21 August 2025

Capital Markets

March 31, 2025

Inside the return of corporate hybrid issuance

Hybrid issuance is becoming an ever more relevant funding instrument and capital management tool for corporate issuers today, attracting strong investor demand, write Tabitha Chang and Stefan Visser from the NAB Capital Markets Origination team.

By Corporate and Institutional Banking

The Australian domestic market has seen a strong re-emergence of the corporate hybrid product with A$5.0 billion seen across six issuances in the past six months, Bloomberg industry data shows[i].

The move is adding diversity to the Australian primary and secondary markets, with investor enthusiasm fuelling multi-billion dollar order books and strong over-subscriptions in a number of transactions[ii].

Given this momentum, it is timely to examine the dynamics on both the issuer and investor sides.

Here we unpack the corporate hybrid product and market outlook, some of the reasons behind the resurgence and what rating agencies are looking for.

What is corporate subordinated issuance and what are the key S&P/Moody’s requirements?[iii]

Transactions are customarily structured with consideration to the relevant ratings agency’s defined Hybrid Equity Credit Ratings Methodology[iv]. The aim is to qualify for some level of equity credit on the subordinated note, with most of the recent examples qualifying for 50% equity credit[v]. The key structural elements to consider include:

- Ranking: The subordinated notes constitute direct, unconditional, unsecured, subordinated obligations of the issuer. The level of ascribed equity credit can also be influenced by the notes’ ranking in relation to the issuer’s ordinary equity and, in some scenarios, any preference shares.

- Issuer call option: Typically, a first standard option is at five years post issue date.

- Maturity date of the note: Recent examples have included a maturity at 30 years post issue date, though it’s worth looking at in relation to the equity credit qualification as follows:

- S&P – Intermediate Equity Credit will remain if residual time until the effective maturity exceeds 20 years (if the issuer Interest Coverage Ratio is at BBB- or higher). A subordinated note that qualifies for 50% S&P Equity Credit with a first call date at five years, if not called, could lose its equity credit after five years.

- Moody’s – Equity Credit will remain if there is an initial maturity date of at least 30 years (at issuance) and at least 10 years remaining until maturity.

- Unrestricted Optional Coupon Skip (optional coupon deferral): Subject to dividend stopper and pusher regime deferred coupons are generally cumulative and compounding.

- First margin step-up: To apply at the earliest from the date that is 10 years from the issue date. Additional margin step-up to apply from (and including) the date that is 20 years after the First Optional Redemption Date. Step up must be equal to or less than 100bps to be considered for relevant equity credit qualification.

Why are corporates issuing this product?

Hybrid issuances are becoming a relevant funding instrument and capital management tool for corporate issuers in the domestic market.

Some of the key drivers to consider are:

- In the instances of all the corporate issuers seen in the AMTN market the key rationale has been to lend support to credit ratings. In many cases this is to mitigate pressure on credit metrics from an increase in capex. Owners assess the preference to issue equity credit subordinated notes as opposed to equity injections and/or flexibility on distributions.

- Issuers value and target certain credit ratings for different reasons. These include: access to capital markets; cost of debt; maintenance of an investment grade credit rating; and managing for sufficient headroom to ensure the issuer does not end at the lower end of the investment grade credit rating band.

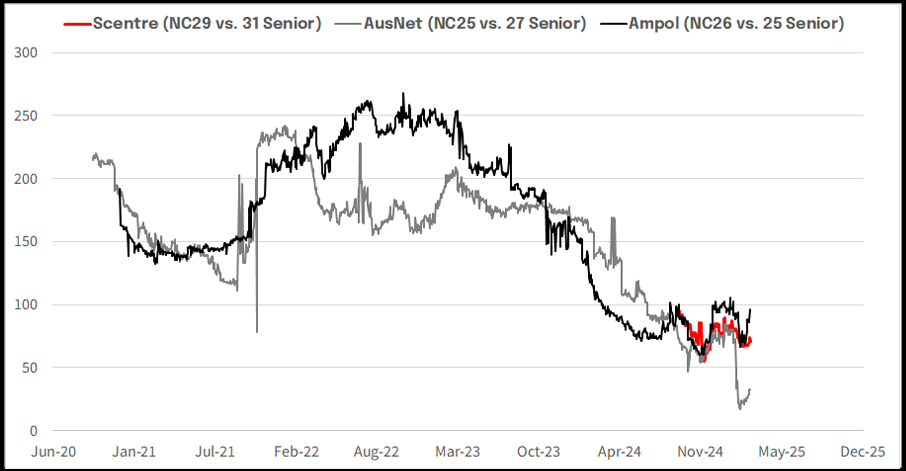

- The senior subordinated spread differential is today at historic tights (see Bloomberg graph below). From levels of about 200bps when Ampol and AusNet issued their subordinated notes in 2020, to below 100bps today, the product has outperformed the rally in senior credit spreads.

Source: Bloomberg, March 2025

Increasing investor demand

We are seeing unprecedented demand from the A$ investor base for this product, given the pick-up in yield over senior paper for strong investment grade issuers. The growth in investor demand has been broad-based across both the Australia and Asia geographies, with a strong Asia bid in order books driving momentum for the trades.

