Firmer consumer and steady outlook

Insight

The breadth of interest from investors across the Asia Pacific region and ease of access is helping drive a strong pipeline in the Australian Medium-Term Note (AMTN) market as New Zealand borrowers head into 2024.

New Zealand corporates are taking advantage of the Australian Medium-Term note (AMTN) market, with borrowers in recent months seeing significant demand from a broad range of investors across the Asia Pacific region.

While NZ treasurers have ready access to a resilient local retail bond market, issuance on the domestic front is often restricted in terms of volumes and tenors.

Historically, this has seen issuers turn to either the US Private Placement (USPP) market or use a European Medium-Term Note program to source longer-dated debt. A more recent shift, however, has seen corporates – including NZ telco Chorus, Contact Energy and Auckland International Airport – looking closer to home and testing the AMTN market.

The first driver behind the move is that the investor base accessed by an AMTN issuance offers natural diversification to the stable yield-driven NZD retail bond market. With mark-to-market-driven asset managers and momentum-driven private bank and broker buyers, conditions that favour issuance in AMTN format tend to be the opposite of those underpinning the “through the cycle” NZ retail bond market, or the USPP insurer-driven market.

The second part is ease of access when compared with other asset manager-led alternatives. The geographical proximity makes it abundantly easier to engage with local investors in an issuer-friendly time zone and, most importantly, the entwined history of the two countries leads to a better latent understanding of how the New Zealand economy, and by extension its issuers, operate.

Add to that, the modest cost and convenience of the documentation requirements for wholesale issuance in AMTN format and the prospect of program establishment overall becomes relatively straightforward. It even means the dedicated arranger role for documentation is largely redundant.

Subject to the “everything else being equal” caveat, we see conditions for AMTN continuing to strengthen as fund inflows continue globally, with indicators of risk appetite showing continued gradual expansion and the rates outlook hovering between balanced to favourable for fixed income investors.

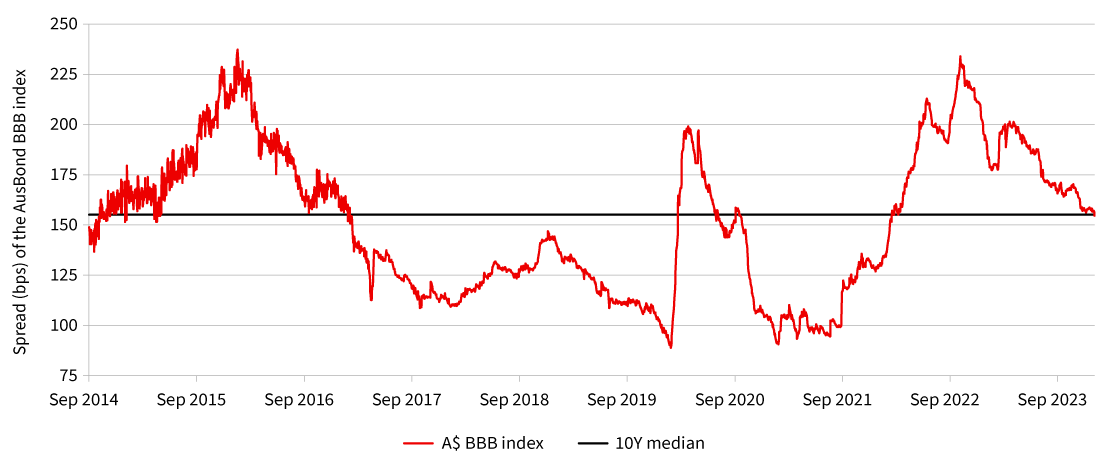

This is a positive signal towards a more bullish backdrop given we closed 2023 with a return to a balanced environment, with the spread on the AusBond BBB index around the 10-year median, new issue concessions globally back to 6bps and around the “fair” level of 5bps, and a return to the typical 7-10bps per annum spread for tenors beyond five years.

