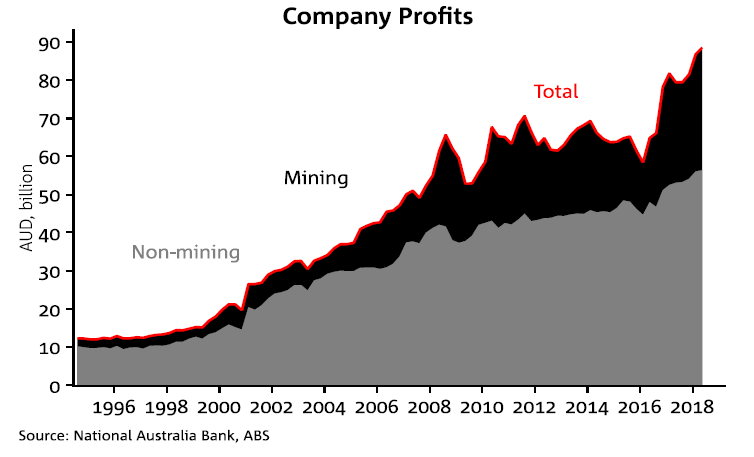

The Weekly delves into trends in profitability following the release of ABS quarterly Business Indicators data,

Chart of the week: Mining profits surge

Customers can receive Australian Markets Weekly and other updates directly in their inbox by emailing nab.markets.research@nab.com.au with the name of their NAB relationship manager.

For further FX, Interest rate and Commodities information visit nab.com.au/nabfinancialmarkets

Change is a constant in our global environment, but that's all the more reason to keep moving forward on your terms.

Article

Protecting your business online is simpler than you think. NAB Executive Business Direct and Small Business, Krissie Jones, shares practical advice on how you can get started.

Newsletter

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.