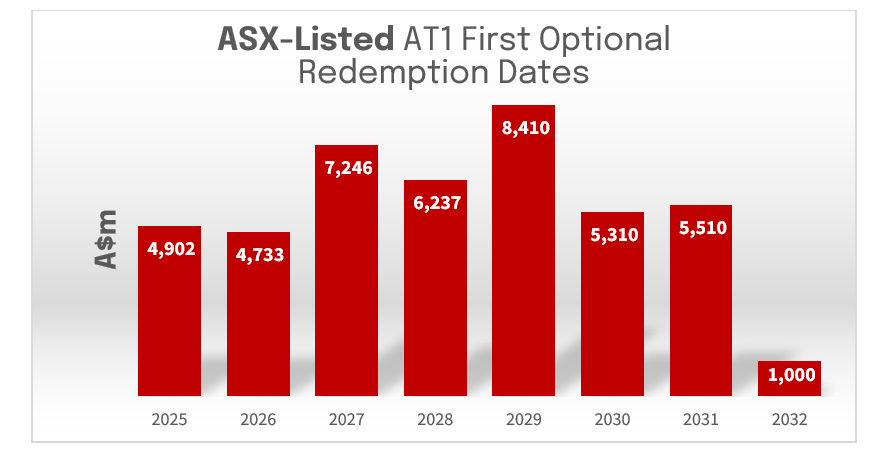

The phasing out of the Additional Tier 1 (AT1) bank debt market (~A$40 billion over time, see graph below) has also bolstered the middle market/private wealth bid as that group of investors seeks to replace the higher yielding AT1 bank instruments.

Source: NAB Capital Markets Origination, March 2025

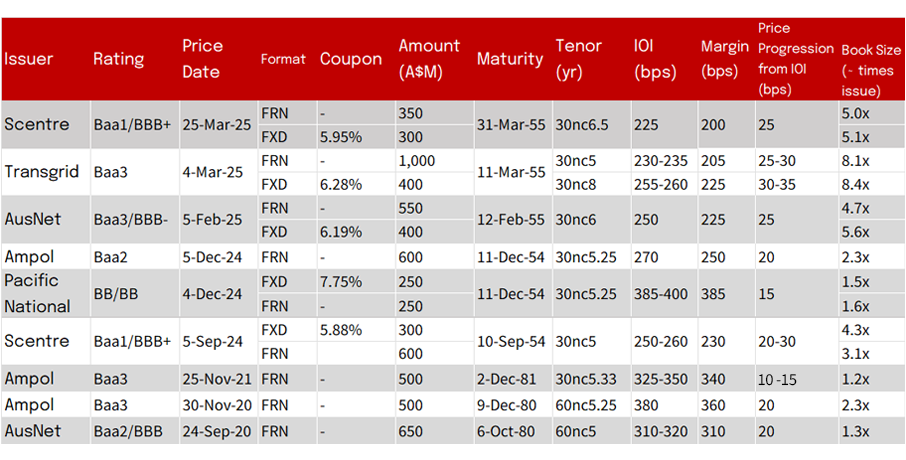

Multi-tenor hybrid issuances have been tested with Transgrid’s A$1.4 billion dual-tranche issuance in March this year signalling to market the evolving investor appetite and distinct pools of demand for different tenors. See table of activity below.

Source: NAB Capital Markets Origination, March 2025

Multi-tenor hybrid issuances have been tested with Transgrid’s A$1.4 billion dual-tranche issuance in March this year signalling to market the evolving investor appetite and distinct pools of demand for different tenors. See table of activity below.

Source: Bloomberg, March 2025

Issuance considerations:

Once issued, there is an expectation that the instrument becomes a permanent feature of the capital structure. There is an ability to reduce the outstanding balance by 25% over time. For issuers looking to solve for short-term pressure on metrics but an uplift over time in revenue, hybrids can provide an effective solution.

Broadly, investors are focused on a prudent capital management approach, especially around substantial capex plans.

Ratings agencies have shifted the goal posts on the treatment of the product. In 2012 S&P moved from offering 100% equity credit to 50% equity credit[vi]. Moody’s has been more consistent and in 2024 made a number of changes to its methodology outlined below[vii]:

- Subordinated debt that is mandatorily convertible to equity will be assigned 100% equity credit.

- Subordinated debt with an unrestricted optional coupon deferral mechanism and with a maturity date of greater than 30 years (and which adheres to all other Moody’s requirements) will receive intermediate equity credit (50%).

- The ability to receive consideration of a one notch downgrade (versus two) with consideration to the following:

- Ranking: senior to other preference shares.

- Optional Coupon Deferral: obligation to settle no later than five years from the date of initial deferral (or at redemption/maturity, on breach of dividend stopper, or on a winding up).

Overall, the NAB Capital Markets Origination Team encourages issuers to keep assessing how A$ corporate hybrid transactions can fit into their capital management strategy. Please contact us for more information on how we can help.

- Tabitha Chang is Executive Director, Corporate Origination

- Stefan Visser is Director, Hybrids and Equity Capital Markets Origination

[i] Bloomberg data, March 2025 (see in-article table)

[ii] NAB Internal data

[iii] Moody’s – credit ratings, research, and data for global capital markets and Home | S&P Global Ratings

[iv] Ibid

[v] NAB Internal data

[vi] Home | S&P Global Ratings

[vii] Moody’s – credit ratings, research, and data for global capital markets

Capital Markets Corporate and Institutional

The information contained in this article is intended to be of a general nature only. It has been prepared without taking into account any person’s objectives, financial situation or needs. NAB does not guarantee the accuracy or reliability of any information in this article which is stated or provided by a third party. Before acting on this information, NAB recommends that you consider whether it is appropriate for your circumstances. NAB recommends that you seek independent legal, property, financial and taxation advice before acting on any information in this article. You may be exposed to investment risk, including loss of income and principal invested.

You should consider the relevant Product Disclosure Statement (PDS), Information Memorandum (IM) or other disclosure document and Financial Services Guide (available on request) before deciding whether to acquire, or to continue to hold, any of our products.

All information in this article is intended to be accessed by the following persons ‘Wholesale Clients’ as defined by the Corporations Act. This article should not be construed as a recommendation to acquire or dispose of any investments.

The Forward View – Australia: August 2025

INSIGHT