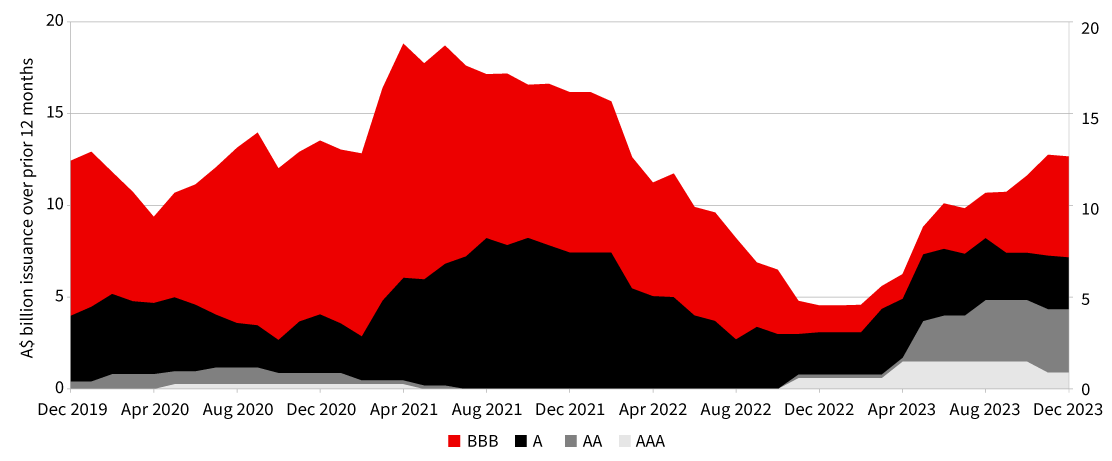

A$MTN 12-month rolling issuance by rating

Source: NAB internal data.

Index spreads back to median levels

Source: Bloomberg, January 2024.

It’s important to note that while we’re constructive on the outlook, it’s unlikely to get to the quantitative easing-fuelled levels of 2021, which saw some of the best conditions on record for issuance. Additionally, event risks such as the Silicon Valley Bank “crisis” of early 2023 highlight the fragility of the market.

A key driver of the improved conditions in the AMTN market has been the breadth of investors, with a notable increase in offshore participation returning after a dour 2022. Of the trades led by NAB, we observed an average of 73 investors per transaction with 37% of demand originating from outside of Australia.

Investor engagement, particularly on a debut trade, is critical to positioning the credit and maximising participation. In simple terms the more investors that look at the trade, the bigger the bookbuild and the harder it is for any one large investor to dictate the execution pathway.

A day in Sydney and Melbourne is a well-worn path, but it is important to remember that the AMTN market is a genuine access point to the Asia Pacific investor base, not just Australian fund managers.

As such, adding an Asian leg to any investor engagement can maximise interest from the broader region rather than focusing solely on the Australian fund manager segment.

Engaging this sector is potentially more important for a New Zealand-based borrower as the market structures and economic drivers in Singapore, Hong Kong and Japan don’t have the same level of overlap with Australia and so require more education to position the credit.

This means looking to avoid Asian holiday periods, along with traditional Australian downtimes around school holidays and the Easter/Anzac Day period, when targeting roadshow windows.

For those worried about the carbon footprint of a roadshow schedule, we have begun to see some issuers look at offsetting the deal-related travel through the use of carbon credits. This has resonated well with investors when addressing the ESG profile of the company.

There is always the alternative of a virtual meeting schedule, but this is only preferred where the timing benefit delivers improved execution. We’ve typically seen better investor engagement, and hence execution outcomes, with in-person meetings.

As we look to the year ahead, we expect to see the pipeline of New Zealand-based borrowers continue to build given the natural fit of the AMTN market, the ease of access, and the understanding of Kiwi credits.

Firmer consumer and steady outlook

Insight

Global growth headed for a H2 trough as tariffs start to bite

Insight

© National Australia Bank Limited. ABN 12 004 044 937 AFSL and Australian Credit Licence 230686.